W40 2024: Beef Weekly Update

.jpg)

1. Weekly News

India

India Sets New Guidelines for Halal Meat Exports

On October 1, 2024, India announced new policy requirements for the export of certain halal meat and related products, effective October 16, 2024. The guidelines specifically address fresh and frozen meat from cattle, sheep, and goats. According to the Directorate General of Foreign Trade (DGFT), halal-certified meat and meat products will be permitted for export to 15 countries, including the United Arab Emirates (UAE), Saudi Arabia, and Bangladesh. To qualify, products must be produced, processed, and packaged in facilities certified under the 'Indian Conformity Assessment Scheme (I-CAS) – Halal' by the Indian Quality Council (ICC). Exporters are required to provide valid halal certificates to buyers in importing countries. This initiative aligns with the Ministry of Commerce and Industry's previous mandate that all halal meat exports must adhere to certification standards. The global halal food market, valued at USD 1.97 trillion in 2021, is projected to grow to USD 3.9 trillion by 2027. Halal certification is granted by various private companies in India, signifying that the food or products are permissible under Islamic law.

South Korea

Korean Beef Supply Stabilization Begins

The National Agricultural Cooperative Federation (Nonghyup) is implementing a plan to reduce the Korean beef supply by 10 thousand cows to stabilize prices through supply and demand adjustments. The project, titled the "Lower-capacity Cow Fattening Support Project Using Local Livestock Cooperative Livestock Farms," began on October 2, 2024, as part of the broader 'Korean Beef Farm Support Plan' and the 'Mid to Long-term Development Plan for the Korean Beef Industry.'

The project will involve local livestock cooperatives purchasing and fattening 7 thousand low-capacity cows under 60 months of age, with Nonghyup providing USD 296.48 (KRW 400 thousand) per cow, totaling approximately USD 63 million (KRW 85 billion) from its budget. The plan follows a request from the National Hanwoo Association for the government to purchase 20 thousand Hanwoo cows amid declining auction prices and rising production costs. The project will run until March 31, 2025, with slaughtering scheduled from January 2, 2025 to November 28, 2025. Additionally, 3 thousand of the targeted 10 thousand cows will be reduced through the 'Hanwoo Root Farm Development Project.' This initiative is expected to create a price support effect and reduce calf production, promoting stability in the Korean beef market in the mid to long-term period.

United Kingdom

UK Beef Prices Soar Amid Tight Supply and Strong Demand

Beef deadweight prices in the United Kingdom (UK) have reached a record high, exceeding USD 6.52 per kilogram (GBP 5/kg) for the first time, with an average of USD 6.56/kg (GBP 5.028/kg) as of September 21, 2024. This price is nearly USD 0.39 (GBP 0.30), higher than the same period last year and USD 1.34/kg (GBP 1.03/kg) above the five-year average. Meat Promotion Wales (HCC), an authority responsible for promoting, developing, and marketing Welsh red meat, attributes the price rise to tightening supply and sustained demand, which are expected to continue supporting prices through 2025.

UK beef prices are now among the highest globally, with the European Union (EU) average standing at USD 5.46/kg (EUR 4.99/kg), USD 1.14 (EUR 1.04) lower than the UK price, and more than 2.5 times higher than Brazilian beef. While the Department for Environment, Food and Rural Affairs (DEFRA) reported a 3% year-on-year (YoY) increase in UK prime cattle supply, global supply remains tight, with Irish cattle slaughter projected to fall by 2% YoY and European beef production to decline by 2.3% YoY in 2024. It is also worth noting that consumer demand in the UK remains strong, with a 3% YoY increase in UK beef sales for the 12 weeks ending August 4, 2024.

United States

US Beef Production Faces Decline Amid Rising Heifer Entries

Data from the United States Department of Agriculture (USDA) indicates that United States (US) cow slaughter has decreased by over 650 thousand heads year-to-date (YTD), totaling 3.76 million heads, a 15% decline from 2023. This drop, along with a significant reduction in bull slaughter, has led to a 12% YoY decline in domestic lean beef production, reaching 1.2 million metric tons (mmt), the lowest level since 2016. However, increasing heifer entries into feedlots and higher average carcass weights have mitigated the overall impact, with total beef production down by 1% YoY so far in 2024 despite a 4% YoY reduction in overall slaughter.

The USDA indicates that the rise in heifer feedlot entries is shrinking the future breeding herd, delaying a herd rebuild, and resulting in a longer-term decline in production. Consequently, US beef production is expected to drop another 4% YoY in 2025, with exports projected to fall by 13% YoY.

2. Weekly Pricing

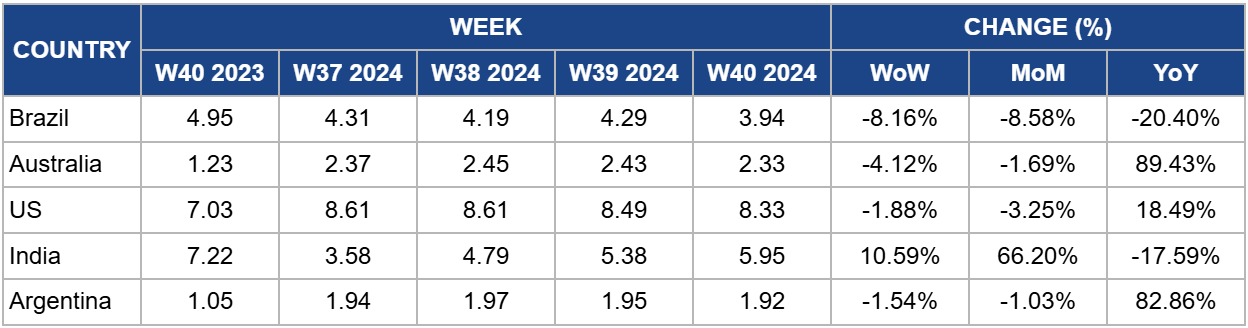

Weekly Beef Pricing Important Exporters (USD/kg)

