.jpg)

1. Weekly News

Russia

Russia's Potato Harvest Declined by 15% YoY in W41

According to the Ministry of Agriculture, Russia harvested 5.6 million metric tons (mmt) of potatoes as of W41, which is lower by 15% year-on-year (YoY). Despite the decline, officials ensure that the quantity is sufficient for domestic consumption, maintaining self-sufficiency until the next harvest. While this year's production won't reach the record 8.2 mmt harvested in 2023, Russia is well within the necessary range to meet its 8 mmt annual potato consumption needs. The Ministry had earlier forecast a harvest of 7.3 mmt for the organized sector. However, more than 50% of the country's potato production comes from private household plots, contributing significantly to the national supply.

Türkiye

Türkiye’s Potato Supply Faces Surplus and Storage Plays a Critical Role

The President of the Turkish Union of Chambers of Agriculture (TZOB) reported that Türkiye's potato supply has increased by 10% in 2024. Still, domestic and foreign demand is insufficient to absorb the surplus. Urgent government intervention is needed to balance the market and stimulate demand. The underground cold storage in Kavak can hold about 2 mmt of potatoes. These storage facilities maintain a stable temperature of 2.8°C and 90 to 95% humidity, securing Türkiye's potato supply for seven to eight months annually and preventing potential marketing disruptions. With this year's potato production expected to reach 6.5 million tons, the growing importance of these storage facilities in managing the increased harvest and ensuring stable supply and market conditions has been underscored.

Ukraine

Ukrainian Potato Prices Surged 19% WoW in Early Oct-24

As of October 8, Ukrainian farmers offered potatoes from USD 0.41 to 0.61 per kilogram (kg), marking a significant 19% week-on-week (WoW) increase. The rise in prices is due to lower yields caused by unfavorable weather conditions during the summer, with droughts in major potato-growing regions leading to a higher percentage of substandard products that cannot be stored long-term. Moreover, wholesale demand remains high as companies continue purchasing for storage, further driving up prices. In some regions, heavy rains have complicated the potato harvest, adding to the price pressure. Currently, Ukrainian potato prices are 2.8 times higher on average compared to last year's period, and many market players are holding off on selling larger volumes, anticipating even higher prices in the coming months.

Ukraine Imported Potatoes to Address Mid-Season and Late Variety Shortages

Ukraine imported mid-ripening and late varieties of potatoes in Sep-24 to cover a shortage, and further imports may continue after the sale of domestic stocks. Weather conditions and seed quality issues have impacted production, leading Ukraine to import potatoes for the first time since 2020. Despite this, the area under potato cultivation in the European Union (EU) has reached its highest levels in recent years. Ukraine is receiving small batches of potatoes from Poland, Lithuania, and Türkiye, but these imports remain far below the levels from 2019 to 2020. These shipments temporarily bridge the gap between the domestic supply of mid-season and late varieties.

2. Weekly Pricing

Weekly Potato Pricing Important Exporters (USD/kg)

Yearly Change in Potato Pricing Important Exporters (W41 2023 to W41 2024)

France

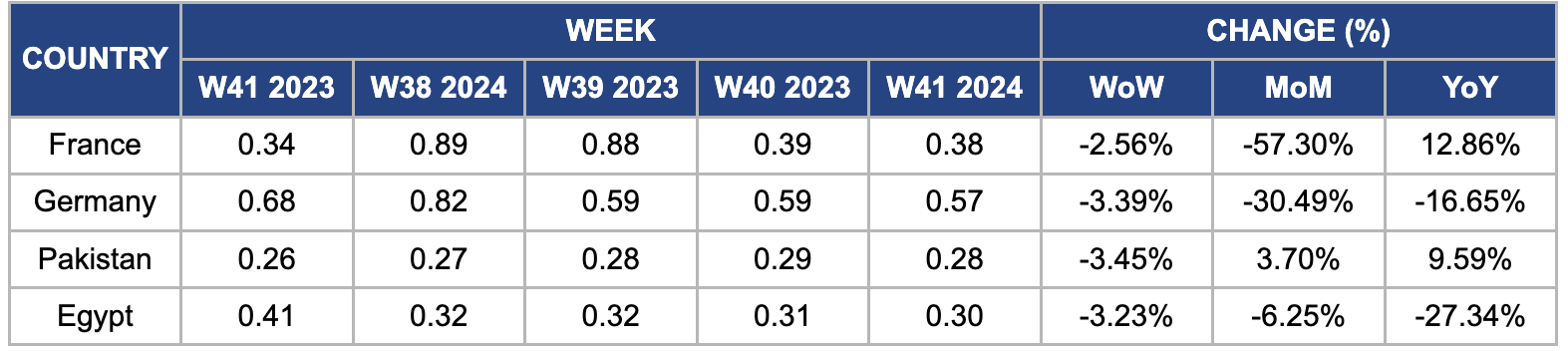

In W41, French potato wholesale prices declined by 2.56% WoW and a steep 57.30% month-on-month (MoM), reaching USD 0.38/kg. This price drop is due to the challenges in the 2024/25 potato campaign, including unfavorable weather conditions and increased pressure from plant diseases, particularly mildew. Despite these challenges, the National Union of Potato Producers (UNPT) remains optimistic, predicting a balanced production and market value outlook. France is on track for a record potato harvest, driven by a 16% YoY increase in the cultivated area, which covers 178,190 hectares (ha) in 2024. This expansion, particularly in the northwestern regions, has been supported by solid potato prices and rising demand from chip factories, positioning France as a critical player in the global potato market this season.

