In W25 in the wheat landscape, some of the most relevant trends included:

- EU wheat production is projected to recover in 2025/26 to about 135.6 to 136.6 mmt. However, drought in France, Germany, and the UK will limit yields. In contrast, Spain, Romania, and Bulgaria expect strong harvests.

- EU wheat exports are forecast to rise over 30% YoY to 33.5 to 34.5 mmt, supported by steady demand from MENA countries and potential trade shifts due to tariffs on Ukrainian grain.

- Argentina's elimination of the Wheat Stabilization Fund signals a shift away from subsidies, potentially impacting domestic flour and wheat prices.

- Brazil faces low wheat market liquidity in the off-season, with prices declining amid strong Argentine competition and a projected 12.6% drop in the wheat area for 2025/26. Unfavorable fertilizer trade terms reduce wheat investment, favoring other crops.

- France's wheat exports remain low due to a poor 2024 harvest, Black Sea competition, and diplomatic tensions, although recent price declines have spurred late-season demand. Domestic wheat stocks are tightening.

- Germany’s wheat production forecast is raised to 21.51 mmt for 2025, a 16.3% YoY increase, due to beneficial rainfall improving yield prospects.

1. Weekly News

European Union

EU Wheat Output to Rebound in 2025/26 Despite Regional Disparities and Shifting Trade Dynamics

The European Union (EU) wheat production is projected to recover in the 2025/26 marketing year (MY), reaching between 135.6 and 136.6 million metric tons (mmt), according to United States Department of Agriculture (USDA) estimates. However, drought in key northern and central regions, notably France, Germany, and the United Kingdom (UK), is expected to limit yield potential, making the recovery uneven. In contrast, southern and eastern EU countries such as Spain, Romania, and Bulgaria are forecast to have strong harvests due to favorable weather.

Improved output is expected to boost EU wheat exports, with forecasts ranging from 33.5 to 34.5 mmt, up over 30% year-on-year (YoY). The reintroduction of EU tariffs and quotas on Ukrainian grain may shift trade flows, potentially increasing intra-EU exports from Eastern European producers. In terms of demand, import needs from the Middle East and North Africa (MENA), especially Morocco, are expected to remain high, supporting EU wheat export prospects for the 2025/26 season.

Argentina

Argentina Eliminates Wheat Stabilization Fund, Signaling Shift in Market Regulation and Subsidy Policy

The Argentine government has announced the elimination of the Argentine Wheat Stabilization Fund (FETA), marking the first of 29 trust funds to be dissolved as part of a broader effort to reduce public spending. Established in 2022, FETA was designed to stabilize domestic wheat flour prices and subsidize the cost of common 000 flour used in bread and processed foods. Its removal may impact price dynamics across the wheat and flour value chain, particularly for bakeries and food manufacturers participating in the Fair Prices program, also known as Precios Justos, which is a voluntary government agreement between the State, consumer goods manufacturers, wholesalers, and supermarkets. The decision reflects the administration's push to dismantle state-funded subsidies deemed inefficient and opaque, signaling potential shifts in wheat market regulation and consumer pricing.

Brazil

Brazil's Wheat Market Faces Off-Season Price Pressure as Record Imports and Sluggish Planting Weigh on Outlook

In Brazil, the wheat market is experiencing low liquidity during the off-season, with domestic prices falling due to reduced trading activity and strong competition from lower-priced Argentine wheat. Spot prices between May-25 and Jun-25 declined by 2% in Paraná, reaching USD 14.26 per 60-kilogram (kg) sack (BRL 78.62/60 kg), and by 4% in Rio Grande do Sul, down to USD 12.71/60-kg sack (BRL 70.04/60-kg sack).

Imports totaled 3 mmt from Jan-25 to May-25, the highest since 2007, driven by the appreciation of the real and favorable Argentine export conditions. While mills remain well-stocked, farmers are holding back sales, awaiting better prices. Planting is advancing in Paraná (78% sown) but lags in Rio Grande do Sul (8%) due to rain. The national wheat area is projected to decline by 12.6% in the 2025/26 season. Unfavorable fertilizer trade terms continue to discourage wheat investment, favoring alternatives like canola. Global and domestic price dynamics in the coming months will depend heavily on weather developments and the progress of the United States (US) harvest.

