August Outlook Report: Nuts and Oils

Market Intelligence Analytics Team, Theo Venter

Published Jul 29, 2023

PDF File Preview

- In India, high peanut prices persist due to strong local and international demand, despite predictions of a bumper crop in 2023. Early planting, allowed by June's Cyclone Biparjoy, may counter potential El Niño-induced droughts. In Brazil, peanut prices have continued to increase, despite becoming less competitive, leading to lower-than-expected volumes being exported. Chinese peanut prices moved sideways, as demand has been slow in recent months, with buyers already covered until the new crop comes in.

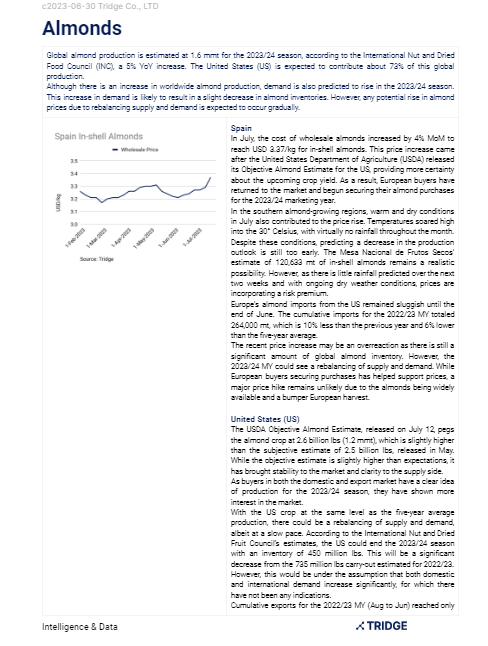

- Global almond production is estimated at 1.6 mmt for the 2023/24 season, according to the International Nut and Dried Food Council (INC), a 5% YoY increase. The United States (US) is expected to contribute about 73% of this global production. Although there is an increase in worldwide almond production, demand is also predicted to rise in the 2023/24 season. This increase in demand is likely to result in a slight decrease in almond inventories. However, any potential rise in almond prices due to rebalancing supply and demand is expected to occur gradually.

- As the 2022/23 MY in the Northern Hemisphere is winding down, lackluster demand for walnuts continues, especially coming from Europe. Stronger demand for larger-sized walnuts has benefitted Chile. The focus is turning to the 2023 harvest, with buyers slowly fixing contracts for the new crop.

- Buyers and importers are mostly covered for the remainder of the 2022/23 MY and are mostly interested in new crop purchases. The Northern Hemisphere harvest will start in August. Prices in Türkiye have continued to decrease in USD terms due to a weakening of the domestic currency. This could trigger more buying of old-crop hazelnuts as prices are significantly low. The large carry-over stocks in Türkiye and another large global crop in 2023 could keep prices under downward pressure.

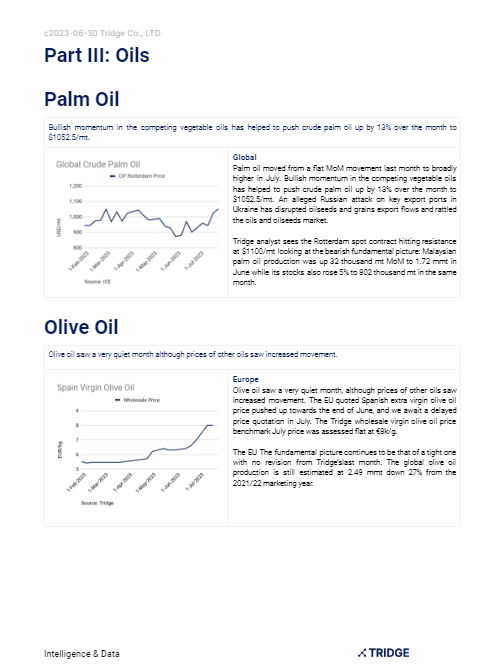

- Bullish momentum in the competing vegetable oils has helped to push crude palm oil up by 13% over the month to $1052.5/mt.

- Olive oil saw a very quiet month although prices of other oils saw increased movement.

- Rapeseed ended the month higher at an average price of €457/mt, €20 up from the average price the previous month.

- Sunflower oil has also traded up over the month under review. It ended the month at $61 up to finish at $945/mt.

- Global almond production is estimated at 1.6 mmt for the 2023/24 season, according to the International Nut and Dried Food Council (INC), a 5% YoY increase. The United States (US) is expected to contribute about 73% of this global production. Although there is an increase in worldwide almond production, demand is also predicted to rise in the 2023/24 season. This increase in demand is likely to result in a slight decrease in almond inventories. However, any potential rise in almond prices due to rebalancing supply and demand is expected to occur gradually.

- As the 2022/23 MY in the Northern Hemisphere is winding down, lackluster demand for walnuts continues, especially coming from Europe. Stronger demand for larger-sized walnuts has benefitted Chile. The focus is turning to the 2023 harvest, with buyers slowly fixing contracts for the new crop.

- Buyers and importers are mostly covered for the remainder of the 2022/23 MY and are mostly interested in new crop purchases. The Northern Hemisphere harvest will start in August. Prices in Türkiye have continued to decrease in USD terms due to a weakening of the domestic currency. This could trigger more buying of old-crop hazelnuts as prices are significantly low. The large carry-over stocks in Türkiye and another large global crop in 2023 could keep prices under downward pressure.

- Bullish momentum in the competing vegetable oils has helped to push crude palm oil up by 13% over the month to $1052.5/mt.

- Olive oil saw a very quiet month although prices of other oils saw increased movement.

- Rapeseed ended the month higher at an average price of €457/mt, €20 up from the average price the previous month.

- Sunflower oil has also traded up over the month under review. It ended the month at $61 up to finish at $945/mt.

Table of Content

Part I: Key Indicators

Part II: Nuts

- Peanuts

- Almonds

- Walnuts

- Hazelnuts

Part III: Oils

- Palm Oil

- Olive Oil

- Rapeseed Oil

- Sunflower Oil

Related market data

Read more relevant content

By clicking “Accept Cookies,” I agree to provide cookies for statistical and personalized preference purposes. To learn more about our cookies, please read our Privacy Policy.

By clicking “Accept Cookies,” I agree to provide cookies for statistical and personalized preference purposes. To learn more about our cookies, please read our Privacy Policy.