In W27 in the wheat landscape, some of the most relevant trends included:

- The EU is reducing Ukrainian wheat imports by 80% from recent annual averages, setting a quota of 1.3 mmt under a revised trade agreement. The cap targets feed wheat, while bread wheat exports remain limited. The decision follows pressure from European farmers and is pending final approval by EU member states.

- In Brazil, wheat sowing in Rio Grande do Sul reached 50% in W27, supported by stable weather. Yield risks persist due to waterlogging, though conditions remain favorable for planting.

- In France, hot weather accelerated the wheat harvest, with soft and durum wheat harvests well ahead of the five-year average. Crop conditions are strong in the north, while drought in the south may reduce yields by 5 to 10%. Wheat prices declined by 4.17% WoW and YoY, reflecting market caution.

- Russia is maintaining its wheat production forecast of 90 mmt despite severe drought in Rostov and reduced yields in key southern regions. Domestic prices remain stable at USD 0.23/kg. A duty-free export quota was granted for the Kaliningrad region to support regional trade and development.

1. Weekly News

European Union

EU Slashes Ukrainian Wheat Imports by 80% Under Revised Trade Quotas Amid Farmer Pressure

The European Union (EU) has announced a significant reduction in wheat imports from Ukraine, cutting volumes by up to 80% compared to the past three years. Under the revised duty-free quotas in the EU-Ukraine trade agreement, wheat imports will be capped at 1.3 million metric tons (mmt), which is well below the recent annual average of over 5 mmt. This adjustment follows pressure from European farmers over surging Ukrainian imports since 2022, when the EU temporarily lifted duties in response to the war.

While the quota represents an increase over the original 2016 agreement, Ukrainian agricultural groups, including major exporter Kernel, warn that the limits will sharply impact feed wheat exports, which had dominated Ukraine's shipments to the EU. However, bread wheat exports are expected to remain largely unaffected due to their already limited trade volume. The revised agreement affects 40 products and allows for further national-level restrictions. It must still receive formal approval from EU member states.

Brazil

Wheat Sowing Reaches 50% in Rio Grande do Sul as Weather Supports Fieldwork, Yield Risks Remain

Wheat sowing in Rio Grande do Sul has reached 50% of the projected 1.2 million hectares (ha), supported by stable weather between June 23 and 27, according to the Technical Assistance and Rural Extension Company of Rio Grande do Sul – Southern Association of Rural Credit and Assistance (Emater/RS-Ascar). Crop emergence is generally uniform, with good initial stands, though some replanting was necessary in sloped areas affected by erosion.

While dry weather and cooler temperatures are aiding sowing and crop management, soil waterlogging and nutrient leaching have hindered tillering and nitrogen application in certain fields, potentially reducing yields. The state’s average yield is estimated at 2,997 kilograms (kg) per ha.

On the price front, the average value of a 60-kg bag fell slightly by 0.14%, from USD 12.65 to 12.63/60-kg (BRL 70.60 to 70.50/60-kg), while prices in Cruz Alta remained stable at USD 13.97/60-kg (BRL 78.00/60-kg). Continued favorable conditions are expected to support sowing and fieldwork within the optimal Agricultural Zoning for Climate Risk (ZARC) climate window.

India

India Turns to Premium European Wheat Flour as Italian Imports Gain Ground in 2024

India's 2024 soft wheat flour imports highlight a shift toward premium, traceable ingredients, with Italy emerging as a leading supplier. Despite a slight decline in overall import value, imports from the EU, particularly Italy, gained ground, rising to 378 metric tons (mt) valued at USD 407,776 (EUR 348,000), higher than 238 mt in 2023. The EU’s share of India's soft wheat flour import value rose to 22% in 2024, compared to 13% in 2023 and just 1% in 2015.

