.jpg)

In W35 in the sugar landscape, some of the most relevant trends included:

- Brazil’s strong sugarcane crushing contrasts with record-low starting stocks, raising the risk of tighter margins and future volatility.

- US sugar prices remain stable due to TRQs despite global softness, though record output may pressure processors if quotas are not adjusted.

- Mexico’s wholesale market is steady, but production inefficiencies and structural challenges could limit export competitiveness.

- Pakistan continues to face elevated wholesale prices amid governance crackdowns, supply bottlenecks, and delayed import relief.

- Industry players are advised to strengthen trade positioning, adopt hedging strategies, and invest in supply chain efficiency to mitigate risks.

1. Weekly News

Brazil

Mills Shift Cane Mix to Sugar as Margins Narrow for Ethanol

Brazilian mills continued to increase the share of cane directed to sugar rather than hydrous ethanol in W35, reflecting a recalibration of processing economics as ethanol margins softened and sugar export windows remained accessible. The Brazilian Sugarcane Industry Association (UNICA) and trade reporting show sugar’s share of crushing rising above recent norms. Mills are responding by tilting the product mix to capture steady dollar-linked export demand even as aggregate crush volumes show some week-on-week (WoW) variability. This tactical shift expands near-term raw sugar availability for global markets while tightening the link between domestic ATR (total recoverable sugar) and exportable volumes.

This reallocation has muted immediate domestic upside in wholesale sugar quotes, because higher sugar output from a larger share of the crush offsets isolated supply dips. Traders need to watch ethanol pricing and mill allocation decisions into the coming weeks as a swing back to ethanol or any weather setback could quickly tighten the domestic pipeline and lift local wholesale values.

Global Benchmarks Under Pressure as Brazil’s 2H Production Holds Up

Global raw sugar benchmarks slid in W35 as markets priced in resilient Brazil supplies and the prospect of increased sugar allocation at mills. Analysts pointed to a combination of stronger-than-expected centre-south cane availability and steady harvest logistics that together capped rallies; Intercontinental Exchange (ICE) and London futures reflected this softer tone. That said, outlets note that the National Supply Company (Conab) and other forecasters are still testing seasonal scenarios — any localized rainfall or transport disruption would be an immediate upside risk for nearby contracts.

India

Government Lifts Ethanol Caps, Clearing Path for Large-Scale Diversion

In W35, New Delhi removed caps on sugar diverted to ethanol for the 2025/26 ethanol supply year and formally cleared expanded use of sugarcane juice, syrup and multiple molasses grades for ethanol production. The market reacted quickly: sugar sector equities jumped as mills signalled they can now ramp anhydrous ethanol output without the earlier quantitative constraints. Policy makers framed the move as both an energy and price-stabilization lever, enabling mills to switch output away from sugar if domestic markets weaken.

E20 Rollout Clears Hurdles, Boosting India’s Sugar Sector Outlook Amid Crop Risks

Following India’s policy announcements and a Supreme Court decision clearing E20 rollout hurdles, market sentiment turned constructive and share prices in major sugar mills rallied. Nonetheless, analysts caution that monsoon distribution, cane acreage trends, and lingering red-rot disease risks remain material constraints on crop size. For agricultural planners, the priority is ensuring cane quality and maximizing recovery rates while balancing faster ethanol offtake.

Mexico

Production Gradual Recovery Continues but Export Drumbeat is Quiet

The United States Department of Agriculture (USDA) and market analysts continue to see a gradual production recovery building from the weather-impacted trough. Improved agronomy and harvest execution have stabilized domestic availability in many regions, keeping wholesale quotes steady. Nevertheless, Mexican exports remain modest versus capacity because structural bottlenecks and legacy drought impacts limit the pace at which surplus can be channelled abroad.

