In W25 in the maize landscape, some of the most relevant trends included:

- Argentina's corn harvest progress remains slow due to excessive moisture and flooding, though strong yields support the unchanged production forecast of 49 mmt. Prices held steady at USD 0.17/kg in W25 but remained lower YoY amid balanced supply expectations.

- Brazil's 2024/25 corn production is poised for a near-record 127 mmt, driven by favorable rainfall and high Safrinha productivity. However, domestic demand from biofuel and livestock sectors is expected to limit export availability. Prices rebounded 5% WoW to USD 0.21/kg amid harvest delays and weather disruptions.

- Minas Gerais recorded a sharp surge in corn exports between Jan-25 and Apr-25, with volumes rising 573% YoY. Export revenues increased by 34% YoY. This growth reflects the state's growing relevance as a cultural and economic contributor to Brazil’s corn market.

- The US corn crop shows strong early development, with 94% emerging and 72% rated good to excellent. The USDA maintained its 2024/25 output estimate at 377.63 mmt, while prices held steady at USD 0.20/kg, supported by favorable weather and high production expectations.

1. Weekly News

Argentina

Argentina's Corn Harvest Nears 50% in W25 as Excess Moisture Slows Progress but Yields Surpass Expectations

Argentina’s 2024/25 corn harvest reached just under 50% completion in W25, hindered by excessive moisture and flooding in key regions, such as Buenos Aires and Santa Fe. Despite the delays, the Buenos Aires Grain Exchange (BAGE) reported that yields in some areas have exceeded initial expectations. The national production forecast remains unchanged at 49 million metric tons (mmt), reflecting a balance between improved yields and weather-related setbacks.

Brazil

Brazil's 2024/25 Corn Harvest Set to Hit 127 MMT, Driven by Record Yields

According to a University of Illinois research, Brazil's 2024/25 corn production is projected to reach 127 mmt, marking the second-largest harvest in the country's history. Favorable rainfall in Apr-25 and May-25 boosted yields, particularly for the second crop (Safrinha), which accounts for 78% of total output and is expected to rise 11% year-on-year (YoY). While the cultivated area increased marginally, record productivity, estimated at 5.96 metric tons (mt) per hectare (ha), has driven the output surge. Despite the strong harvest, corn exports are forecast to decline by 9% in 2025 due to higher domestic demand from the livestock and biofuel sectors.

Minas Gerais Corn Exports Surge 573% in Early 2025

Between Jan-25 and Apr-25, Minas Gerais significantly increased its corn exports, shipping 105,000 mt, a 573% rise compared to the same period in 2024, according to the State Secretariat of Agriculture, Livestock and Supply (SEAPA). Export revenues reached USD 32 million, which is 34% higher YoY. The smaller revenue increase, despite the sharp rise in volume, reflects a significant drop in the average export price per mt, likely due to global oversupply and intensified market competition. The majority of exports (101,000 mt) were classified as cereal corn, with a remarkable 1,200% increase in volume and USD 22 million in revenue. Minas Gerais remains an important corn producer in Brazil, with cultural significance tied to traditional June festivities, also known as Festa Junina. The main harvest occurs in June, coinciding with these celebrations, reflecting the crop's economic and cultural importance.

United States

US Corn Crop Shows Strong Early Development in W25

In W25, the United States Department of Agriculture (USDA) reported that 94% of the United States (US) corn crop has emerged, slightly ahead of last year and consistent with the five-year average. Crop quality remains strong, with 72% rated good to excellent, a 1-point improvement from the previous week. Iowa, the top-producing state, reported 84% of its corn in good to excellent condition, indicating favorable early-season development.

US Corn Outlook Steady Amid Global Pressures as USDA Maintains 2024/25 Production Forecast

The USDA's latest supply and demand report for the 2024/25 season kept corn production estimates unchanged: 377.63 million tons for the US, 130 million tons for Brazil, and 50 million tons for Argentina. In Chicago, Jul-25 corn futures rose 0.68% to USD 4.45/bushel, while B3, a genetically modified (GM) corn variety that expresses a third-generation Bacillus thuringiensis (Bt) trait, prices declined by 1.97%, with physical markets under downward pressure.

Market outlooks remain cautious amid several global factors, Iran's reduced corn imports could impact Brazilian exports, while geopolitical tensions in the Middle East may raise fertilizer and energy costs. The US-China tariff agreement may marginally support corn exports, though Brazil and Argentina remain strong competitors. Record US output and favorable harvests in both hemispheres continue to weigh on prices. However, Brazil's domestic demand and harvest delays may offer near-term price support, while international markets remain sensitive to US crop developments.

