Argentine apple and pear forecast for MY 2020/21

Argentinian Apples

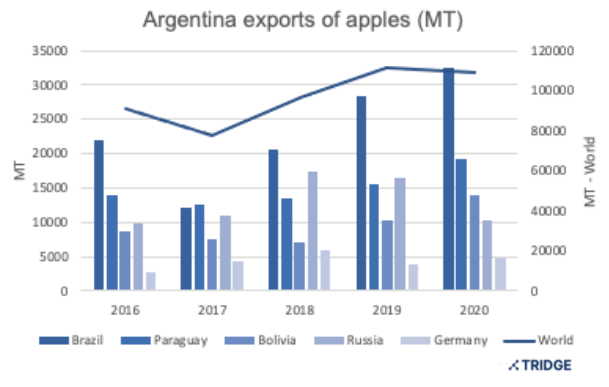

Argentina is the third-largest exporter of apples in the Americas, coming after the US and Chile. The main countries that imported Argentinian apples in 2020 were Brazil (33.3%), Bolivia (8.6%), Russia (8.4%), Germany (6.6%), and Paraguay (5.8%). For MY 2020/21, the USDA post-harvest forecast on apples was revised to 560 thousand MT, which is 10 thousand MT less than the initial forecast and 6.7% less compared to last year’s volume. The exports are expected to fall 9% on YoY comparison as apple production volume in the Northern Hemisphere is likely to increase in the 2020/21 season. On the other hand, Brazil that imported over 32 thousand MT in 2020 might face less availability when it starts to import with this decrease in production.

The decrease in production is attributable to the reduction in the planted area. More than 40% of the apple orchards have been replaced with other more profitable crops such as vineyards, alfalfa, or corn. Only in the last two years, the harvesting area has decreased by 6.7%. The decrease is also related to the economic difficulties in keeping apple orchards, as currency fluctuations increased the prices of agricultural inputs needed for the crop.

The main varieties planted are the Red Delicious (65%), Granny Smith (13%), Gala (12%), and others (10%) with the peak of the harvesting period is between March and August, but with a year-round availability with smaller volumes.

Source: Tridge, Ministry of Agroindustry of Argentina, USDA

Argentinian Pear

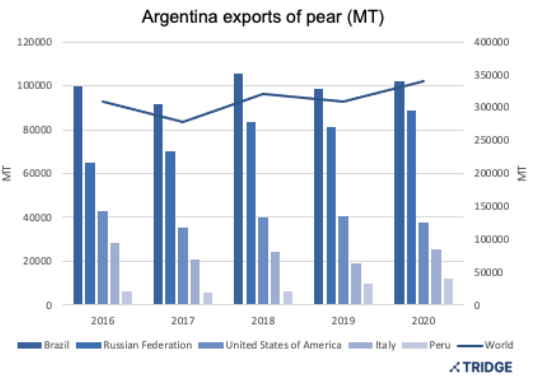

On the other hand, the post-harvest forecast for Argentinian pear production increased 10 thousand MT than initially expected to 620 thousand MT. However, the production volume is still low compared to last year, showing l a decrease of 3.1%. The increase in forecast production is due to the good weather conditions and a smaller than expected damage by hail at the beginning of the year. The export volume remains unchanged from the previous forecast at 320 thousand MT, decreasing 5.9% compared to the previous MY. On export volume, Argentina is the third-largest global exporter, with the main importers being Brazil (26.2%), Russia (23.2%), and the US (14.1%). The main varieties are William (40%) with production between January and July, Packham (29%), with the seasonality starting from February to December.

Source: Tridge, Ministry of Agroindustry of Argentina, USDA

Export and price trend of Argentinian apples and pears

For the first half, Argentinian apples and pears exports are mainly exported to the US, Russia, and the EU. Exports to the EU are highly preferred for the exporters due to the higher prices as higher quality fruits are demanded. But the competition with other deciduous fruit producers in the Southern countries has been hard for the Argentinian producers. Recently, they are experiencing an increase in production costs primarily due to the devaluation of the Argentinian peso. The Russian and Mercosur are less demanding on quality and have a larger demand for second-quality fruits and consequently have lower pricing.

In March 2021, the FOB price for Argentine apple was quoted at USD 605 per MT, showing an MoM increase of 12.5%. The pear prices also decreased compared to the previous year. Pear with Argentinian origin was quoted USD 695 per MT, which is an increase of 1.3% compared to February, but compared to last March; it is decreased by 17.5%. The decrease in pricing of both fruits in 2021 is related mainly to the devaluation of Argentinian pesos and main sales to Mercosur. But prices will start to rise once the sales to the EU and the US beginning in April, achieving the highest price in the season before subsiding again.

Sources:

- Argentina Government. Translated from Spanish. “Harvest calendar”.

- Argentina Government. Translated from Spanish. “Market profile of Apples and Pears”

- Argentina Government. Translated from Spanish. “Monthly statistics”

- EfeAgro. Translated from Spanish. “Argentinian harvest of pears and apples will increase to 1.18 million MT in 2020/21”.

- USDA. “Fresh Deciduous Fruit Semi-Annual”