In W25 in the sugar landscape, some of the most relevant trends included:

- Sugar production in Quintana Roo, Mexico, fell short by 300,000 mt in the 2024/25 harvest due to severe pest infestations, drought, flooding, and labor shortages, causing financial strain and low recovery rates at mills.

- The Philippines is facing a rapidly spreading RSSI infestation, threatening up to 50% sugar content loss. Local authorities and the national government are mobilizing pesticide support and emergency declarations.

- Generating USD 38.15 million in export revenue, Peru exported over 50 million kg of refined cane sugar in 2024, with Colombia, Ecuador, and the US as key markets.

- Ukraine reinstated EU-bound sugar export quotas valid through Aug-25, with leading exporters allocated specific volumes. The country is also exploring new markets in the Balkans and Middle East despite tariff barriers.

- The USDA lowered its 2025 US sugar production forecast slightly, especially in beet and Florida cane output, while imports remain near record lows. This kept prices stable but highlighted tight supply conditions.

1. Weekly News

Mexico

Quintana Roo Sugarcane Harvest Falls 300,000 MT Short in 2024/25

Quintana Roo's 2024/25 sugarcane harvest concluded with a shortfall of 300,000 metric tons (mt), yielding only 1.2 million metric tons (mmt) against a target of 1.5 mmt. According to the National Confederation of Rural Landowners (CNPR), producers faced multiple challenges including pest infestations, drought, flooding, and labor shortages, affecting over 2,800 farmers. The San Rafael de Pucté sugar mill reported one of its worst harvests in recent years, compounded by the nation’s lowest Standard Base Recoverable Kilogram of Sugar (KARBE) among 48 mills. Financial strain deepened as many growers relied on loans and machinery purchases, leaving the sector with over USD 633,797 (MXN 12 million) in debt.

Peru

Peru's Refined Cane Sugar Exports Total 20 Million KG in Early 2025

From Jan-25 to May-25, Peru exported 20,221,622 kilograms (kg) of refined cane sugar, generating free-on-board (FOB) revenues of approximately USD 14.4 million. Colombia was the largest market, accounting for 55% of exports, followed by Ecuador with 30%, the United States (US) with 13%, and the Netherlands with 1%. In 2024, Peru's total refined cane sugar exports reached over 50 million kg, valued at USD 38.15 million.

Philippines

SRA Seeks Calamity Status as Sugarcane Pest Infestation Spreads Across Philippine Provinces

The Sugar Regulatory Administration (SRA) has called on local governments to declare a state of calamity amid a rapid outbreak of the red-striped soft-scale insect (RSSI), which has spread from 87 hectares (ha) on May 22 to over 1,500 ha as of June 18 across four Philippine provinces. The Province of Negros Occidental is the most affected, with over 1,490 ha and 729 farmers impacted. The infestation ranges from mild to highly severe, threatening up to 50% reduction in sugar content if not contained. While some recovery has been noted, the SRA Administrator emphasized the urgency of comprehensive data collection and local government intervention to expedite pesticide distribution. The Department of Agriculture (DA) has approved USD 175,809 (PHP 10 million) for pest control, but timely reporting remains critical to effectively address the crisis.

Ukraine

Ukraine Allocates 2025 Sugar Export Quotas to EU Under Resolution No. 1481

By Government Resolution No. 1481, Ukraine's Ministry of Agrarian Policy has allocated export quotas for sugar shipments to the European Union (EU), valid until August 5, 2025. The distribution was based on each company's export volume to the EU from Jan-25 to May-25. Leading recipients include Radekhivskyi Sugar LLC (3,977.6 mt), Tsukoragroprom LLC (1,700.9 mt), and PK Zoria Podillya LLC (927.6 mt), among others. This measure aims to manage trade volumes under existing licensing frameworks and maintain compliance with EU trade arrangements.

