.jpg)

1. Weekly News

Global

ISO Revises Global Sugar Outlook with Lower Deficit and Confirmed Surplus

The International Sugar Organization (ISO) has revised its forecast for the global sugar deficit in the 2024/25 season to 2.51 million metric tons (mmt), down from the earlier estimate of 3.58 mmt. For the 2023/24 season, the ISO projects a sugar surplus of 1.31 mmt as of W48, reversing its prior forecast of a 200,000-metric ton (mt) deficit. This is driven by lower global consumption estimates of 180.05 mmt, down from 181.46 mmt.

The ISO has also reduced its global consumption forecast for 2024/25 to 181.58 mmt from 182.87 mmt. Meanwhile, global sugar production for 2024/25 is expected to reach 179.07 mmt, slightly below the earlier forecast of 179.29 mmt and a 1.3% decline from the record 181.37 mmt produced in 2023/24.

Brazil

Brazil Anticipates 4.8% Drop in Sugarcane Harvest for 2024/25

Brazil expects a 4.8% reduction in its sugarcane harvest for the 2024/25 period, with an estimated total of 678.67 mmt. This decline is due to adverse weather conditions, including low rainfall, high temperatures, and forest fires, which affected yields in the country's Center and South. Despite these challenges, the area dedicated to sugarcane will grow by 4.3% to 8.7 million hectares (ha). Sugar production is forecasted to decrease by 3.7%, reaching 44 mmt. However, Brazil remains a dominant player in the international market, with exports expected to reach a record 23.1 mmt, up 23% from the previous period. In addition, the country's sugar export earnings are forecasted at USD 10.9 billion.

Brazil's Sugar Production in Center-South Region Drops 59.2% in Early Nov-24

According to the Union of the Sugarcane Industry (UNICA), Brazil's sugar production in the Center-South region totaled 898,000 mt in the first half of Nov-24, a 59.2% decline compared to the previous year. Sugarcane crushing also fell 52.8% to 16.46 mmt, both below market expectations. The production decline was due to a lower proportion of sugarcane allocated to sugar production, which dropped the allocation to 43% in early Nov-24, down from 50% a year earlier, with the remainder directed toward ethanol production. Total sugar production in the region for the 2024/25 season is now 3% lower than at the same time last year, totaling 38.27 mmt.

Egypt

Egypt Launches 20,000-Acre Sugarcane Cultivation Initiative with Modern Irrigation Systems

Egypt's Ministries of Water Resources and Irrigation and Agriculture are preparing to cultivate 20,000 acres of sugarcane in Luxor and Qena governorates using seedling and modern irrigation systems. Each ministry will oversee 10,000 acres in their respective governorates. The Minister emphasized the importance of transitioning to modern irrigation systems, aligning with national priorities and political directives. The project will also consider the societal and environmental impacts of modern irrigation, including water reuse, soil salinity, and drainage management.

Kenya

Kenya Advances Toward Sugar Self-Sufficiency with Record Production and Reforms

Kenya's sugar industry has reached a milestone, with all 17 sugar mills operational and domestic production surpassing demand for the first time. In Jul-24, sugar production hit 84,000 mt, exceeding the monthly consumption average of 40,000 mt. Kenya's President attributed this success to subsidized fertilizers, expanded sugarcane cultivation by 500,000 acres, and streamlined industry practices. A new sugar law has also been enacted to guide policy as Kenya aims to achieve self-sufficiency and position itself as a future sugar exporter.

Philippines

Philippines Delays Sugar Imports to Mid-2025 Due to Stable Supplies and Slow Harvest

The Philippine government has decided to delay sugar imports until mid-2025, citing stable domestic supplies of raw and refined sugar. The Agriculture Secretary and the Sugar Regulatory Administration (SRA) Director announced that imports would only be considered after the current harvest season concludes in May-25. Despite stable supply levels, the harvest has been slower than expected, with total sugarcane volume currently one-third of last year's level. The delay is attributed to lower sugar content per ton of sugarcane caused by El Niño, prompting farmers to postpone harvesting to allow sugarcane ripening.

