.jpg)

In W24 in the potato landscape, some of the most relevant trends included:

- Asia’s frozen potato market dipped slightly in 2024, with consumption down 0.4% YoY to 16 mmt and value dropping 5% to USD 16.8 billion. However, long-term growth remains positive, led by China’s 44% share.

- European potato markets face oversupply pressure, as farm-gate prices in the NEPG region plunged nearly 75% from Feb-25 to Jun-25 amid increased planting and weaker demand, despite high production costs and regulatory hurdles.

- Global prices showed mixed trends in W24, with steady-to-rising prices in the US, Germany, and Pakistan due to harvest delays and supply disruptions, while Egypt’s prices fell sharply YoY amid weak demand and ample supply.

1. Weekly News

Asia

Asia’s Frozen Potato Market Saw Brief Decline in 2024 but Long-Term Growth Remains Intact

In 2024, Asia’s frozen potato market recorded a slight 0.4% year-on-year (YoY) dip in consumption to 16 million metric tons (mmt) and a 5% decline in value to USD 16.8 billion, following eight consecutive years of growth. Despite this temporary setback, long-term trends remain positive. From 2013 to 2024, the region's frozen potato consumption grew at an average annual rate of 1.6%, while market value rose by 2.2% annually. Steady growth is forecasted through 2035, with consumption projected to reach 17 mmt and market value climbing to USD 18.9 billion. China remains the dominant market, accounting for 6.8 mmt or 44% of Asia's total frozen potato consumption in 2024, driven by growing food service demand and shifting dietary preferences.

United Kingdom

UK and EU Potato Markets Plunge Amid Oversupply Fears and Global Competition

As the new season potato harvest gained pace across the United Kingdom (UK) and Europe, demand for old crop stocks has sharply declined due to fears of oversupply and weak market activity. The North-Western European Potato Growers (NEPG) warned producers after farm-gate prices collapsed from USD 344.13 per metric ton (mt) in late Feb-25 to just USD 86.03/mt by early Jun-25. The NEPG region, including Belgium, the Netherlands, Germany, and France, has reportedly planted 25 thousand additional hectares (ha) for the 2025 season, a 5% YoY increase from 2024, intensifying oversupply risks. Growers experienced mounting global competition from countries like Canada, China, and India, which has made potatoes an increasingly globalized commodity. Moreover, high production costs, stricter European Union (EU) regulations on crop protection, and greater climate and pest challenges aggravated the situation.

United States

US Seed Potato Exports Expand in Central America and Caribbean

From Jul-24 to Mar-25, United States (US) seed potato exports posted strong growth, particularly in Central America, where shipments rose 61% YoY. Panama and Nicaragua imported US seed potatoes for the first time since the pandemic, driven by successful 2023 variety trials. Panama brought in the Soraya variety, while Nicaragua imported the Golden Globe. Long-term trials in Cuba continue, with Golden Globe expected to be registered in 2025, opening the door to potential sales later in the year. Cuba could become the largest market for US seed potatoes in the Americas outside Canada as additional varieties like Eva, Soraya, Alegria, Gala, and Blackberry move through the registration pipeline. Potatoes USA is also working to expand into the Dominican Republic’s fresh market segment and support registration of the Sound variety in Honduras, where trials were successful at six sites in 2024. These efforts highlight Potatoes USA’s strategy to strengthen global market presence through trials, grower collaboration, and tailored market development.

2. Weekly Pricing

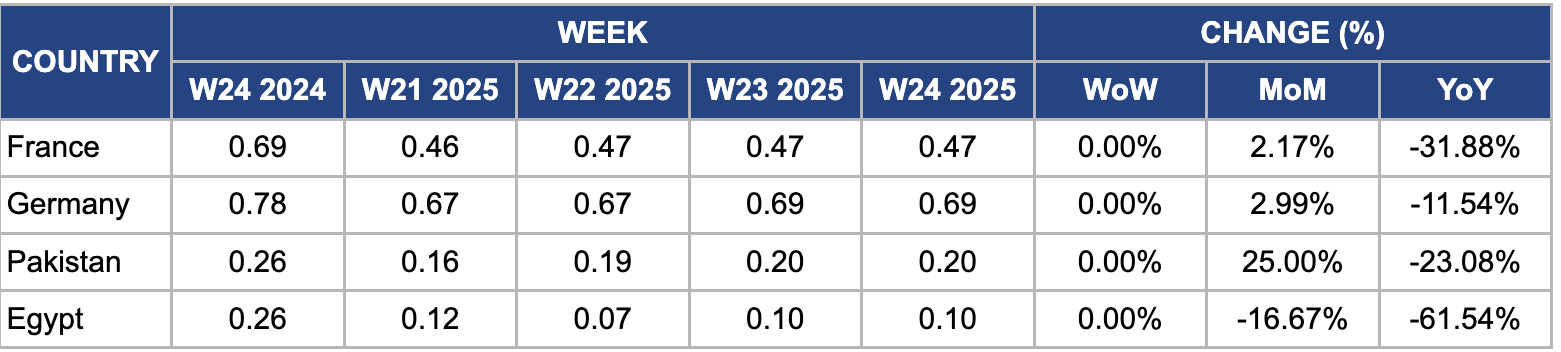

Weekly Potato Pricing Important Exporters (USD/kg)