Ukraine Expands Sugar Export Destinations Beyond EU Amid Tariff Challenges

While the EU remains the primary market for Ukrainian sugar due to favorable logistics, Ukraine actively seeks alternative export destinations. According to the National Association of Sugar Producers of Ukraine's (Ukrtsukor) head, exports to North Macedonia are increasing, with additional interest in Montenegro, Bosnia and Herzegovina, and Albania, though customs duties remain a barrier. The Middle East and North Africa (MENA) markets are also attracting interest, with Türkiye serving as a key buyer and potential gateway to Syria and Iraq. As of W25, Ukraine holds a duty-free sugar quota of 20,700 mt for the EU, far below the 1 to 2.5 mmt annually imported by EU countries. Industry leaders anticipate that government support in tariff negotiations could enhance Ukraine's competitiveness in these regions.

Ukrainian Sugar Prices Rise Slightly in June Despite Global Market Decline

In Jun-25, Ukraine's average retail sugar price rose by 1.55% month-on-month (MoM), reaching USD 0.82/kg (UAH 34.02/kg) as of June 19, compared to USD 0.81/kg (UAH 33.52/kg) in May-25, according to the Ministry of Finance. Prices varied across major supermarket chains, with discounted offers starting at USD 0.76/kg (UAH 31.49/kg. In contrast, global sugar prices have declined, with Jul-25 raw sugar futures falling 1.6% to USD 0.1582 per pound (lb) on June 18, the lowest level since Apr-21, driven by expectations of higher output from India and Thailand.

United States

US Lowers 2025/26 Sugar Supply Forecast Following Production Cuts and Weak Imports

The United States Department of Agriculture's (USDA) Jun-25 sugar outlook projects total the US sugar supply at 13.773 mmt, raw value (STRV), down 17,000 STRV from last month, driven by a decline in domestic production despite higher beginning stocks. Imports remain nearly unchanged at 2.474 million STRV, the lowest since 2007/08, as the refined specialty tariff-rate quota (TRQ) was not yet announced.

Total domestic production is revised down to 9.254 million STRV, due to a 30,000 STRV reduction in beet sugar output. Cane sugar production is trimmed slightly to 4.104 million STRV, with Florida’s output revised down to 2.016 million STRV, while Louisiana’s remains steady at 2.088 million STRV. Deliveries for food and beverage use are also reduced by 25,000 STRV.

The US stocks-to-use ratio is adjusted slightly upward to 11.7%. Mexico's 2025/26 sugar production is unchanged at 5.094 mmt, reflecting a 7% recovery from the previous season. While total exports from Mexico are slightly lower, exports to the US remain stable at 572,489 mt under suspension agreements.

2. Weekly Pricing

Weekly Sugar Pricing Important Producers (USD/kg)

Yearly Change in Sugar Pricing Important Producers (W25 2024 to W25 2025)

.png)

Brazil

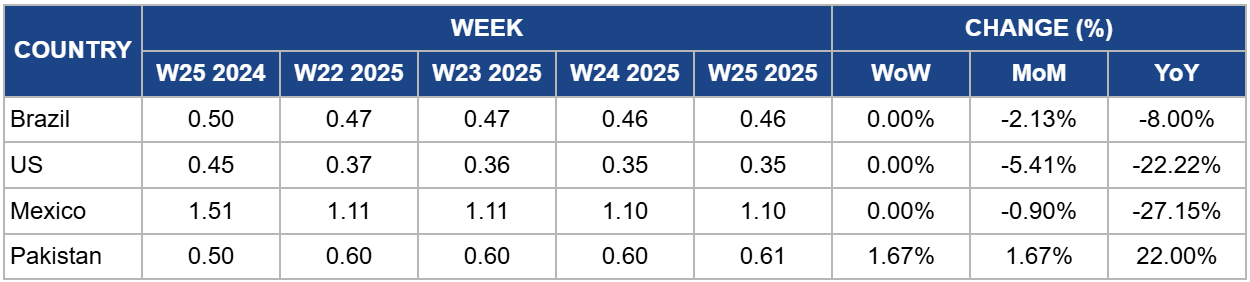

In W25, Brazil's wholesale sugar price held steady week-on-week (WoW) at USD 0.46/kg, reflecting an 8% year-on-year (YoY) decline from USD 0.50/kg. Despite the limited availability of high-quality crystal sugar (Icumsa 150) and early Jun-25 rains that disrupted production, São Paulo spot market prices continue to fall. According to the Center for Advanced Studies in Applied Economics (Cepea), external market devaluation remains the primary downward pressure. Furthermore, Icumsa 130–180 fell back to around USD 21.59 per 50-kg bag (BRL 120/50 kg), a level last experienced in Oct-22. Weak domestic prices, despite limited supply, suggest that global market pessimism is outweighing local conditions.