Value-Add Strategies Move to Forefront as Volume Growth Lags

With Mexico’s volume upside constrained, a widening set of mills and packers are pursuing value pathways, organic certification, traceability, and sustainable sourcing, to access higher-margin specialty pockets and non-traditional buyers. These structural adjustments require up-front investment and certification lead time, so immediate price effects are modest, but in the medium term, they create differentiated revenue streams that can insulate mills from commodity swings. For producers, shifting a subset of output to premium channels is emerging as a commercially sensible hedge against continued export friction.

Pakistan

Elevated Prices Persist as Imports and Enforcement Await Execution

Pakistan’s domestic sugar market remained highly elevated in W35. Retail and wholesale quotes averaged well above government ex-mill references as distributors and consumers continued to feel tight supply. The government has placed large import orders and announced enforcement measures against hoarding, but reportage in W35 emphasizes that physical relief depends on timely arrival of shipments and transparent stock release. Until imports are landed and distributed, wholesale markers will remain vulnerable to local supply bottlenecks and speculative pressure.

The announced import volumes and enforcement rhetoric have been necessary but not sufficient to calm markets. Market observers in W35 flagged concerns about tender transparency and the timing of shipment arrivals. Analyst commentary suggests that until government action is matched with visible supply movement and tight anti-hoarding enforcement, market psychology will keep wholesale prices elevated and volatile. This places a premium on rapid, verifiable delivery of imports and clear communication from authorities.

United States

Domestic Price Insulation Continues Under TRQ Regime

United States (US) wholesale refined sugar remained relatively stable in W35 as the Tariff Rate Quota (TRQ) system continued to limit import pressure and preserve domestic price floors. USDA commentary and the August outlook reinforced that US policy mechanics are keeping domestic availability balanced even as the global market softens. For refiners and industrial buyers, the policy-backed structure is the dominant determinant of domestic wholesale pricing rather than short-term swings in world raws.

Record US Production Outlook Clouds Refinery Margins Longer Term

USDA projections released this month show elevated US sugar production for 2025/26, a development that has traders flagging potential margin pressure for refiners if demand growth lags. While current Tariff Rate Quota (TRQ) settings insulate near-term domestic prices, the record domestic crop outlook increases the risk of softer margins and heightened competition for offtake through the balance year. Processors and industrial users are therefore watching inventory, regional freight spreads, and contract roll mechanics as signals for margin management.

2. Weekly Pricing

Weekly Sugar Pricing Important Producers (USD/kg)

Yearly Change in Sugar Pricing Important Producers (W35 2024 to W35 2025)

Brazil

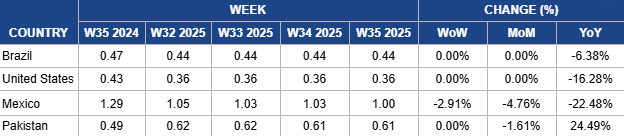

Wholesale sugar prices in Brazil remained flat in W35 at USD 0.44/kg, reflecting balanced domestic fundamentals despite global volatility. Mills continued diverting more cane towards sugar rather than ethanol, encouraged by firmer export opportunities and weaker ethanol margins. This increased sugar availability in the domestic pipeline, helping cap any strong upward movement in wholesale prices. Local traders noted that logistical efficiency and stable crush rates supported consistent supply to wholesale buyers, limiting speculative pressure.

Looking into W36, wholesale prices are expected to hold within their current range, barring unexpected weather or logistical disruptions. Any sudden shift in cane allocation back toward ethanol, or transport bottlenecks in key producing states, could introduce modest upward pressure. However, with global benchmarks softening, domestic buyers are unlikely to see sharp price hikes in the immediate term.

United States

US wholesale refined sugar prices held stable at USD 0.36/kg in W35, supported by the protective effect of the TRQ system and relatively tight domestic supplies. Even as global sugar futures softened, the US market remained insulated due to import restrictions and steady industrial demand. Wholesale markets in major consuming regions showed little price movement, with most spot trades conducted under existing long-term contracts rather than open-market adjustments.

