In W24 in the maize landscape, some of the most relevant trends included:

- Argentina’s corn area is expected to rise 10% YoY to 1.8 million ha in 2025/26, signaling recovery after previous pest and drought setbacks. Improved pest control and favorable conditions support a production forecast of nearly 15 mmt.

- Indonesia plans to export corn following a projected 12.88% YoY harvest increase, though experts urge caution due to climate uncertainties and incomplete production data.

- Peru’s corn imports surged 22.42% YoY to 1.85 mmt, driven by strong domestic demand and higher global prices.

- US corn prices rose WoW due to tightening short-term supply. In contrast, Argentinian and Brazilian corn prices fell MoM amid robust harvest progress and increasing global competition.

1. Weekly News

Argentina

Argentina’s Corn Area Expected to Rebound 10% YoY in 2025/26 After Pest-Hit Season

Following a challenging 2024/25 season marked by the loss of 300 thousand hectares (ha) due to a severe leafhopper outbreak, corn emerged again as a leading crop in Argentina’s core region. According to the first planting intention survey by the Rosario Stock Exchange (BCR), the 2025/26 campaign will see a 10% year-on-year (YoY) increase in planted area from 1.64 to 1.8 million ha, bringing projected production to nearly 15 million metric tons (mmt). This signals a return to the upward expansion trend observed over the past decade, which had been interrupted by the 2022/23 drought and the recent pest crisis. The outlook for the upcoming season is notably optimistic, supported by reduced pest concerns, advancements in biological control methods, and favorable soil moisture levels that encourage early planting.

Brazil

Paraná Corn Crop at Risk Due to Dry Weather and Frost Threats

Corn producers in Paraná are increasingly concerned as irregular rainfall and the onset of winter threaten crop development. The National Institute of Meteorology (INMET) has warned that a cold air mass in early Jun-25 could bring frosts to parts of the Southern Region, including Paraná. Combined with several weeks of dry weather, this poses a serious risk to crop productivity. The last significant frontal rainfall occurred on Dec-24, leaving soil moisture levels insufficient heading into the critical crop growth stages.

Indonesia

Indonesia’s Corn Export Plan Draws Caution Amid Climate Uncertainty

Indonesia’s plan to export 27 thousand metric tons (mt) of corn in mid-Jun-25 has received mixed reactions. Economists support the initiative in principle but advise caution, stressing that export decisions should be based on full-year production data, which will only become clear between Sep-25 and Oct-25 when 80 to 85% of the total output is known. The harvest for Jan-25 to Jun-25 is projected at 8.07 mmt, a 12.88% YoY increase, mainly due to favorable weather conditions. However, economists warn that ongoing climate uncertainties and other variables still risk the overall season. The Ministry of Agriculture has confirmed that three regions are preparing for corn exports. However, only one has officially reported its delivery volume, while the other two have yet to provide specific figures.

Peru

Peru’s Hard Yellow Corn Imports Surged Over 22% in 2025

From Jan-25 to May-25, Peru imported 1.85 mmt of hard yellow corn (maíz amarillo duro or MAD), marking a 22.42% YoY increase compared to 1.51 mmt in the same period of 2024, according to the Agricultural Statistics Directorate (DEA) of The Ministry of Agricultural Development and Irrigation (MIDAGRI). The value of these imports reached USD 462.5 million, up 32.03% YoY from USD 350.3 million in 2024, reflecting both higher import volumes and increased global corn prices.

United States

US Corn Seeding Nears Completion with Stable Crop Conditions

As of June 9, 2025, United States (US) corn seeding for the 2025/26 crop cycle has reached 97% of the intended area, progressing 4% from the previous week and standing 3% ahead of 2024’s pace according to the United States Department of Agriculture (USDA). Crop condition ratings remain relatively stable, with 71% rated good to excellent, 24% as fair, and 5% as poor or very poor. The timely planting and consistent conditions support a positive outlook for the season.

