1. Weekly News

Global

Global Vegetable Oil Prices Rose 0.8% MoM in Aug-24

According to the Food and Agriculture Organization of the United Nations (FAO), vegetable oil prices rose by 0.8% month-on-month (MoM) in Aug-24. The price rise is due to an increase in global palm oil prices, which offset a decrease in soybean, sunflower, and rapeseed oil prices. In contrast, global soybean oil prices fell during this period due to the positive outlook for the 2024/25 global soybean harvest.

India

India's Cooking Oil Imports Dropped in Aug-24

India's cooking oil imports declined by 17% MoM to 1.53 million metric tons (mmt) in Aug-24. Sunflower oil imports in Aug-24 dropped by 21% MoM to 288 thousand metric tons (mt). In contrast, soybean oil imports increased by 16% MoM to 456 thousand mt, reaching a two-year high. The rise in soybean oil demand is driven by increased rapeseed oil prices, prompting processors to blend more affordable soybean oil with rapeseed oil. In Jul-24, the country's vegetable oil imports exceeded domestic demand, reducing purchases in Aug-24. In addition, palm oil prices recently climbed to the same level as soybean oil, removing its price advantage.

United States

US Boosts Soybean Crushing Capacity

The United States (US) is building new soybean crushing plants and expanding existing facilities due to the country’s record soybean production in the 2023/24 season. The goal is to increase the nation’s crushing capacity from 300 thousand bushels per day in 2023 to 1.462 million bushels per day by 2026. This expansion is primarily driven by the growing demand for soybean oil, especially from the renewable diesel sector, due to the US Environmental Protection Agency’s (EPA) ongoing biofuel blending targets for gasoline and diesel refineries or importers.

2. Weekly Pricing

Weekly Soybean Oil Pricing Important Exporters (USD/kg)

Yearly Change in Soybean Oil Pricing Important Exporters (W36 2023 to W36 2024)

* Blank spaces on the graph signify data unavailability stemming from factors like missing data, supply unavailability, or seasonality

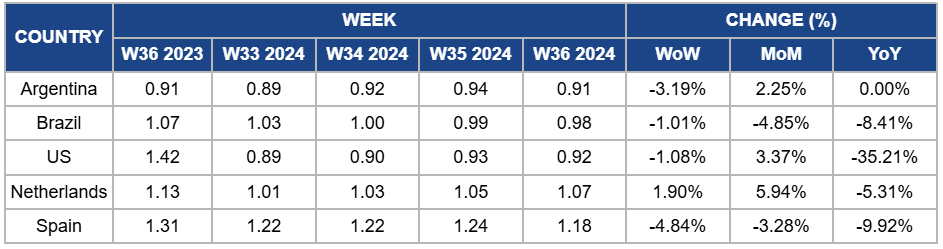

Argentina

In W36, Argentina's soybean oil price dropped to USD 0.91 per kilogram (kg), marking a 3.19% week-on-week (WoW) decline. Global soybean oil prices fell in Aug-24 due to a positive soybean production outlook in Argentina, Brazil, and the US. According to the United States Department of Agriculture (USDA), global soybean production is expected to increase 8.5% year-on-year (YoY) to 428 mmt in the 2024/25 season. Argentina's production is estimated to grow 4.1% YoY, reaching 51 mmt. The increased supply of soybeans exerts downward pressure on soybean oil prices. Future prices will largely depend on the global supply and demand dynamics.

Brazil

Brazil's soybean oil prices declined by 1.01% WoW to USD 0.98/kg in W36, compared to USD 0.99/kg in W35 due to surging soybean supply. The MoM price decreased by 4.85%, while the YoY prices dropped by 8.41%. According to the USDA, Brazil's soybean oil exports are expected to fall to 1.4 mmt in the 2024/25 season, down 22% from the previous season due to rising domestic demand for biodiesel and price competition from Argentina and the US. Soybean oil accounts for 72% of raw materials used in Brazil's biodiesel production in 2024, compared to 69% in 2024. The decreasing exports from Brazil will significantly impact the global soybean oil trade balance.

Unite States

US soybean oil prices decreased by 1.08% WoW to USD 0.92/kg in W36, reflecting an increase of 3.37% MoM and a drop of 35.21% YoY. The US soybean production is expected to increase by 10.2% YoY to 124.9 mmt in the 2024/25 season. As a result of this abundant supply, the country is expanding its soybean crushing capacity to process the increased output. However, since Jan-24, crushing margins have been tightening, partly due to falling soybean oil futures. Higher interest rates and rising production costs have further slowed down expansion efforts. There is a high risk of project cancellations for facilities that have yet to begin construction because current crush margins are insufficient to justify the high costs.

Netherlands

In W36, soybean oil prices in the Netherlands increased by 1.9% WoW and 5.94% MoM, reaching USD 1.07/kg. However, the YoY prices declined by 5.31% compared to USD 1.13/kg in W36 2023. The weekly price increase is due to the European Union (EU) ’s targets to increase the use of biofuels, which has led to higher demand for cheaper vegetable oil. Nevertheless, due to a significant global supply and uncertainties in China’s market, the prices in the Netherlands will likely decrease in the short term.

Spain

In W36, Spain’s soybean oil prices fell by 4.84% WoW to USD 1.18/kg, contributing to a 3.28% MoM decrease and a 9.92% YoY drop. The price decline is due to the overall reduction in global soybean oil prices, driven by optimistic forecasts for the 2024/25 global soybean harvest. In addition, the recent drop in global vegetable oil prices, particularly sunflower and rapeseed oils, further influenced the prices in Spain. The market will likely see price adjustments influenced by shifts in global oil supply and consumption patterns.

3.Actionable Recommendations

Prioritize Soybean Oil Purchases to Manage Costs

Indian importers and processors should focus on purchasing soybean oil as demand rises due to its cost-effectiveness compared to rapeseed oil. With rapeseed oil prices increasing, many processors blend soybean oil to reduce expenses. Additionally, palm oil, which traditionally held a price advantage, is now on par with soybean oil, making it less appealing. To manage costs efficiently, buyers should take advantage of the current affordability of soybean oil, ensuring a stable supply for future needs while monitoring shifting market conditions.

Reassess Investment in Soybean Crushing Capacity

US soybean processors should re-evaluate expansion plans due to tightening crushing margins. The country is expanding its soybean crushing capacity to meet growing demand, particularly from the renewable diesel sector. However, current interest rates and rising production costs may impact project feasibility. Facilities that have not yet started construction face a higher risk of cancellation. Investors should consider financial strategies to offset risks from potential delays or cancellations.

Focus on Domestic Biodiesel Demand

Brazilian soybean oil producers should prioritize the domestic biodiesel market over exports, as export volumes are expected to decrease. Since soybean oil is a significant component of Brazil’s biodiesel production, producers should explore partnerships with biodiesel companies to secure long-term contracts. Additionally, they should prepare for price competition from Argentina and the US and consider diversifying export destinations.

Sources: Tridge, FAO, Sinor, Agromeat, 3tres3, S&P Global