France

FranceAgriMer Revises French Wheat Export Forecasts Upward Amid Lowest Volumes in 28 Years

The National Establishment for Agricultural and Marine Product (FranceAgriMer) has raised its forecast for French soft wheat exports within and outside the EU for the current season, despite export volumes expected to be the lowest in at least 28 years. Exports outside the EU are projected at 3.25 mmt, slightly up from May-25's forecast but down 68% from last season, while EU exports are expected to reach 6.64 mmt, a 5.6% increase. The decline in overall exports reflects a poor 2024 harvest, strong competition from the Black Sea region, and diplomatic tensions with Algeria. However, recent price drops have stimulated late-season demand, including from Egypt. Carryover wheat stocks are forecasted to fall by 22% compared to last season. Barley export forecasts have also increased amid rising sales to North African and Middle Eastern markets, though French barley stocks are expected to tighten due to low availability in competing Black Sea countries.

Germany

Germany Raises 2025 Wheat Production Forecasts Following Favorable Rainfall

Germany's National Association of Agricultural Cooperatives (DRV) has revised upward its 2025 wheat and rapeseed production forecasts following beneficial rainfall. As of W25, wheat output is expected to reach 21.51 mmt, a 0.5 mmt increase from May-25 and 16.3% higher than last year.

Romania

Romania Set for Record Wheat Harvest in 2025/26

Romania is projected to achieve a record wheat harvest of 12.2 mmt in the 2025/26 season, the highest since 1997, driven by increased yields and expanded planting areas. As of W25, harvesting is expected to begin within the next four weeks, slightly later than last year due to cooler spring temperatures, though no weather risks are anticipated in the final development phase. Romania's growing role in the global wheat market is underscored by its surpassing France in the EU wheat exports earlier this season and the inclusion of Romanian port prices in the Chicago Mercantile Exchange Group's (CME) new Black Sea wheat futures contract.

Russia

Russia's May-25 Wheat Exports Reach 1.9 MMT

In May-25, Russia exported 1.9 mmt of wheat to non-Eurasian Economic Union (EAEU) countries, with Iran as the largest importer at 342,000 metric tons (mt), followed closely by Egypt with 341,000 mt, Türkiye with 332,000 mt, Bangladesh with 159,000 mt, and Sudan with 138,000 mt. Total wheat exports for the first eleven months of the current season reached 38.7 mmt.

2. Weekly Pricing

Weekly Wheat Pricing Important Exporters (USD/kg)

Yearly Change in Wheat Pricing Important Exporters (W25 2024 to W25 2025)

.png)

Russia

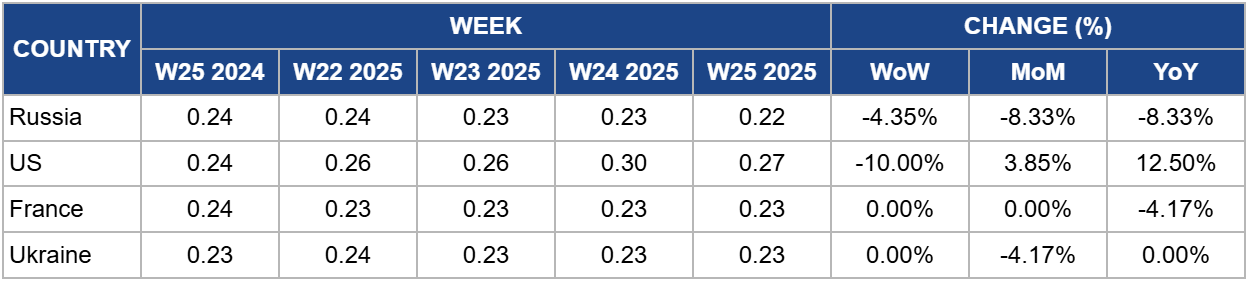

In W25, Russia’s wheat prices declined by 4.35% week-on-week to USD 0.22/kg, reflecting an 8.33% drop month-on-month (MoM) and YoY from USD 0.24/kg. Russia's wheat prices declined due to several key factors. Positive harvest prospects in the Northern Hemisphere, especially the improved condition of US spring wheat crops rising to 57% rated good to excellent, have increased global supply expectations, exerting downward pressure on prices. Although geopolitical tensions in the Middle East have created some market uncertainty, their impact on prices has been limited.