Germany

In W41, the wholesale price of German potatoes declined 3.39% WoW, falling to USD 0.57/kg from USD 0.59/kg in W40. This drop reflects a significant decrease of 30.49% MoM and 16.65% YoY. The price decline is expected to lead to lower supermarket prices as Germany prepares for a robust potato harvest, estimated at approximately 12.7 mmt. This figure represents a 9% YoY increase and is 17% above the average harvest. The increase in harvest size is due to a 9% expansion in potato planting areas. Despite facing challenges from late-season diseases due to adverse weather conditions, the harvest is considerably larger than last year's production. This positive trend indicates an optimistic outlook for producers and consumers regarding potato availability.

Pakistan

Pakistan's wholesale potato prices declined by 3.45% WoW, reaching USD 0.28/kg. This decrease coincided with a slight decline in the inflation rate, which fell by 0.08%. However, the annual inflation rate remains high at 12.75%. Consequently, potato prices still reflect an increase of 9.59% MoM and 3.70% YoY. The price surge is due to several factors, including rising input costs driven by a 25% reduction in seed availability due to currency depreciation, which has increased production expenses. Moreover, there is heightened export demand, particularly from regional markets like Afghanistan and the Middle East, which has intensified pressure on domestic prices. Logistical challenges have also resulted in localized supply shortages, compounding the upward price pressure.

Egypt

In W41, Egypt's wholesale potato prices declined by 3.23% WoW and 6.25% MoM, reaching USD 0.30/kg, which reflects a 27.34% YoY decrease. This price drop is primarily due to increased supply as the harvest season progresses. However, the sector faces challenges, particularly a declining currency exchange rate, which has led to a 25% reduction in seed quantities compared to the previous year. Looking ahead, Egypt anticipates further price relief with the new potato season set to commence in Nov-24, which could potentially stabilize the market.

3. Actionable Recommendations

Develop Drought-Resistant Potato Varieties

Ukraine's potato sector faces significant challenges due to erratic weather patterns, particularly droughts, which have reduced yields and created price volatility. To enhance resilience, Ukraine should focus on developing and adopting drought-resistant potato varieties such as 'Desiree,' 'Riviera,' and 'Agria,' which are known for their adaptability and high yields in dry conditions. Investing in research and development (R&D) to breed climate-adapted varieties with improved water efficiency, pest resistance, and soil optimization is crucial. Furthermore, integrating modern agronomic practices like precision irrigation, better soil management, expanding cold storage, and improving distribution channels will stabilize supply and mitigate future weather-related disruptions.

Develop Export Channels and Innovate in Domestic Consumption

Türkiye can leverage its strategic position as a trade hub between Europe, Asia, and the Middle East to cultivate new export markets for potatoes, particularly in regions like North Africa, the Caucasus, and Central Asia. Türkiye can alleviate some of its surpluses by building stronger trade relationships with these regions and targeting niche markets where demand for fresh potatoes or processed potato products (such as chips or frozen fries) is growing. Furthermore, Türkiye should develop domestic campaigns to boost potato consumption, particularly in processed forms, through partnerships with food producers and retailers. Promoting the nutritional benefits of potatoes through marketing campaigns and working with restaurants to feature potato-based dishes can stimulate demand. Establishing more effective distribution channels within Türkiye will also help reduce bottlenecks and stabilize prices, ensuring producers can sell their excess supply while maintaining reasonable consumer prices.

Expand and Modernize Cold Storage Infrastructure

Russia should focus on expanding and modernizing its cold storage infrastructure to maintain consistent supply levels and prevent market fluctuations. This would involve building larger, more efficient storage facilities across key potato-producing regions, particularly for smallholder and household producers. Enhanced cold storage capabilities would allow farmers to store potatoes for longer periods, minimizing spoilage and enabling surplus from plentiful harvests to compensate for years with lower yields, such as 2024. This would help stabilize domestic prices, reduce post-harvest losses, and improve food security. Moreover, investing in logistics networks to efficiently transport potatoes from these facilities to urban areas or export hubs could help streamline distribution, making the market less reliant on fluctuations in short-term supply.

Sources: Tridge, Agrobusiness, Sondakika, RG, Agrotimes, Dunya News