Yearly Change in Potato Pricing Important Exporters (W24 2024 to W24 2025)

France

In W24, potato prices held steady week-on-week (WoW) at USD 0.47 per kilogram (kg) but rose 2.17% month-on-month (MoM), driven by delayed new season harvests due to cooler-than-average spring temperatures, which tightened supply. Producers anticipate a 3% YoY decline in 2025 output to 6.6 mmt, down from 6.8 mmt in 2024, adding to supply constraints. Strong domestic demand from retail and processing sectors, compounded by higher import tariffs and logistical disruptions affecting foreign supply, further supported upward price pressure during the period.

Germany

In W24, Germany’s wholesale potato prices remained unchanged WoW but rose 2.99% MoM to USD 0.69/kg. The increase stemmed from a stable flow of fresh potatoes from early harvests in key regions like Lower Saxony and Bavaria, where harvesting progressed steadily without disrupting supply. However, moderate demand from processing industries, particularly potato chip and frozen product manufacturers, put slight downward pressure on prices. Post-holiday consumer demand also softened due to seasonal factors. The modest price rise reflects a market balance between stable supply and subdued demand.

Pakistan

In W24, potato prices in Pakistan held steady WoW at USD 0.20/kg. However, prices surged 25% MoM to USD 0.20/kg, driven by weather-related disruptions in Punjab and Khyber Pakhtunkhwa, which produce over 80% of the country’s potatoes. Unseasonal rains and localized flooding delayed harvests and damaged crops, tightening supply. Rising fuel prices further inflated transportation and handling costs, a critical issue in a logistics system reliant on overland trucking. Moreover, earlier stock releases from cold storage, prompted by prior price stagnation, left limited reserves to buffer the market. With steady domestic demand and fewer arrivals in wholesale markets, traders raised prices in anticipation of short-term shortages.

Egypt

In W24, Egypt’s wholesale potato prices held steady WoW at USD 0.10/kg. However, prices declined significantly by 16.67% MoM and 61.54% YoY. The sharp YoY drop is primarily attributed to a substantial increase in domestic supply as the 2025 harvest progresses, particularly from early spring crops in major producing areas like Beheira and Dakahlia. Improved weather conditions and expanded planting areas this season have boosted production volumes, contributing to the oversupply. Moreover, reduced export activity, especially to Gulf countries, and weakened local demand in recent weeks have further pressured prices downward. The current price levels reflect high availability, subdued external demand, and seasonal market trends.

3. Actionable Recommendations

Diversify Export Markets for Surplus Supply in Europe

Given the oversupply and falling prices in North-Western Europe due to increased planted area and weak demand for old crop stocks, European producers should proactively explore export opportunities in emerging markets with rising consumption, such as Southeast Asia or Sub-Saharan Africa. Collaborative initiatives with trade agencies and processors can identify buyers in regions with growing demand for frozen and processed potatoes. By developing tailored export-grade varieties and leveraging existing EU trade agreements, growers can mitigate domestic price pressures while tapping into long-term consumption growth abroad.

Invest in Climate-Resilient Potato Varieties in South Asia

In countries like Pakistan, where weather-related disruptions and logistical issues have caused price volatility, public and private stakeholders should invest in climate-resilient and early-maturing potato varieties. Strengthening regional cold storage infrastructure and implementing farmer-focused weather advisory systems can also help stabilize supply. These efforts would improve harvest timing, reduce post-harvest losses, and increase the resilience of domestic markets against climate-related shocks.

Expand Seed Potato Trial Programs Across Latin America

Following the successful expansion of US seed potato exports to Central America, exporters should replicate their trial-based market entry model in additional Latin American and Caribbean countries. Collaborating with local agricultural ministries and research institutions to trial new varieties can build trust and accelerate regulatory approval. In particular, focusing on countries with underdeveloped seed systems, such as Guatemala, Haiti, or El Salvador, could unlock new demand while reinforcing the US' position as a premium seed supplier in the region.

Sources: Tridge, Hort News, Potato News Today, Potato Pro