In W7 in the sugar landscape, some of the most relevant trends included:

- The sugar market is transitioning from a deficit to a surplus, with global production expected to rise significantly in MY 2025/26, driven by higher output in key producing countries like Brazil, India, and Thailand.

- Brazil is pushing back against US sugar and ethanol tariffs, signaling potential negotiations for better market access.

- India, Mexico, and Pakistan are experiencing supply challenges due to poor harvests, mill closures, and government interventions, leading to price volatility and production declines.

- Kazakhstan and Nigeria are investing in domestic sugar production to reduce import dependence, with major projects focused on infrastructure, processing capacity, and agricultural expansion.

- Sugar prices fluctuated globally, with Brazil and Pakistan seeing declines, while the US and India experienced short-term increases

1. Weekly News

Global

Global Sugar Surplus Expected in 2025/26 as Production Rises

Global sugar supply is forecasted to shift to a surplus of 2.7 million metric tons (mt) in the 2025/26 marketing year (MY), following a deficit of 3.7 mmt in MY 2024/25, according to Green Pool analysts, an independent agribusiness research firm. World sugar production is projected to rise by 4.5% to 202 mmt, the second-largest output on record, driven by higher production in Brazil, India, and Thailand.

Brazil

Brazil Criticizes Potential US Ethanol Tariff, Calls for Greater Sugar Market Access

Brazil's Mines and Energy Minister criticized a potential United States (US) tariff increase on Brazilian ethanol, calling it unreasonable unless accompanied by greater access for Brazilian sugar exports. His comments follow US plans to raise tariffs on several imports, citing Brazil's 18% ethanol tariff as an example of unfair trade. In addition, he pointed out that US sugar tariffs, at USD 360 per metric ton (mt) outside preferential quotas, equate to an 81.2% tax, effectively limiting Brazilian exports. While Brazil is a major sugar producer, its US export quota remains small. The announcement could prompt negotiations, with Brazil signaling openness to discussions.

India

India's Sugar Supply Tightens as Mill Closures Drive Prices Higher

India's sugar market faces tightening supply and rising prices as early mill closures and poor harvest conditions reduce output. Over 30 mills, mainly in Maharashtra, Karnataka, and Uttar Pradesh, shut down nearly two months early due to adverse weather, pushing domestic sugar prices up 10% month-on-month (MoM). The government's approval of 1 mmt in exports has further constrained availability, raising concerns about meeting the quota. Analysts estimate 2024/25 sugar production could fall 14.7% to 27.27 mmt, with some predicting a drop to 26 mmt. Exports remain slow, as mills delay contracts, expecting higher prices.

Kazakhstan

Kazakhstan to Build New Sugar Factory in Atyrau Region to Reduce Import Dependence

Led by Goldbridge International, a global investment and development firm, Kazakhstan will construct a new sugar factory in the Atyrau Regio, with completion expected by summer 2026. The USD 112.9 million project, primarily funded by a Chinese investor, aims to reduce Kazakhstan's dependence on sugar imports by producing 144,000 mt annually. The facility will require 900,000 mt of raw materials per year, with agreements underway for local sugar beet cultivation. The project is expected to create 200 jobs and boost regional agriculture, with strong support from local authorities who emphasize its role in enhancing food security and economic development.

Nigeria

Nigeria's Sugar Market Poised for Growth, but Faces Challenges in Achieving Self-Sufficiency by 2030

Driven by rising domestic demand and favorable government policies, Nigeria's sugar market is expected to grow significantly, potentially surpassing USD 2.5 billion by 2030. However, the sector faces several challenges, including climate change impacts, poor infrastructure, outdated farming practices, and limited sugar processing capacity. Experts advocate for government and industry collaboration to enhance productivity, expand processing facilities, and foster a supportive environment for local producers. They recommend supporting research on high-yielding sugarcane varieties, encouraging private investment, and improving security in sugar-producing regions. Nigeria requires a USD 5 billion investment to achieve self-sufficiency, as current production falls significantly short of local consumption needs.

2. Weekly Pricing

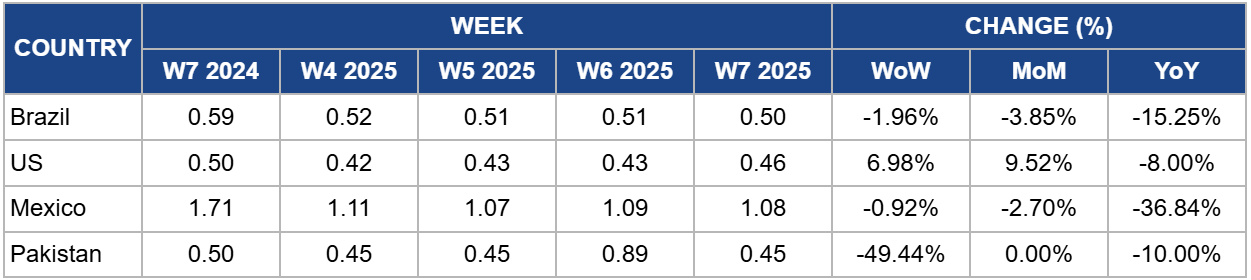

Weekly Sugar Pricing Important Producers (USD/kg)

