In W34 in the tomato landscape, some of the most relevant trends included:

- A severe heatwave in France has destroyed up to 80% of the tomato harvest in key regions, pushing wholesale prices up 55% YoY.. This has created a critical supply shortage across Europe.

- The termination of the US-Mexico tomato agreement has caused Mexican wholesale prices to collapse by 40% YoY. This has created a significant, short-term purchasing opportunity for US buyers before a new 17.1% tariff fully impacts the market.

- Traditionally a top exporter, Spain is undergoing a significant market shift. Its tomato exports have fallen 10% while imports have surged by over 45%, with Morocco emerging as the dominant, low-cost supplier, fundamentally altering regional trade flows.

- Extreme weather is impacting production globally, not just in Europe. In Brazil, prolonged cold weather has reduced the tomato harvest by an estimated 35%, highlighting the widespread vulnerability of supply chains to various climate shocks.

- The global agricultural landscape is undergoing significant changes. While major European producers, such as France and Spain, face a long-term decline in available farmland, nations like South Korea are pioneering a high-tech future, utilizing AI, drones, and smart farms to enhance resilience and efficiency.

1. Weekly News

Europe

France and Spain Lead European Decline in Cultivated Farmlan

Between 2014 and 2023, France and Spain experienced a significant reduction in their cultivated agricultural land, according to data from the United Nations' Food and Agriculture Organization (FAO). France lost 1.4 million hectares (ha) of cropland, a 7.3% decline. Spain also lost a substantial area, with its farmland shrinking by 581,488 ha, a 3.38% reduction. Other nations, such as Morocco and the Netherlands, also reported modest decreases in their available cropland.

In contrast, Italy expanded its agricultural footprint during the same period, adding 363,067 ha. Turkey, which has the largest cropland area of the countries analyzed, maintained its scale with a slight increase of 34,000 ha. The data also highlights the primary crops in each region, with Spain dedicating the most land to olive groves, vineyards, and almond orchards, while France's largest crop areas are used for corn and grapes. Italy's primary crops are olives and grapes.

Brazil

Cold Weather Hits Tomato Production in Brazil, Causing Prices to Soar

Prolonged cold weather in the mountainous region of Espírito Santo, Brazil, has severely impacted tomato production, resulting in a sharp increase in prices. According to a recent news report from Globo, the largest mass media conglomerate in Brazil,, low temperatures extended the crop cycle from 70 to 90 days. This delay, combined with the cold's impact on plant development, has resulted in an estimated 35% reduction in the harvest compared to last year. Consequently, with lower supply and steady demand, the price for 9 kilograms (kg) of tomatoes jumped from USD 10.68 in Jan-25 to USD 17.86 in Jun-25. The situation also raises concerns about the tomato supply for the upcoming Christmas season.

Egypt

Egypt's Agricultural Sector Sees Significant Export Growth

As of August 23, 2025, Egypt's agricultural exports have reached approximately 6.8 million metric tons (mmt), an increase of 650,000 mt from the previous year. This growth highlights the strength and global competitiveness of the Egyptian agricultural sector, contributing significantly to the national economy and foreign currency earnings.

The primary exports are citrus fruits, with volumes surpassing 1.9 mmt, and fresh potatoes, totaling more than 1.3 mmt. Tomatoes were not detailed in a report by the Central Administration for Plant Quarantine (NPPO), while they were mentioned as a key part of the various agricultural products exported, alongside garlic, mangoes, and strawberries. This success is bolstered by the opening of eight new international markets for Egyptian produce, a result of adhering to high-quality standards.

South Korea

Drones and AI Cultivate a New Generation of Farmers in South Korea

South Korea is advancing a digital transformation in its agricultural sector, utilizing drones and artificial intelligence (AI) to usher in a new era of data farming. Drones are now used to survey farmland, capturing video data that AI immediately processes to predict crop yields and identify potential pest and disease outbreaks. This technological integration helps address rural labor shortages and reduces production costs.

In support of this shift, the government and local municipalities are championing data-driven agriculture. A notable initiative is the establishment of rental smart farms aimed at young farmers. Equipped with state-of-the-art technology, these facilities lower the barrier to entry by reducing initial costs and enabling aspiring farmers to acquire practical skills before launching their own businesses, thereby fostering a new generation of innovative farmers.

Spain

Spain's Fresh Produce Exports Surge in Value

In the first half of 2025 (H1-2025), Spanish fresh fruit and vegetable exports grew 8.9% year-on-year (YoY) in value to USD 12.74 billion (EUR 10.97 billion), compared with the same period in 2024This occurred despite the export volume remaining stable at 6.6 mmt.