2. Weekly Pricing

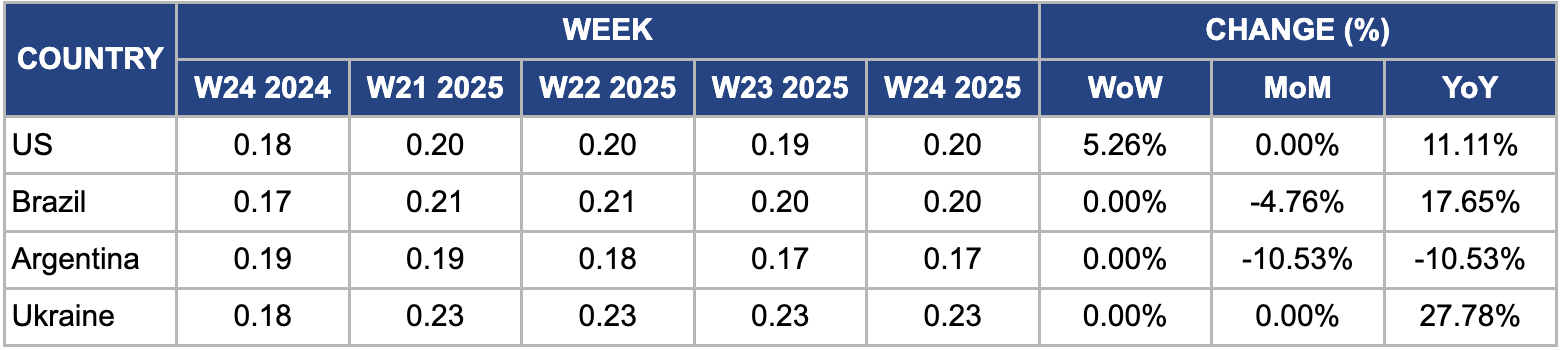

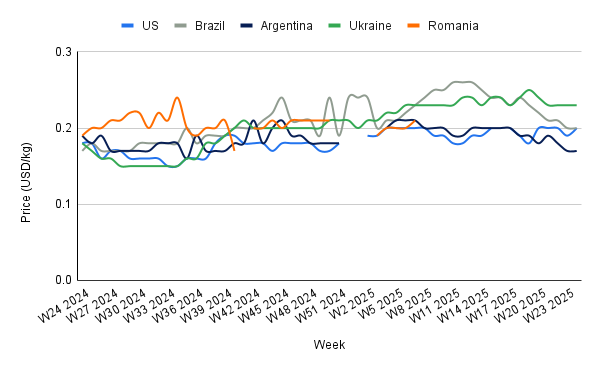

Weekly Maize Pricing Important Exporters (USD/kg)

Yearly Change in Maize Pricing Important Exporters (W24 2024 to W24 2025)

United States

In W24, US corn prices increased 5.26% week-on-week (WoW) and 11.11% YoY to USD 0.20 per kilogram (kg), primarily due to tightening supply conditions as planting nears completion. According to the USDA National Agricultural Statistics Service (NASS), as of June 9, 97% of corn had been planted, with 87% of seedlings emerging, on par with the five-year average. While this suggests steady progress, the limited remaining unplanted area indicates a slowdown in new supply additions to the market.

Brazil

In W24, Brazil’s wholesale maize prices remained unchanged WoW, but declined 4.76% month-on-month (MoM) to USD 0.20/kg, primarily due to strong production prospects and harvesting delays in key second-crop (Safrinha) regions. Persistent rainfall and lower temperatures have slowed fieldwork in states like Mato Grosso do Sul and Paraná, where only about 2% of the Safrinha area had been harvested by late May-25. Meanwhile, the first-season crop is nearly complete, with 80% already harvested. The national supply outlook remains solid, as Brazil’s National Supply Company (CONAB) raised its 2024/25 total corn production forecast to 126.8 mmt in Jun-25, up by 2.13 mmt compared to May-25, reinforcing market expectations of abundant supply and contributing to the monthly price decline.

Argentina

In W24, Argentine maize prices remained unchanged WoW but declined 10.53% MoM and YoY to USD 0.17/kg. This price drop reflects ongoing pressure from robust domestic harvest progress and increasing global competition. According to the Buenos Aires Grain Exchange (BAGE), Argentina’s 2024/25 maize harvest reached 38.7% completion by early Jun-25, with a production forecast of 46.5 mmt, significantly higher than last season’s drought-affected crop. Moreover, large exportable surpluses from Brazil and the US have intensified regional price competition, further weighing Argentine maize prices.

Ukraine

In W24, Ukrainian EXW maize prices held steady WoW and MoM at USD 0.23/kg. According to the USDA’s Jun-25 report, Ukraine’s 2024/25 corn harvest forecast remains unchanged at 30.5 mmt, with projected exports of 24 mmt and low ending stocks of just 0.6 mmt. However, the price surged 27.78% YoY from USD 0.18/kg in W24 2024. The YoY increase is mainly due to tighter global corn supplies and stronger export demand. Ukraine has remained a key supplier amid ongoing geopolitical tensions and logistical challenges in the Black Sea region.

3. Actionable Recommendations

Prioritize Early Pest and Climate Risk Mitigation in Argentina and Brazil

Authorities and farmer cooperatives in Argentina and Brazil should invest in early warning systems and broader adoption of integrated pest and climate management strategies. This includes subsidizing biological control products (such as those used against leafhoppers), supporting crop insurance adoption, and facilitating real-time soil and weather monitoring through mobile platforms and satellite-based tools. By proactively managing risks related to pests and erratic weather, producers can protect yield potential, reduce input losses, and secure higher returns. It also ensures planting and harvesting schedules remain on track, sustaining Argentina’s production rebound and minimizing weather-induced delays in Brazil’s Safrinha harvest.

Optimize Domestic Buffer Stocks and Import Timing in Southeast Asia

Indonesia and Peru should refine their corn import/export strategies by aligning them closely with updated production data and storage capacity. Indonesia should postpone exports until at least Sept-25 when harvest results are available. Meanwhile, Peru should diversify its import sources and negotiate forward contracts to manage price volatility due to increased global competition. Such timing and procurement adjustments help stabilize local markets, prevent premature exports during uncertain climate periods, and protect against unexpected shortfalls or international price spikes. This ensures food and feed security while enhancing trade efficiency.

Leverage Surplus Supplies for Regional Feed and Biofuel Markets

With abundant corn supplies in Brazil, the US, and Argentina, exporters should coordinate with regional feed manufacturers and biofuel producers to channel surpluses into nearby South American and African markets. Governments and trade boards can support this by offering export incentives or logistical assistance, especially where domestic prices are under pressure. Redirecting surplus corn to growing feed and biofuel industries will absorb excess supply, support local price floors, and create long-term trade relationships. This reduces reliance on fluctuating global demand and helps sustainability through regional supply chain integration.

Sources: Tridge, Agraria, Agrolink, Chacra Magazine, UkrAgroConsult