2. Weekly Pricing

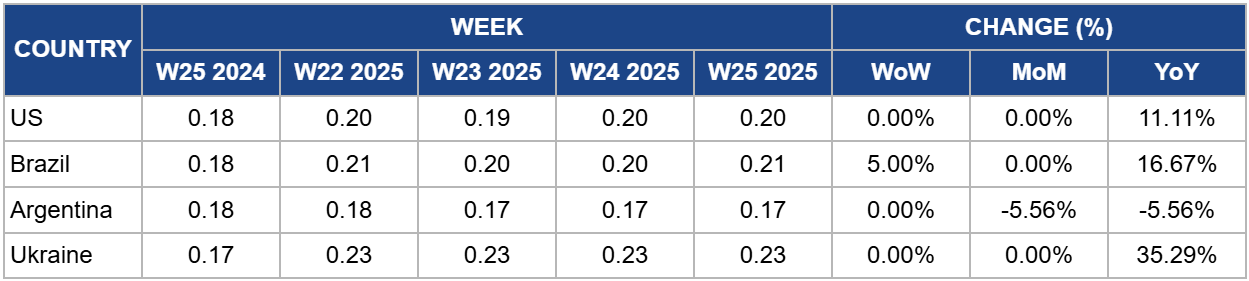

Weekly Maize Pricing Important Exporters (USD/kg)

Yearly Change in Maize Pricing Important Exporters (W25 2024 to W25 2025)

.png)

United States

In W25, US corn prices held steady at USD 0.20 per kilogram (kg), showing no week-on-week (WoW) and month-on-month (MoM) change but reflecting an 11.11% YoY increase from USD 0.18/kg. The stability in spot prices contrasts with declining Chicago Board of Trade (CBOT) corn futures, which recently hit six-month lows amid limited weather risk premiums. Improved crop conditions in Jun-25, driven by above-average rainfall, have eased near-term supply concerns. However, with Jul-25 historically being the most critical month for yield outcomes, upcoming weather patterns, particularly the risk of heat and dryness, could add volatility to prices. A hotter-than-average Jul-25, as forecasted, could reverse current trends, potentially tightening supply and lifting prices later in the season.

Brazil

In W25, Brazil's corn prices rose 5% WoW to USD 0.21/kg, reflecting a 16.67% YoY increase. This rebound follows sharp declines in key producing regions like Sorriso, where prices fell nearly 25% in May-25 and another 15% in early Jun-25 amid the onset of the second harvest. The recent price increase may signal a tightening of domestic supply due to harvest delays caused by excessive rainfall and cold weather in southern regions such as Paraná. However, with Paraná total production forecasted to reach 105 mmt, an increase of 15% YoY, upward pressure on prices may be short-lived. Future pricing will remain sensitive to harvest pace, and input cost dynamics, particularly fertilizer prices.

Argentina

In W25, Argentina's corn prices held steady at USD 0.17/kg, showing no weekly change but reflecting a 5.56% decline MoM and YoY from USD 0.18/kg. Despite slower-than-expected harvest progress due to excess moisture and flooding in key producing areas, the BAGE maintained its 2024/25 crop estimate at 49 mmt, noting yields are meeting or exceeding forecasts. The combination of strong yield prospects and delayed harvesting is likely contributing to current price stability. Continued monitoring of harvest pace and moisture conditions will be critical, as prolonged delays could tighten near-term supply and influence price movements going forward.

Ukraine

Ukraine's corn prices held steady WoW and MoM at USD 0.23/kg in W25, but remained elevated YoY with a 35.29% increase from USD 0.17/kg in the same period last year. Recent downward pressure has emerged due to weaker export demand and favorable US crop conditions, which have improved global supply expectations. Domestic demand prices declined by USD 2.40 to 4.79/mt (UAH 100 to 200/mt), while port prices fell slightly to the USD 219–228/mt range. However, constrained local grain availability is limiting further price drops. The government's decision to raise the minimum export price to USD 0.153/kg in Jun-25 from USD 0.135/kg in Apr-25 may help stabilize prices, supporting market resilience amid fluctuating export dynamics.

3. Actionable Recommendations

Enhance Harvest Management Strategies in Argentina to Mitigate Weather-Related Delays

Argentine producers and agricultural agencies should adopt improved harvest management techniques, such as real-time moisture mapping and adaptive scheduling, to address disruptions caused by excess rainfall and flooding. Investment in mobile grain drying units and improved drainage infrastructure in vulnerable areas would accelerate harvest pace, reduce post-harvest losses, and stabilize short-term supply. These interventions are especially critical as delayed harvesting, despite strong yields, risks constraining near-term availability, and putting pressure on logistics chains.

Prioritize Domestic Supply Planning in Brazil Amid Surging Internal Demand

Given Brazil's projected record corn production and the forecasted 9% drop in exports due to rising internal demand from the livestock and biofuel sectors, policymakers and industry stakeholders should focus on strengthening domestic supply chains. Actions include expanding grain storage capacity near key consumption centers and incentivizing forward contracts between producers and domestic buyers. These measures will help ensure timely internal distribution, prevent supply disruptions, and moderate potential price spikes in the local market.

Sources: Tridge, Agrolink, Oil World, Hellenic Shipping News, Canal Rural, Super Agronom