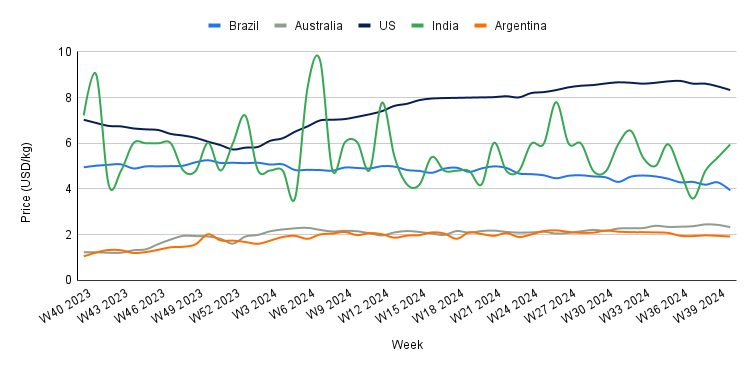

Yearly Change in Beef Pricing Important Exporters (W40 2023 to W40 2024)(W40 2023 to W40 2024)

Brazil

In W40, Brazil's wholesale price for boneless rear beef averaged USD 3.94/kg, marking a 8.16% week-on-week (WoW) decrease and a significant 20.40% YoY decline. This price drop is attributed to an increased beef supply in the market and reduced competitiveness against other meats. According to the National Supply Company (CONAB), domestic beef availability is expected to grow by 4.2% YoY, reaching 6.82 mmt in 2024. Additionally, Canal Rural reports that beef tends to lose competitiveness in the short term, particularly against proteins with lower added value, such as eggs, sausages, and chicken meat.

Australia

Australia's national young cattle indicator averaged USD 2.33/kg in W40, reflecting a 4.12% WoW decrease but a significant 89.43% YoY increase. According to Meat and Livestock Australia (MLA), despite a slight reduction in cattle yardings compared to W39, the lower supply had little positive impact on prices, as throughput remained above the annual average of 66.52 thousand heads. MLA notes that prices declined across various saleyards during the week, although some states experienced isolated supply-driven price increases. Overall, the market trend was downward, with consistent demand across sales offset by discounts on lower-quality offerings.

United States

The average price of lean beef (92% to 94% lean) in the US was USD 8.33/kg in W40, reflecting a 1.88% WoW drop but a notable 18.49% YoY rise. This decline marks the fourth consecutive week of price reductions, bringing prices to their lowest level since W26. The price drop is attributed to a decrease in demand following the peak summer season and the usual seasonal decline in beef demand as winter approaches. Nevertheless, lean beef prices remain high compared to last year, driven by reduced domestic production resulting from a shrinking cow herd, which affects overall supply.

India

In W40, the average price of cow beef in India rose to USD 5.95/kg, reflecting an 10.59% WoW increase but a 17.59% YoY decrease. These price fluctuations show the volatility of India's beef market, which has been particularly evident over the past year. This instability is primarily attributed to fluctuating domestic and international regulatory changes, as well as variations in domestic supply. Consequently, prices remain unpredictable, with market conditions significantly influenced by policy developments and supply chain dynamics.

Argentina

The average price of steer beef in Argentina decreased to USD 1.92/kg in W40, representing a 1.54% WoW decline. This price reduction is primarily due to weakened domestic demand, as beef consumption has plummeted to historic lows amid the country’s ongoing economic crisis. The Rosario Board of Trade (BCR) forecasts that Argentina's per capita beef consumption will fall to 44.8 kg by the end of 2024, marking the lowest level in 110 years and a significant decrease from the historical average of 72.9 kg. This trend reflects a broader shift in consumption patterns driven by economic challenges and diminished purchasing power.

3. Actionable Recommendations

Enhance Halal Certification Compliance

Indian exporters should invest in upgrading their production and processing facilities to meet the requirements of I-CAS – Halal. This includes obtaining certification from accredited bodies to ensure compliance with the new halal export guidelines. Regular audits and training programs for staff on halal practices can also enhance the quality and credibility of exported products, facilitating smoother access to international markets. Furthermore, Indian exporters should establish partnerships with local cooperatives to expand their sourcing capabilities and improve supply chain efficiency. Exporters should also consider exploring emerging markets in Southeast Asia and Africa, where halal demand is growing, to create new revenue streams.

Leverage Financial Support for Korean Beef Farmers

The Korean beef industry stakeholders should actively promote the "Lower-capacity Cow Fattening Support Project" to local farmers. Ensuring that farmers are aware of the financial assistance available will encourage participation and compliance. Additionally, facilitating workshops or training sessions on best practices in cattle management can help farmers enhance productivity and profitability, contributing to long-term stability in the beef supply chain.

Invest in Marketing Strategies Amid Rising UK Beef Prices

UK beef producers should invest in targeted marketing strategies that emphasize the premium quality of their products due to the high prices. Highlighting the benefits of local sourcing, sustainability practices, and the superior taste of UK beef can attract more consumers. Creating promotional campaigns that educate consumers about the reasons for the price increase, while reinforcing quality, can enhance brand loyalty and consumer trust.

Sources: EuroMeat, Nongmin, Agromeat, MLA