1. Weekly News

Argentina

Argentina’s Corn Planting Progress and Weather Update

In Argentina, corn planting reached 38.5% completion in W47, with progress slower in southern areas at 30 to 40% and no activity yet in the north, while core production zones are 75 to 80% planted. Light, scattered rainfall improved moisture in localized areas like Central and Southern Buenos Aires and Northern Entre Rios, but much of the country's major growing regions remain drier than usual. W48’s rain is confined to northeastern areas, risking expanded dryness elsewhere, though the 6 to 10-day forecast offers hope for better precipitation in central regions. Planting is expected to advance 1 to 2% weekly until early Dec-24, with late planting likely wrapping up in Jan-25.

Brazil

Mato Grosso’s Corn Exports in Oct-24 Declined by 4.72% MoM

Corn exports from Mato Grosso totaled 4.14 million metric tons (mmt) in Oct-24, marking a 4.72% month-on-month (MoM) decrease. However, cumulative exports from Jan-24 to Oct-24 reached 21.38 mmt, the second-highest volume since 1997, according to the Mato Grosso Institute Of Agricultural Economics (IMEA). Mato Grosso accounted for 69.48% of Brazil’s corn exports, the second-highest share in five years, reinforcing its position as a leading exporter. IMEA forecasts sustained export levels in the coming months, aligning with the average performance of the past five years and maintaining robust activity through the end of 2024.

China

China's Corn Demand Outlook and Brazil's Export Advantage in 2024/25

China's corn demand remains sluggish, but traders anticipate a potential recovery post-Chinese New Year, driven by reduced domestic stocks and the possible easing of unofficial import restrictions. If China re-enters the global corn market, Brazil stands to gain significantly, especially if United States (US) and China trade tensions resume. Brazil's corn exports to China rose to 11 mmt in the 2024/25 fiscal year, up from 10 mmt in 2023/24. Conversely, US corn exports to China are expected to decline to 2 mmt in 2024/25 from 3 mmt the prior year. Although China is a crucial market for US corn, it is smaller. Trade disruptions with China would severely impact the US soybean more than the corn market. In such a scenario, US exporters will likely redirect their corn exports to Mexico and other Central Asian buyers.

Philippines

Philippine Corn Imports Set to Increase in 2024/25

The Philippines is forecasted to increase its reliance on corn imports in the 2024/25 season, with imports estimated at 1.5 mmt, slightly down from the record 1.52 mmt in 2023/24. This import rise is due to lower domestic production and higher demand from the livestock sector, including poultry. Despite a modest recovery in domestic corn production, the country's output has struggled to meet the growing market due to pest infestations, typhoons, and limited arable land. Imports now account for 16% of total corn supply, up from 4% in 2019/20. To support this, the Philippine government reduced tariffs on corn, leading to a 56% increase in imports in 2022/23 and a 68% increase in 2023/24. While most corn has traditionally come from the Association of Southeast Asian Nations (ASEAN) countries, there is a shift toward imports from non-ASEAN countries, including Brazil and Argentina.

Ukraine

Ukrainian Corn Exports to China Set to Decline Amid Market Diversification Efforts

Ukrainian corn exports to China are forecasted to drop to 3 mmt in 2024/25, down from 5 mmt the previous season, driven by reduced Chinese demand. Ukrainian traders are diversifying markets, increasing exports to Asia and the Middle East to offset the decline. Analysts expect Chinese corn demand to recover after the Chinese New Year, with domestic stock reductions and a possible easing of import restrictions. Brazil is poised to benefit most from a rebound in Chinese demand, with exports to China projected to rise to 11 mmt, up from 10 mmt last year. Meanwhile, US corn exports to China are expected to decrease to 2 mmt, from 3 mmt previously, as trade tensions and a shift in focus toward markets like Mexico and Asia impact US exporters.

2. Weekly Pricing

Weekly Maize Pricing Important Exporters (USD/kg)

Yearly Change in Maize Pricing Important Exporters (W47 2023 to W47 2024)