Italian flour is increasingly favored for its consistent quality, traceability, and adherence to EU milling standards, factors strongly promoted under the "Pure Flour from Europe" campaign, co-funded by the EU and led by the Italian Milling Industry Association (ITALMOPA). This shift is especially visible in India’s foodservice and processing sectors, which are gradually replacing re-branded imports with certified European products. The campaign’s ongoing outreach, including its upcoming presence at the International Food Exhibition (SIAL) India 2025, reflects growing Indian interest in high-quality European wheat flour amid a broader move toward premium and origin-assured ingredients.

France

Hot Weather Accelerates France's Wheat Harvest

France's wheat harvest is progressing ahead of schedule due to hot weather, according to the National Establishment for Agricultural and Marine Products (FranceAgriMer). As of June 30, 11% of the soft wheat crop had been harvested, significantly above the five-year average of 4%. Durum wheat harvest reached 33%, nearly double the seasonal norm of 17%. The rapid pace mirrors trends in barley, with autumn and spring varieties also well ahead of typical timelines. While the heat has not harmed wheat and barley, concerns are rising for maize, now nearing its critical pollination stage, with crop condition ratings showing a slight weekly decline.

Russia

Russia Maintains Wheat Harvest Forecast at 90 MMT Despite Drought in Rostov and Delays from Rain

Despite severe drought in the Rostov region, Russia's leading wheat-producing area in 2024, the country’s overall grain and wheat harvest forecasts remain unchanged. According to the Minister of Agriculture, it is expected to lose 20% of its crop this year, following a 30% loss in 2023. However, national wheat output is still projected at approximately 90 mmt, with total grain production forecast at 135 mmt. The ongoing harvest is progressing slowly due to heavy rains in central regions, with 4 mmt of grain collected so far.

Russia Approves Duty-Free Wheat Exports from Kaliningrad to Boost Regional Grain Sector

The Russian government has authorized duty-free wheat exports from the Kaliningrad region, setting a quota of 233,300 mt, which is valid until December 31, 2025. The measure applies to exports outside the Eurasian Economic Union (EAEU) and aims to enhance the export potential of local producers. Regional authorities view the decision as a step toward strengthening the sustainable development of Kaliningrad’s grain sector.

2. Weekly Pricing

Weekly Wheat Pricing Important Exporters (USD/kg)

Yearly Change in Wheat Pricing Important Exporters (W27 2024 to W27 2025)

.png)

Russia

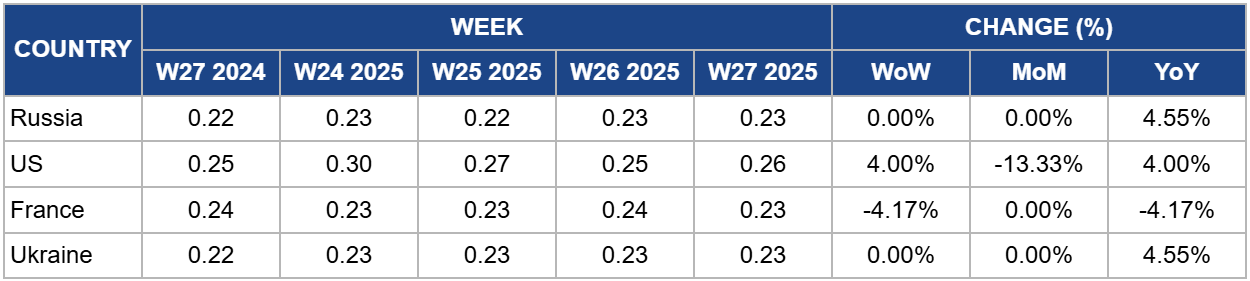

In W27, Russia's wheat prices held steady at USD 0.23/kg for the second consecutive week, showing no weekly or monthly changes, though recording a 4.55% year-on-year (YoY) increase from USD 0.22/kg in W27 2024. Price stability persists despite early signs of reduced yields in major southern production regions.

In Rostov, Russia's top wheat-producing region, early grain yields dropped to 2 mt/ha, sharply below last year’s 3.6 mt/ha. Similarly, Krasnodar saw yields fall to 4.5 mt/ha from 6.2 mt/ha, due to insufficient soil moisture. However, Stavropol reported an improved yield of 4 mt/ha, up from 3.5 mt/ha, supported by better soil moisture conditions.

