In W24 in the sugar landscape, some of the most relevant trends included:

- EU sugar beet production is expected to decline due to reduced planting and adverse weather, with France and Germany facing early-season drought and pest pressure despite recent rainfall.

- China's sugar imports surged in Apr-25, showing signs of recovery, though cumulative volumes remain sharply lower YoY, with Brazil retaining its lead as the top supplier.

- India is anticipating a strong sugar production rebound in 2025/26, driven by expanded cane planting and favorable weather, likely enabling exports to exceed 3 mmt.

- Indonesia is revising sugar regulations to support its self-sufficiency target of 5 mmt by 2028 through land expansion, improved inputs, and state-backed support programs.

- Ukraine has reinstated sugar export quotas to the EU following the expiration of temporary trade measures, significantly reducing allowable volumes under the FTA.

1. Weekly News

European Union

EU Sugar Beet Output Faces Decline Due to Reduced Planting and Adverse Spring Weather

Sugar beet production in the European Union (EU) is expected to decline due to reduced planting and unfavorable weather conditions. A dry spring, particularly in key regions of France and Germany, hampered early crop development while rising pest pressure added to concerns. In France, sugar beet planting is projected to fall 5% year-on-year (YoY), with the Hauts-de-France region suffering a 60% rainfall deficit from Mar-25 to May-25. Germany also reported a 6.6% drop in the sown area. Although recent rainfall has partially alleviated dryness, the smaller cultivated area across the EU suggests a lower overall harvest. Yield forecasts remain uncertain but are currently leaning toward average outcomes.

China

China's Sugar Imports Rebound Sharply in Apr-25 Despite Steep Year-to-Date Decline

China's sugar imports experienced a sharp rebound in Apr-25, reaching USD 70 million, up 104.3% YoY, with volumes rising 148.5% YoY to 134,800 metric tons (mt). However, cumulative imports from Jan-25 to Apr-25 totaled USD 150 million, marking an 80.3% YoY decline, with volumes down 77.3% to 283,200 mt. Brazil remained the leading supplier, accounting for USD 60 million in the four-month period despite a 91.0% YoY drop. Notably, Apr-25 imports from Brazil surged 1587.0% YoY, highlighting a potential recovery in sourcing. The top ten suppliers accounted for 98.4% of total imports.

India

India Forecasts Sugar Surplus in 2025/26 as Improved Weather and Planting Boost Output and Export Potential

India is poised for a sugar production rebound, with surplus output expected for at least two consecutive years, supported by expanded sugarcane cultivation and above-average rainfall in key producing states such as Maharashtra and Karnataka. The National Federation of Cooperative Sugar Factories (NFCSF) projects gross sugar production for the 2025/26 season at 35 million metric tons (mmt), nearly 20% higher YoY. This recovery follows a drought-induced decline in 2023 that led to export restrictions in 2023/24 and limited exports in 2024/25. Improved weather and planting conditions are likely to enable exports exceeding 3 mmt in the upcoming season, strengthening India’s reentry into global sugar markets.

Indonesia

Indonesia Strengthens Regulatory Framework to Achieve Sugar Self-Sufficiency by 2028

Indonesia is revising key regulations to accelerate its goal of sugar self-sufficiency, targeting 5 mmt within the next three years. The government is amending Presidential Regulation No. 40/2023 and Presidential Decree No. 15/2024 to strengthen support for national sugar and bioethanol production, particularly in South Papua. Officials emphasized the need to follow recent surpluses in rice and corn with increased sugar output. The strategy includes expanding sugarcane farming to new areas and increasing production on existing land, improved irrigation, superior seeds, and enhanced land management, backed by government support such as subsidized fertilizers and collaboration with state-owned enterprises.

Ukraine

Ukraine Reduces 2025 Sugar Export Quota to EU Following Expiry of Temporary Trade Measures

Ukraine has reintroduced a sugar export quota to the EU for 2025, setting the limit at 11,007.5 mt under Cabinet Resolution No. 664 of June 6. This follows the expiration of the EU's Autonomous Trade Measures (ATMs), which had temporarily lifted duties and quotas on Ukrainian goods since Jun-22. With the ATMs terminated, trade reverts to the Free Trade Area (FTA) agreement, reinstating export limits on selected agricultural products. Previously, under the ATMs, Ukraine's sugar export quota for 2025 was set at 107,200 mt. Licensing for sugar exports under the new quota will remain in effect until August 5, 2025, as Ukraine and the EU continue discussions on revised trade terms.