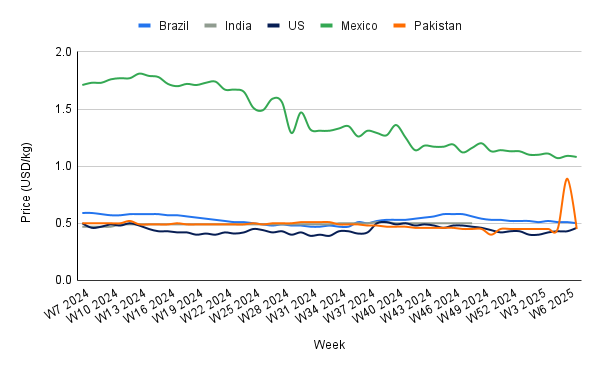

Yearly Change in Sugar Pricing Important Producers (W7 2024 to W7 2025)

Brazil

Brazil's sugar prices decreased to USD 0.50/kg in W7, reflecting a 1.96% week-on-week (WoW) drop and a 15.25% year-on-year (YoY) decline. Despite a favorable recovery in the 2025/26 crop, boosted by improved soil moisture and rainfall, analysts caution that the poor condition of sugarcane in 2024 may limit production increases, preventing a return to 2023/24 levels. Sugar availability in Brazil's center-south region is expected to rise due to a higher sugar mix and increased raw material, though reduced planted areas could limit total supply. Weather conditions in 2025 are forecasted to support a healthy crop, but a delayed crushing start may impact export timing, with prices potentially adjusting once crushing peaks.

United States

US sugar prices have recently risen by 6.98% WoW and 9.52% MoM, reaching USD 0.46/kg. However, despite this increase, the overall outlook for sugar prices in the US remains stable due to a combination of market factors. Sugar consumption in the US is projected to decline for the third consecutive year in the 2024/25 season, with a 2.7% drop expected. This decline is attributed to changing consumer habits and the growing adoption of GLP-1 weight-loss drugs, which are reducing sugar intake.

Despite this decreased demand, US sugar production is forecasted to hit a record 9.37 mmt, ensuring an ample supply. This increase in domestic production is expected to reduce the need for imports, which are anticipated to fall to 2.89 mmt, down from 3.81 mmt in the previous season. As a result, the sugar stocks-to-use ratio is projected to rise to 15.3%, well above the United States Department of Agriculture (USDA) benchmark of 13.5%, indicating a well-supplied market. While prices have increased in the short term, the combination of lower demand and higher production is expected to prevent significant price fluctuations, keeping the market stable in the near future.

Mexico

In W7, Mexico's sugar prices increased to USD 1.08/kg, marking a 0.92% weekly increase but a sharp 36.84% YoY decline. The sugar industry in Puebla, particularly in the Sierra Negra region, has faced significant disruptions due to the temporary closure of the Calipam sugar mill in Coxcatlán. A strike over unpaid wages led to an 89.42% drop in sugarcane production in the region, with harvested land shrinking from 1,417 hectares (ha) in 2023 to 150 ha in 2024. Despite this decline, sugarcane production in Puebla's Mixteca region expanded, with 6,440 ha harvested in 2024.

Puebla's planted sugarcane area grew 0.89% to 18,606 ha in 2024, but only 35% was harvested, leading to a 60.63% drop in output. The closure of the Calipam sugar mill disrupted production, underscoring vulnerabilities in Mexico's sugar supply chain. While regional supply constraints may cause localized price volatility, stable output in other areas and a global surplus should limit significant national price increases.

Pakistan

Pakistan's sugar prices declined to USD 0.45/kg in W7, reflecting a 49.44% WoW drop and a 10% yearly decrease. Despite this, domestic retail prices have risen in recent months due an artificial shortage linked to exports, prompting government intervention. Authorities are implementing district-wide distribution plans and price monitoring, particularly ahead of Ramadan, to ensure stable supply and affordability. Pakistan holds a sugar surplus of 1.7 mmt, with 750,000 mt approved for export. While price caps and taxation policies may help control costs, future prices will depend on global market conditions and the government’s ability to balance exports with domestic supply stability.

3. Actionable Recommendations

Leverage Brazil's Improved Sugar Outlook for Export Expansion

Given Brazil's projected sugar surplus in the 2025/26 season, fueled by a robust recovery and favorable weather conditions, sugar exporters should capitalize on this opportunity by strengthening trade relationships with key importers, including the US. Negotiating more favorable export quotas, especially in light of ongoing US tariff discussions, will help Brazilian producers expand market access. Exporters should prepare for potential shifts in US tariff policies by ensuring flexible contract terms and by securing alternative markets in Asia and Africa, where demand for sugar is rising.

Adapt to India's Tightening Sugar Market by Exploring Alternative Sourcing

India's sugar market faces tightening supply due to weather-related disruptions and early mill closures. Importers should consider diversifying their sugar sourcing by looking beyond India and exploring opportunities in Brazil, Thailand, or other emerging sugar markets. Additionally, collaborating with Indian producers on long-term contracts could help mitigate potential price volatility, ensuring a steady supply of sugar while managing rising costs. Furthermore, stakeholders should monitor the progress of India's export restrictions, as they could further influence domestic availability and pricing.

Build Strategic Sugar Reserves in Response to Global Price Fluctuations

Given fluctuating sugar prices across markets like Mexico, Pakistan, and the US, both private and government entities need to invest in strategic sugar reserves. For instance, Pakistan's surplus presents an opportunity to stockpile sugar at lower prices before Ramadan-related demand peaks. Similarly, regions facing production disruptions, such as Mexico's Sierra Negra area, should implement measures to ensure domestic stocks remain sufficient. Investing in storage infrastructure and coordinating with local producers can stabilize supply and mitigate price spikes during periods of high demand.

Sources: Tridge, Noticias Agricolas, Agro Perú, Ukr AgroConsult, Agro Info, Chem Analyst News, Chini Mandi, Investing, El Sol de Puebla