If below-average yields persist across key regions, upward pressure on wheat prices may emerge later in the season, particularly if domestic or export demand strengthens. As of W27, the market appears to be in a wait-and-see phase, absorbing early data while monitoring ongoing harvest outcomes and weather conditions.

United States

In W27, US wheat prices rose to USD 0.26/kg, reflecting a 4% increase both week-on-week (WoW) and YoY from USD 0.25/kg in W27 2024. The weekly price uptick aligns with a broader rally in US crop markets, where wheat futures in Chicago rose by 3%, supported by strong export sales and speculative positioning ahead of the US Independence Day holiday on July 4.

The United States Department of Agriculture (USDA) reported wheat export sales of 586,000 mt for the 2025/26 marketing year (MY). This figure is toward the upper end of market expectations, bolstering short-term demand sentiment. Meanwhile, traders trimmed their futures positions ahead of the long weekend, anticipating possible shifts in weather or trade developments. Temperatures in major cropping areas are forecast to be moderate, with rainfall expected, reducing immediate weather-related risks. At the same time, market attention is turning to policy factors, such as the “Big Beautiful Act,” which includes biofuel mandates that may influence domestic grain usage patterns.

France

France's wheat prices declined to USD 0.23/kg in W27, a decrease of 4.17% both WoW and YoY from USD 0.24/kg in W27 2024. The decline reflects regional disparities in crop development during the 2025 season. While northern France reports improved wheat conditions with 70% of crops rated “good to excellent,” southern regions continue to suffer from drought and soil moisture deficits, which may reduce yield potential by 5 to 10% in key areas.

Soft wheat plantings rose by 9.1% YoY, but dry weather across central and western zones has limited overall gains. The current price movement suggests market caution, though tightening supplies and weather-driven risks may support future price increases, particularly for contracts maturing in late 2025 and early 2026. Traders are monitoring rainfall trends and soil moisture in critical regions, as well as potential export disruptions and global supply developments.

Ukraine

In W27, Ukraine's wheat prices remained stable at USD 0.23/kg, unchanged WoW and month-on-month (MoM) but up 4.55% YoY from USD 0.22/kg in W27 2024. The start of the winter wheat harvest in southern regions, including Odesa, Mykolaiv, and Kherson, has revealed initially low yields averaging 2.1 to 2.15 mt/ha, according to the First Ukrainian Cooperative of Suppliers and Consumers (PUSK). However, favorable weather and uninterrupted fieldwork may support improved yields as the campaign progresses.

Market activity remains subdued, with traders currently focused on barley and rapeseed, and wheat shipments to ports are expected only after mid-Jul-25. Current prices hover around USD 210/mt carriage paid to-port (CPT), third class, but analysts foresee a gradual rise to USD 230–240/mt by fall, potentially peaking at USD 250–260/mt between Dec-25 and Feb-26.

3. Actionable Recommendations

Adjust Procurement Strategies in Response to EU Import Quotas

Importers in the EU should reassess sourcing plans due to the 80% cut in Ukrainian wheat quotas. Diversifying origins, including sourcing from Russia or South America, and increasing reliance on intra-EU supply will be critical to managing potential feed wheat shortfalls.

Capitalize on Demand for Premium EU Wheat Flour in Asia

EU exporters, particularly in Italy, should expand targeted campaigns and partnerships in India’s growing premium flour segment. Leveraging traceability and quality standards can help capture market share, especially in foodservice and processing industries seeking certified products.

Monitor Yield Risks and Price Signals in Brazil and Ukraine

Traders and buyers should track weather-related yield risks in Brazil and Ukraine, where waterlogging and low early harvest yields may affect output. Early contracting or hedging strategies may be warranted ahead of possible price increases expected later in 2025.

Sources: Tridge, Sinor, Hellenic Shipping News, Agro Forum, Ukr AgroConsult, APK, AInvest