The growth was primarily driven by the fruit sector, which saw a 12.04% YoY rise in value and a 2.28% YoY increase in volume. Conversely, vegetable exports declined slightly in volume by 2.75% YoY, though their value still grew by 5.44% YoY. Peppers were the most valuable vegetable export, followed by tomatoes. The European Union (EU) remains the primary market, accounting for 84% of Spain's exports, with Germany as the leading destination.

A notable exception is the tomato sector, which experienced a 10% YoY drop in exports. This decline coincided with a significant 45.6% YoY increase in tomato imports, with over half of these imports now originating from Morocco, indicating a shifting dynamic in the domestic market for this key vegetable.

Turkey

Turkey Maintains Its Stronghold in the Global Tomato Market

Turkey ranks as the third-largest tomato producer in the world, with a production of 14.6 mmt last year, according to the Agriculture and Forestry Ministry. The domestic demand for tomatoes is notably high, with an average per capita consumption of about 109 kg. The nation's production exceeds local demand, achieving a sufficiency level of 117%. This surplus establishes the tomato as a significant export product for the country. Over the past decade, Turkey has exported an average of approximately 535,000 mt of tomatoes annually, solidifying its position as a key player in the global tomato market.

United States

Rutgers University Introduces the New 'Scarlet Sunrise' Tomato Variety

Rutgers University has unveiled 'Scarlet Sunrise,' a new bicolor grape tomato developed after nearly a decade of dedicated research. This sweet, crack-resistant variety features a distinctive golden-yellow hue with a reddish blush. The tomato was developed using traditional breeding methods, where a flavorful commercial grape tomato was crossed with a sweet but fragile bicolor cherry tomato to combine their best attributes.

The primary goal of producing 'Scarlet Sunrise' is to give New Jersey growers a competitive edge in a market dominated by mass producers, focusing on superior flavor as a key differentiator. The development was a painstaking process involving years of backcrossing to isolate the desired traits. After the COVID-19 pandemic delayed its official release, Rutgers University is now actively seeking commercial seed partnerships to bring the unique tomato to a broader audience, reinforcing the state's reputation for high-quality, flavorful produce. Researchers are already working on developing a more compact plant version for easier cultivation.

2. Weekly Pricing

Weekly Tomato Pricing Important Exporters (USD/kg)

Yearly Change in Tomato Pricing Important Exporters (W34 2024 to W34 2025)

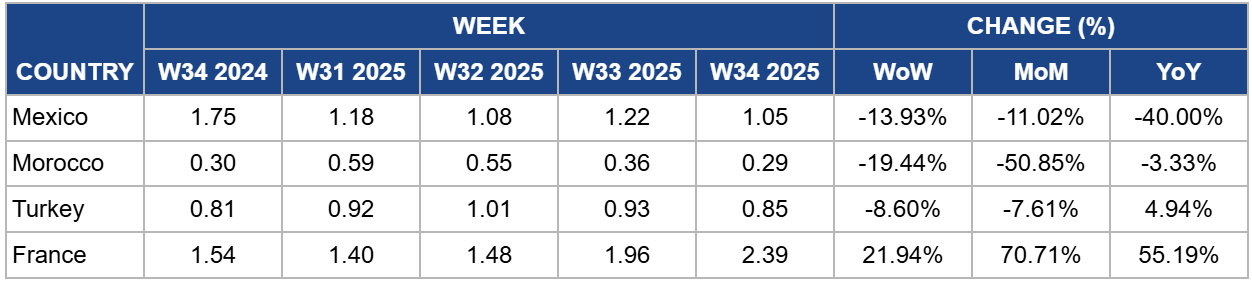

Mexico

In W34, the wholesale price for Mexican round tomatoes fell by 13.93% week-on-week (WoW) to USD 1.05/kg. This decline is part of a larger downward trend, with prices down 40% (YoY). This price collapse is a direct consequence of the United States (US) terminating the Tomato Suspension Agreement in Jul-25. This agreement had been in place since 1996, setting floor prices for Mexican tomatoes. Its termination was immediately followed by the US imposing a 17.1% antidumping duty on these imports.

The market reaction suggests Mexican exporters are moving large volumes at lower prices to sell off inventory ahead of the new duties, creating a temporary oversupply. The scale of this trade is significant. Mexico accounts for approximately 90% of US tomato imports, with exports in 2024 reaching USD 3.1 billion. Following the termination, Mexico's tomato output is projected to fall by 5% YoY. This decision has divided the US tomato industry. Southeastern growers, who feel undermined by imports, supported the move. However, western growers and importers, whose operations are deeply integrated with Mexico and support nearly 25,000 US jobs, opposed it.