United States

In W25, US sugar prices remained steady at USD 0.35/kg, unchanged from the previous week but down 22.22% compared to W25 2024. The USDA's Jun-25 outlook projects a slight reduction in total sugar supply to 13.773 mmt STRV, mainly due to lower domestic production despite increased beginning stocks. Domestic production cuts, especially in beet sugar output, and modest reductions in Florida's cane sugar output contribute to supply tightening. The slight increase in the stocks-to-use ratio to 11.7% suggests moderate inventory buffers, but continued production and import uncertainties may limit upward price movement in the near term.

Mexico

In W25, Mexico’s sugar prices held steady at USD 1.10/kg, showing no weekly change but a significant 27.15% YoY decline from USD 1.51/kg. Despite stable production forecasts of 5.094 mmt for the 2025/26 season, the sector faces ongoing challenges from past drought impacts and only partial yield recovery. With harvested area projected at 760,000 ha and moderate cane yields, profitability pressures persist due to low prices. While sugar exports to the US declined slightly by 0.1% in early 2025, continued domestic price weakness could tighten producer margins and reduce incentives for expanding production unless export demand strengthens significantly.

Pakistan

In W25, Pakistan's sugar prices rose to USD 0.61/kg, 1.67% higher WoW and MoM, amid sharp domestic supply concerns. Despite exporting 765,734 mt of sugar in the current fiscal year (FY), a 2,200% YoY increase, the government has now approved the import of 750,000 mt to counter surging local prices, which reached a record USD 0.68/kg (PKR 190/kg). This reversal has drawn criticism for benefiting sugar millers at the expense of consumers, especially as the move contradicts recent free-market policy commitments.

The price increase reflects market reaction to tight domestic availability, fueled by inconsistent government interventions and reduced production, estimated at 5.9 mmt, down 14% from the prior season. Although the Pakistan Sugar Mills Association (PSMA) claims stocks are sufficient until Nov-25, the government’s large import order suggests deeper market imbalances or underreported demand. Continued policy ambiguity and perceived cartel influence may sustain elevated prices in the short term unless import volumes stabilize supply and retail price enforcement improves.

3. Actionable Recommendations

Strengthen Pest Management and Financial Relief in High-Risk Producing Regions

Governments and producer associations in countries like Mexico and the Philippines should prioritize the development of region-specific pest monitoring systems and early-warning networks to curb crop loss from infestations and weather-related disruptions. Concurrently, targeted debt restructuring, access to emergency credit lines, and subsidized input support should be extended to severely affected growers to prevent prolonged production losses and sectoral instability.

Diversify Export Strategies and Strengthen Trade Negotiations

Exporters in Ukraine and Peru should expand their market reach beyond traditional partners by prioritizing trade missions and bilateral talks with underutilized markets in North Africa, the Balkans, and Southeast Asia. Securing reduced tariff access or transit partnerships, especially through hubs like Türkiye, can offset EU quota constraints and bolster long-term competitiveness.

Enhance Regional Stock Management and Procurement Flexibility

Import-dependent markets such as Pakistan and the US should adopt dynamic procurement models, including forward contracts and strategic imports from surplus-producing nations like India or Brazil. Establishing buffer stocks during low-price cycles and improving real-time inventory tracking will help mitigate volatility and protect end-users from price spikes driven by inconsistent domestic output or delayed import approvals.

Sources: Tridge, Agravery, Agro Polit, UNIAN, Agraria, Canal Rural, Chini Mandi, The Manila Times, Por Esto!