2. Weekly Pricing

Weekly Sugar Pricing Important Producers (USD/kg)

Yearly Change in Sugar Pricing Important Producers (W24 2024 to W24 2025)

.png)

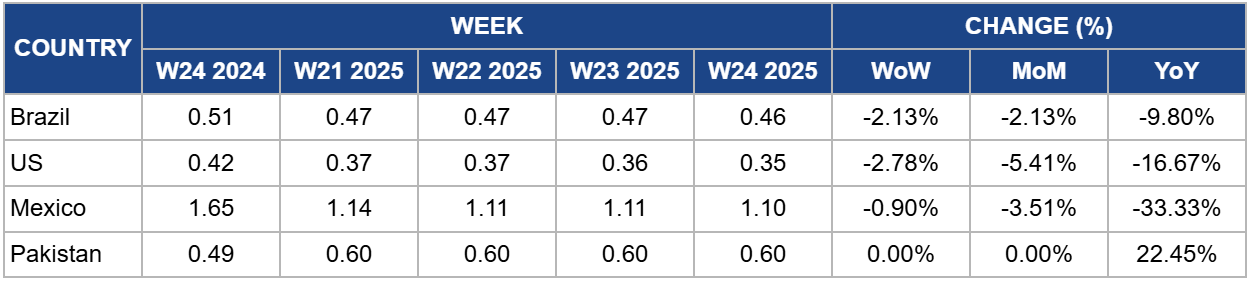

Brazil

Brazil's sugar prices declined by 2.13% week-on-week (WoW) to USD 0.46 per kilogram (kg) in W24, reflecting a 9.80% YoY decrease from USD 0.51/kg in W4 2024. The downward trend is driven by weak domestic demand for high-quality crystal sugar (Icumsa 150–180) and an increased supply of lower-grade varieties, which are being sold at deeper discounts. Center for Advanced Studies in Applied Economics (Cepea) data shows that in May-25, the average price for top-grade sugar dropped 7.2% month-on-month (MoM), with a further 0.98% MoM decline in early Jun-24. Export performance also weakened, with May-25 shipments falling 19.6% YoY, and cumulative exports from Jan-25 to May-25 down 29.6% from the same period in 2024. If these trends persist, domestic oversupply and weak international demand may continue to pressure Brazilian sugar prices in the near term.

United States

In W24, United States (US) sugar prices declined to USD 0.35/kg, reflecting a 2.78% WoW and 16.67% YoY drop amid stable domestic supply and subdued trading. Despite this decline, new pricing risks are emerging. The recent imposition of a 10% tariff on Brazilian sugar, a key US supply, could raise import costs and potentially lift domestic prices if supply tightens or alternative sources prove more expensive. While current production in Florida and Louisiana remains largely steady and imports are unchanged at 2.24 mmt raw value (RV), any future disruption or cost pass-through from tariffs could lead to modest price increases in the second half of 2025.

Mexico

In W24, Mexico’s sugar prices fell by 0.90% WoW to USD 1.10/kg, representing a sharp 33.33% YoY decline from USD 1.65/kg in W4 2024. Despite stable production projections of 5.094 mmt for the 2025/26 season, the market remains under pressure due to the lingering effects of past droughts and only partial recovery in yields. The area harvested is forecast at 760,000 hectares (ha), with a sugarcane yield of 64.2 mt/ha and a factory recovery rate of 10.44%. Although seasonal rains returned in mid-2024, supporting crop development, the continued low prices may affect profitability and future investment. While sugar exports to the US saw only a marginal 0.1% decline from Jan-25 to Apr-25, sustained domestic price weakness could lead to tighter margins and reduced incentives for production expansion unless export demand strengthens.

Pakistan

Pakistan's sugar prices held steady WoW at USD 0.60/kg in W24, reflecting a 22.45% YoY increase from USD 0.49/kg in W24 2024. This trend is attributed to high sugarcane procurement costs, reduced recovery rates, and a tighter domestic supply following substantial export volumes earlier in the year. Despite government measures, such as price controls, anti-hoarding actions, and subsidized allocations, retail prices remain elevated between USD 0.58/kg and USD 0.64/kg. With an anticipated national sugar shortfall of nearly 1 mmt, the market is likely to face continued upward price pressure. Potential imports of raw sugar could help stabilize the market, but their effectiveness will depend on the scale and timing of their arrival.

3. Actionable Recommendations

Enhance Monitoring and Risk Mitigation in EU and Brazil-Linked Supply Chains

Importers and global traders should closely monitor weather developments and planting conditions in the EU and Brazil, where lower planted areas and weak domestic demand are pressuring prices and yields. To mitigate supply disruptions and price volatility, they should implement flexible procurement strategies and consider diversifying sourcing beyond traditional suppliers such as France, Germany, and Brazil.

Leverage India's Rebound for Strategic Procurement and Long-Term Contracts

Buyers and refiners should capitalize on India’s expected surplus sugar output by engaging in forward contracts or long-term procurement agreements. With anticipated exports exceeding 3 mmt, this window offers a cost-effective opportunity to secure supplies before global prices potentially tighten again due to policy changes or weather shocks elsewhere.

Expand Market Reach and Bilateral Agreements in Response to Quota and Tariff Shifts

Exporters in countries facing new trade restrictions, such as Ukraine and Brazil, should diversify market access by strengthening ties with high-growth importers in Asia, Africa, and the Middle East. Negotiating bilateral trade agreements and investing in logistics infrastructure can help counter reduced EU quotas and US tariffs, ensuring sustained export performance.

Sources: Tridge, Hellenic Shipping News, News Foodmate, Republika, Agravery, Canal Rural, Agropolit, Michigan Farm News, El Diario de Coahuila, El Sol de San Luis