Thailand

Thailand's Sugar Exports Poised for Record Levels in Q1-2025, Despite Lowered Production Forecast for 2024/25 Season

Thailand's sugar exports are set to reach record levels in Q1-2025, with raw sugar exports potentially hitting 2.15 mmt if logistics and seasonal starts proceed smoothly. However, global commodities trading and consulting firm specializing in sugar Czarnikow has revised its forecast for Thailand's sugarcane production in the 2024/25 season, lowering it to 105 mmt from the earlier estimate of 111 mmt due to reduced yields. Despite this, the United States Department of Agriculture (USDA) expects Thailand's total sugar exports, including raw and white sugar, to exceed 10 mmt in the 2024/25 season, driven by decreased competition from Brazil and India's export restrictions.

Ukraine

Ukrainian Sugar Beet Harvest in 2024 Declines

Ukrainian farmers harvested 11.956 mmt of sugar beets from 97.3% of the planned area, with an average yield of 476 mt/ha, marking a decrease from last year’s harvest, which totaled just over 13 mmt with an average yield of 525.3 t/ha. The top regions for total sugar beet harvest were Vinnytsia with 2.522 mmt, Khmelnytskyi with 2.180 mmt, Ternopil with 1.436 mmt, and Poltava with 1.183 mmt. The highest yields were recorded in Lviv Oblast (678.6 mt/ha), Bukovyna (635 mt/ha), Ivano-Frankivsk (585.7 mt/ha), Ternopil (578.9 mt/ha), and Khmelnytskyi (566.2 mt/ha).

2. Weekly Pricing

Weekly Sugar Pricing Important Producers (USD/kg)

Yearly Change in Sugar Pricing Important Producers (W48 2023 to W48 2024)

.png)

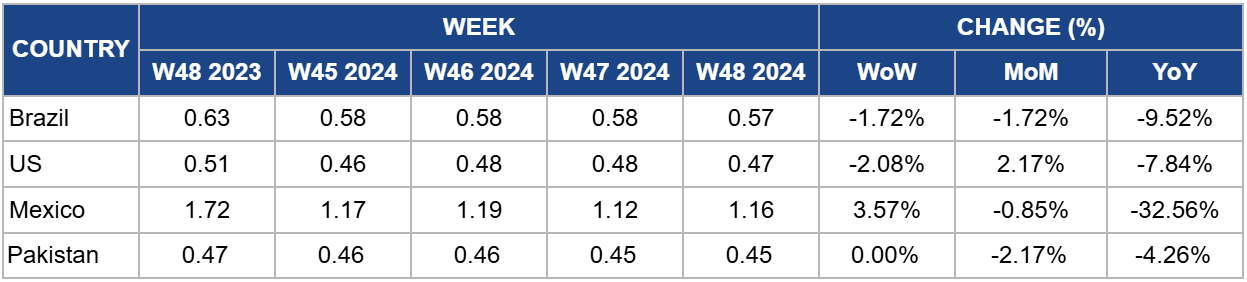

Brazil

Brazil's sugar prices declined to USD 0.57 per kilogram (kg) in W48, a 1.72% week-on-week (WoW) decrease. This price drop reflects a challenging production season, particularly in Brazil's key Center-South region, where sugar production fell by 60% in the first half of Nov-24, marking a significant decline compared to the same period in 2023. Due to drought conditions and a shift towards ethanol production, the reduced sugarcane supply contributed to the 52.8% decrease in sugarcane crushing during this period. Crystal sugar prices in the domestic market decreased by 0.62%, while hydrated ethanol prices slightly increased. The ongoing challenges in the sugar and ethanol sectors will continue impacting domestic and international sugar prices.

United States

The United States (US) sugar prices fell to USD 0.47/kg in W48, marking a 2.08% WoW decrease and a 7.84% year-on-year (YoY) drop. This decline follows USDA projections, which forecast a 2024/25 sugar production reduction to 9.276 mmt, down 2.3% from the previous year. The decrease is due to lower yields and earlier harvests that pulled some production into the 2023/24 season. Despite record-high sugar production in 2023/24, reducing sugar imports and increasing domestic use have strained supply. US sugar stocks are set to drop by 32% from the previous year, creating a shortfall in supply, with ending stocks projected to be below the USDA's target range. Potential solutions include raising the export limit for Mexico under the US-Mexico agreement, increasing tariff-rate quotas, or increasing high-duty imports. The tight supply situation, coupled with a forecasted shortfall could result in upward pressure on US sugar prices in the near future. Should the USDA adjust its forecast in Dec-24 and imports rise, sugar prices might stabilize or even increase as the market reacts to these adjustments.