For W36, wholesale prices are projected to remain firm within their current narrow band. Unless the USDA makes changes to quota allocations or reports unexpected shifts in beet or cane output, there is little room for downward adjustment. The main factor to watch is regional freight spreads, which could cause localized price variations for industrial buyers and distributors.

Mexico

Mexican wholesale sugar prices averaged USD 1.00/kg in W35, down 2.91% WoW. Seasonal stability, along with moderate domestic availability from a recovering production cycle, kept markets relatively calm. Despite global price corrections, local wholesale values held firm, with limited export pressure and steady internal demand helping to sustain the current price structure.

Looking ahead to W36, wholesale prices are expected to stay in the same range barring any sudden changes in trade policy or logistics. Export constraints and a focus on stabilizing internal supply suggest that volatility will be limited. The key risks remain unexpected supply chain issues or policy adjustments regarding exports, which could temporarily push prices upward.

Pakistan

Pakistan’s wholesale sugar market remained flat in W35, at USD 0.61/kg. Despite this weekly stability, prices remain firm, rising by 24.49% YoY. The supply pipeline has struggled to stabilize despite government intervention, as mills hold limited carryover stocks and imports are yet to flow into domestic distribution channels. Market participants noted that speculative stockpiling and delayed releases by traders have aggravated the shortage, pushing wholesale prices well above official benchmarks.

Government authorities have intensified enforcement efforts, including anti-hoarding drives and directives to ensure transparency in mill operations. However, these measures have not yet translated into tangible relief on the ground, as logistical delays and weak regulatory compliance dilute their impact. Industrial buyers, particularly in the confectionery and beverage sectors, continue to face elevated procurement costs, while retail consumers encounter limited availability at inflated rates.

Looking ahead to W36, wholesale sugar prices in Pakistan are expected to remain firm at elevated levels unless import shipments are expedited and effectively integrated into the market. The government’s capacity to enforce compliance among mills and distributors will be critical in determining near-term price movement. Without swift import inflows and stronger market discipline, the wholesale market is likely to remain overheated, keeping pressure on downstream users.

3. Actionable Recommendations

Strengthen Import and Export Positioning

Industry players should actively manage cross-border trade flows in light of shifting stock levels and government interventions. For Brazil, the recent surge in crushing paired with record-low starting stocks suggests that exporters should lock in forward contracts to secure margins before volatility emerges. In the US, processors and traders should closely monitor TRQ adjustments, as domestic price stability hinges on quota timing and import levels. For Mexico and Pakistan, import timing becomes critical. Mexican refiners may need to supplement domestic supply through targeted imports if output underperforms, while Pakistani buyers should anticipate bottlenecks and diversify sourcing to minimize exposure to delayed inflows.

Enhance Risk Management Through Hedging and Stock Planning

With futures volatility persisting across both sugar and related agricultural commodities, industry players should adopt hedging strategies to mitigate price swings. Brazilian mills could benefit from hedging part of their output against international futures, especially as weather risks continue to inject uncertainty into yields. In the US, refiners may seek to lock in favorable supply contracts before any adjustments in TRQs. Mexican and Pakistani traders should consider building buffer inventories where they are financially viable, as both markets face structural risks, Mexico from production inefficiencies and Pakistan from governance and hoarding pressures that could trigger sudden price spikes.

Invest in Supply Chain and Distribution Efficiency

Distribution challenges have amplified wholesale market pressures, particularly in Pakistan where anti-hoarding measures have yet to ease shortages. Industry players should invest in improving transparency and efficiency in supply chains, leveraging technology to track inventory flows and improve delivery responsiveness. In Mexico, adopting sustainable and higher-value production practices should be paired with logistics upgrades to ensure that premium-quality sugar reliably reaches export and domestic buyers. For Brazil, expanding storage and handling capacity could provide resilience against seasonal fluctuations, while US processors should optimize distribution channels to prevent localized shortages if imports are delayed.

Sources: Tridge, ADM Investor Services, Times of India, Global News Wire, Reuters, The Economic Times, USDA, The Express Tribune