Domestically, prices at Russian deep-water ports for wheat with 12.5% protein fell by USD 6.39 (RUB 500) from 185.42/mt (RUB 14,000 to 14,500/mt) to USD 179.03 excluding value-added tax (ex-VAT), reflecting weaker demand amid abundant supply and anticipation of the upcoming harvest. Inland prices remained steady but are expected to adjust after harvests begin, with recent rains delaying barley harvesting and contributing to market uncertainty. Together with strong international competition and seasonal factors, these conditions continue to suppress Russian wheat prices in the short term.

United States

US wheat prices decreased by 10% WoW to USD 0.27/kg in W25, marking an increase of 12.50% YoY from USD 0.24/kg. US wheat prices have shown volatility amid adverse weather and geopolitical tensions. Persistent rains in the southern plains have delayed winter red wheat harvests, with threshed acreage well below the five-year average. Prices remain sensitive to weather developments, and significant shifts are expected only after clearer crop data become available.

France

France's wholesale wheat prices held steady WoW at USD 0.23/kg in W25. This stability occurs amid a reduced 2024/25 production forecast of 25.78 mmt, reflecting slightly lower yields of 6.15 mt per hectare (ha) due to adverse weather. Despite this, prices fell 4.17% YoY, pressured by weak extra-EU export demand, projected at a historic low of 3.25 mmt, and intensified competition from lower-priced Russian wheat, which has eroded France’s export competitiveness and weighed on domestic market prices.

Ukraine

In W25, Ukraine's wheat prices remained stable at USD 0.23/kg for the third consecutive week but declined 4.17% MoM from USD 0.24/kg in W22. This stabilization follows a recent downward trend driven by subdued export demand and anticipation of the upcoming harvest. Despite limited grain supply, high demand from processors has provided a floor to prices, preventing sharper declines. Class 2 wheat was priced between USD 239.67 to 270.83/mt (UAH 10,000 to 11,300/mt) Carriage Paid To (CPT), while feed wheat ranged from USD 220.50 to 244.46/mt (UAH 9,200 to 10,200/mt CPT). As harvest season nears and traders await new crop availability, current price levels may face further downward pressure. However, if farmers continue withholding grain and processor demand remains firm, near-term price stabilization could persist. Longer-term price direction will depend on harvest volume, export market developments, and domestic procurement strategies.

3. Actionable Recommendations

Enhance Intra-EU Trade and Export Diversification

Stakeholders should leverage the expected uneven recovery in EU wheat production by promoting intra-EU trade, especially from southern and eastern producers with strong harvests, to offset yield shortfalls in northern and central regions. Exporters should also target high-demand markets in MENA countries, such as Morocco and Egypt, capitalizing on robust import needs to sustain export growth despite tariff adjustments on Ukrainian grain.

Support Market Adaptation to Policy and Price Shifts in Argentina and Brazil

Wheat industry participants in Argentina and Brazil should prepare for increased price volatility and changing market dynamics due to the removal of Argentina’s Wheat Stabilization Fund and intensified price competition in Brazil. Food manufacturers and mills need to reassess pricing strategies and supply chain resilience. Meanwhile, producers should consider alternative crops or improved input efficiency to mitigate reduced wheat area and fertilizer constraints.

Implement Risk Management and Supply Chain Strategies Amid Price Volatility and Weather Uncertainty

Importers and traders should adopt flexible sourcing approaches by securing diversified supply contracts, including short-term volumes from competitively priced Russian and Ukrainian wheat while monitoring US and EU crop conditions closely. Investment in weather risk monitoring and adaptive procurement planning is critical to navigating expected price fluctuations caused by adverse weather, geopolitical tensions, and shifting harvest timelines across major producing regions.

Sources: Tridge, Oil World, Agro Meat, Agri, Uk AgroConsult, Agro Link, Agro Investor