Overall, Mexican exporters may be moving large volumes at lower prices to sell off inventory ahead of potential new duties, leading to a temporary oversupply and depressed prices in the market.

Morocco

The wholesale price of Moroccan tomatoes experienced a 19.44% WoW decrease, settling at USD 0.29/kg in W34. Additionally, this marks a 50.85% drop month-on-month (MoM), bringing the price nearly on par with the previous year. Morocco's growing dominance as a key tomato supplier to Europe is creating a contradictory market situation, with booming exports to Spain contrasting sharply with collapsing domestic prices. In Q1-2025, Moroccan tomato exports to Spain surged by 34% YoY in volume, underscoring strong European demand and Morocco's increasing competitiveness.

However, this export success contradicts the significant domestic price crash. The sharp decline of tomato prices in Morocco was due to ample supply, while demand was not sufficient to impact prices more significantly. Conversely, with prices in key export destinations like France soaring due to production issues, Moroccan exporters are likely to accelerate harvests to capitalize on the demand. This rapid movement of large volumes is causing a short-term glut, driving down prices as traders aim to clear inventory quickly.

Turkey

In W34, Turkish tomato prices saw a decrease of 8.60% WoW, landing at USD 0.85/kg. This slight weekly drop can be attributed to typical seasonal fluctuations, as many regions in Turkey are currently in the harvest stage, which contributes to a solid overall supply in the market and provides temporary price relief for consumers.

Despite this weekly dip, prices remain 4.94% YoY higher. Two significant factors drive this underlying strength. First, robust export demand is creating a higher price floor. The surge in Turkish exports to Syria, which has grown over 54% YoY, exemplifies this trend. Strengthened trade relations and a solid Turkish presence at international trade fairs solidify this demand, pulling prices upward.

Second, domestic supply is facing significant challenges. High summer temperatures and related pest outbreaks, such as the red spider mite, are causing considerable damage to crops, including tomatoes. This weather-induced stress threatens to reduce the overall yield and quality of the harvest, constraining supply and putting upward pressure on prices compared to the previous year.

France

French wholesale tomato prices surged by 21.94% WoW to USD 2.39/kg, continuing an upward trend that has seen prices increase by 70.71% MoM and 55.19% YoY in W34. This significant price inflation is a direct result of severe weather conditions impacting domestic production. As reported by French media (Europe 1), extreme heatwaves and drought in key agricultural regions like Occitanie have led to devastating crop losses, with some producers losing up to 80% of their harvest. High temperatures exceeding 40°C caused significant stress to plants, which resulted in poor sap flow, flower loss, and a much lower fruit yield. The heat also disrupted the typical breakdown of chlorophyll, leading to unevenly ripened tomatoes, and created ideal conditions for pests like mites to flourish, further damaging the crops. The resulting scarcity of domestic supply has driven wholesale prices to exceptionally high levels.

3. Actionable Recommendations

Secure Moroccan and Turkish Supply to Bypass French Crisis

With French tomato production impacted by extreme heat and prices surging over 55% YoY, European buyers must urgently diversify their sourcing. Morocco, which has already increased its exports to Spain by 34% YoY, offers the most immediate and cost-effective alternative due to geographical proximity and low prices at USD 0.29/kg in W34. Buyers should also secure contracts with Turkish suppliers to hedge against further regional weather disruptions and ensure a stable supply chain through the fall.

Lock in Low Mexican Prices Amidst Tariff Disruptio

The termination of the Tomato Suspension Agreement has caused Mexican wholesale prices to collapse by 40% YoY to just USD 1.05/kg in W34. This presents a significant short-term procurement opportunity for US importers and retailers. Buyers should capitalize on this price drop by securing large-volume, short- to medium-term contracts before the market adjusts to the new 17.1% US tariff and Mexican production potentially declines as a result.

Invest in Climate-Resilient Agriculture Technology

The severe crop losses in France due to adverse weather, and production challenges in Turkey due to pests and heat, underscore the growing threat of climate change to traditional agriculture. Producers should look to South Korea's model of data-driven farming, which uses AI and drones to predict yields and manage pests. Investing in innovative farm technology, protected cultivation, and developing climate-resistant varieties, such as Rutgers 'Scarlet Sunrise', will be critical for mitigating risk and ensuring long-term profitability.

Sources: Tridge, Alfallahalyoum, Sinor, G1 Globo, Donga, Agronoticias/FEPEX, Agraria, Producer