Mexico

In W48, Mexico's sugar prices rose to USD 1.16/kg, reflecting a 3.57% WoW increase. However, prices have decreased by 32.56% YoY from USD 1.72/kg. This WoW price increase is partly driven by heightened demand for sugarcane during the year-end season, particularly in regions like Querétaro, where sugarcane is a popular snack and ingredient for holiday drinks like punches. The demand for sugarcane could continue to influence local sugar prices, particularly as the harvest season peaks.

Pakistan

Pakistan's sugar prices remained stable at USD 0.45/kg in W48, though they saw a 4.26% decrease compared to 2023. A key development in the sugarcane sector is the growing preference among farmers for manufacturing gurr (jaggery) instead of selling their crops to sugar mills. This shift is driven by the attractive market rates for gurr, which range from USD 25.20 to 29.52/40 kg (PKR 7,000 to 8,200/40 kg), offering farmers more immediate profits compared to the lower prices paid by sugar mills. Despite the government's announcement to begin the cane-crushing season on November 21, local sugar mills have failed to comply with the directive. This has led many farmers, particularly in districts like Muzaffargarh, to set up mobile jaggery production units. These units offer a profitable alternative, as jaggery is sold at nearly double last year's prices. However, farmers continue to express concerns about rising input costs, such as fertilizers and fuel, while sugarcane prices have remained stagnant for the past two years. The increased demand and profitability of gurr production could affect the overall sugar market in Pakistan, potentially reducing the sugarcane supply available for milling. This shift underscores the sugar industry's challenges, which may see supply constraints if the trend continues.

3. Actionable Recommendations

Optimize Export Strategies in Response to Price Fluctuations

Given the projected global sugar deficit for 2024/25 and changing production forecasts, especially in Brazil, stakeholders in sugar production and trading should focus on optimizing their export strategies. Countries facing challenges with reduced sugar production but increased exports should explore new markets or expand existing trade agreements to secure higher export volumes. This will help mitigate domestic supply constraints as weather-related disruptions have impacted Brazil's sugar prices. Additionally, businesses should work closely with global trading firms and enhance logistical operations to prevent disruptions in the sugar supply chain. This could involve strengthening relations with key buyers in emerging markets to capture new growth opportunities.

Diversify Sourcing and Supply Chain Resilience

To hedge against potential supply shortages and price volatility, companies should consider diversifying their sourcing strategies, particularly in countries with growing domestic production, such as Kenya and Thailand. The success of Kenya's sugar self-sufficiency initiative, bolstered by subsidies and improved agricultural practices, presents an opportunity for international stakeholders to explore new sourcing partnerships. Additionally, businesses should actively monitor sugar production in Ukraine and Pakistan, where domestic supply dynamics are shifting. By establishing agreements with multiple suppliers across diverse regions, companies can reduce dependency on any single source and improve their resilience to disruptions caused by weather, policy changes, or production fluctuations.

Invest in Local Production and Technological Advancements

To reduce dependency on imports and enhance domestic sugar production, countries facing supply challenges, like Egypt and the Philippines, should invest in local agricultural advancements and infrastructure. Egypt's project to expand sugarcane cultivation with modern irrigation systems provides a model for improving water efficiency and yields. Other regions should explore similar initiatives, incentivizing farmers to adopt sustainable farming practices and modern irrigation techniques. Government support through subsidies, infrastructure investments, and training programs can foster growth in local sugar production, helping to stabilize supply and ensure long-term self-sufficiency in the face of global market uncertainties.

Sources: Tridge, Vinanet, Agriculture Egypt, Hellenic Shipping News, El Periódico de México, Agro Times, Ukragroconsult, Azteca Querétaro, Dawn