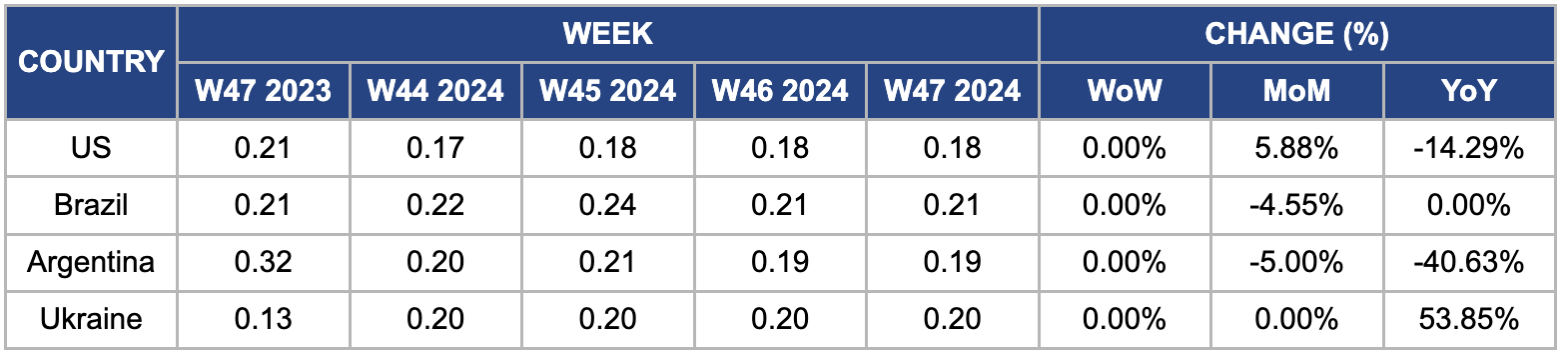

US

In W47, wholesale maize prices in the US remained stable week-on-week (WoW) at USD 0.18 per kilogram (kg) but increased 5.88% MoM. The Nov-24 World Agricultural Supply and Demand Estimates (WASDE) report forecasted lower production and ending stocks for the 2024/25 US corn season. Corn production is projected at 15.1 billion bushels, a decrease of 60 million bushels from the previous month, with a yield reduction to 183.1 bushels per acre. The harvested area remains unchanged at 82.7 million acres. Total use is forecasted to remain at 15 billion bushels, resulting in lower ending stocks of 1.9 billion bushels.

Brazil

In W47, wholesale maize prices in Brazil remained stable WoW but dropped 4.55% MoM, reaching USD 0.21/kg, driven by improved weather conditions and rainfall in the country. Despite the price decline, Brazil's first corn crop is 72% planted, slightly behind last year's pace of 76%, with farmers in Parana ahead, reaching 98% planting completion. The crop is in good condition, though some areas have shifted to grain sorghum due to lower costs. The safrinha corn acreage in Mato Grosso is expected to decrease slightly, influenced by delays in soybean planting. Wet weather in central Brazil may delay planting, potentially missing the ideal window.

Argentina

In W47, the wholesale price of Argentine corn remained unchanged WoW at USD 0.19/kg, but it declined by 5% MoM and 40.63% year-on-year (YoY). This price drop is due to recent rainfall, which improved crop conditions. Argentina's corn sowing plans for the 2024/25 campaign are optimistic, with reduced leafhopper and disease pressure, as reported by the National Monitoring Network of Dalbulus maidis. The Association of Argentine Cooperatives (ACA) expects an increase in the planting of late corn varieties, which, while yielding less than early corn, can still be profitable with proper management. The Rosario Stock Exchange forecasts that almost 8 million hectares (ha) will be planted, with a potential production of 51 to 52 mmt.

Ukraine

In W47, Ukrainian wholesale maize prices remained steady WoW at USD 0.20/kg, reflecting a 53.85% YoY increase from USD 0.13/kg in 2023. The price surge prompted the Ukrainian Agrarian Council (UAC) to revise the USDA's corn harvest forecast downward by 1 mmt to 26.2 mmt due to dry weather conditions. Challenges persist, as Ukraine's reliance on deep-sea ports has led to a 13% YoY decline in exports through the Constanta port. In the Lviv region, autumn fieldwork continues, with 96.5% of winter crops sown. In comparison, nearly 60% of the corn planted remains to be harvested, according to the Institute of Agriculture of the Carpathian Region.

3. Actionable Recommendations

Expand Export Markets

Ukraine should actively diversify its export destinations to mitigate the risks posed by reduced Chinese demand and logistical challenges at deep-sea ports. With China scaling back its corn imports from Ukraine, opportunities lie in tapping into growing markets in Southeast Asia, the Middle East, and Africa. These regions have an increasing need for corn, particularly as animal feed, driven by expanding livestock sectors. Ukraine can strengthen trade relationships with these regions by negotiating new agreements and focusing on reliable and cost-effective delivery systems. Moreover, improving land and river-based transportation routes can help overcome the limitations posed by reliance on sea-based logistics, ensuring uninterrupted supply even amid geopolitical or infrastructure challenges. Strategic market intelligence will also be crucial in identifying emerging demand patterns and tailoring export strategies accordingly, safeguarding Ukraine’s global market share.

Strengthen Strategic Position in the Global Corn Market

As the largest exporter of corn to China, Brazil could benefit from any potential recovery in Chinese demand post-Chinese New Year. Brazil should focus on bolstering its supply chain efficiency to maintain this momentum and capitalize on its export strength. Streamlining storage, transport, and logistics infrastructure can ensure rapid response to market fluctuations and help Brazil stay ahead of competitors. Furthermore, fostering closer ties with Chinese importers through long-term contracts can provide a stable demand base, reducing exposure to volatile market shifts. Keeping an eye on Chinese trade policies and tariff adjustments will also be essential in aligning export strategies with regulatory changes. By prioritizing these actions, Brazil can further solidify its dominance in the Chinese corn market while mitigating risks from US-China trade dynamics.

Enhance Adaptability to Weather Challenges

Due to weather-related delays, Argentina’s corn planting progress has been uneven, requiring a more flexible and adaptive approach to meet production goals. A key strategy is promoting late-maturing corn varieties that are better suited for delayed planting and are resilient to unfavorable weather conditions. These varieties can help maintain yields even when planting timelines are disrupted. Investing in advanced water management practices, such as irrigation systems or moisture-conserving technologies, can protect crops from prolonged dry spells. Farmers should use climate risk forecasting tools to safeguard productivity further and adjust planting and harvesting schedules based on predicted weather patterns. By adopting these measures, Argentina can minimize the impact of weather uncertainties and continue efficiently meeting domestic and export demand for corn.

Sources: Portal Do Agronegócio, AgroPortal.ua, UkrAgroConsult