Colombian Coffee Industry's Missed Opportunity

Colombian coffee industry as the backbone of Colombian agriculture

When it comes to a cup of coffee, you are an outlander if you have not had a cup of Colombian coffee. Not only known for its excellence in quality, but also for its culture and history, the Colombian coffee industry plays an important role in Colombia’s economy. In fact, over 540,000 small-family-owned coffee farms spanning 23 departments comprise the Colombian coffee industry and represent 69% of the total production in Colombia. It is estimated that about 2 million people in Colombia rely on the coffee industry to make a living. According to the National Federation of Coffee Growers of Colombia (FNC), the coffee industry’s Gross Domestic Product (GDP) grew by 21.4% (agricultural GDP - 3.3%; national GDP - 1.1%) in the first quarter of 2021, proving its strong presence in the Colombian economy as a whole.

Colombia is the world’s largest producer of Arabica and the third-largest producer of coffee in the world. That is, Colombia produces the most premium quality coffee amongst its major competitors, Brazil and Vietnam. Among the top three exporters of coffee (HS code 090111), Colombia’s unit value far exceeds that of Brazil and Vietnam as shown in the chart below, reflecting the Colombian premium.

Triumph over the pandemic

In 2020, amidst COVID-19, the Colombian coffee industry successfully overcame pandemic challenges through implementing preemptive sanitary measures and a campaign that redirected unemployed local laborers from other industries to fill in the labor gap. While the original projection estimated total production at 13.8 million 60-kg bags, MY 2019/2020 ended with 14.1 million bags, a 2% increase from MY 2018/19 (13.8 million). Since then, Colombia’s coffee production has remained steady and has marked a 2.9% rebound from 8.2 million to 8.4 million during the first seven months of MY 2019/20 and 2020/21, respectively. USDA has projected MY 2020/21 to end with a total production of 14.3 million bags.

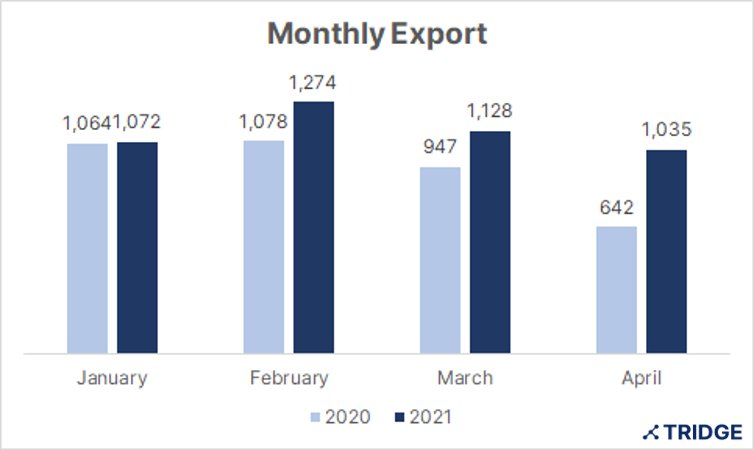

A similar trend applies to exports. MY 2020/21 export (estimated 13.8 million) is projected to see a 6% increase in total export compared to that of MY 2019/20 (13.0 million). Monthly reports by FNC support such trends as well. Compared to 2020, the first four months of 2021 marked a 21% growth with April’s growth peaking at a 61% increase from the previous year.

(USDA's Marketing Years refer to October - September for Colombian coffee)

Current & future challenges ahead

However, it is maybe too early to celebrate. The Colombian coffee industry in 2021 is currently facing both production and export challenges. In terms of production, while MY 2020/21 is expected to end strong with continuous growth in monthly production volume, the projection for early MY 2021/22 harvest is in question due to unfavorable weather conditions.

In long term, climate change affects coffee production in two major ways, production volume and bean quality. Changes in temperature and precipitation directly impact productivity by damaging the flowering stage of coffee beans and indirectly by lowering harvest altitude for which high-altitude is known to be beneficial. Furthermore, climate change makes coffee crops more susceptible to pests, inducing increased use of pesticides and soil pollution and consequently altering beans’ quality and flavor. While FNC has recommended coffee farmers to plant pest-resistant variants to prevent future production damages from climate change, due to its small-family-owned nature, Colombian coffee farmers would need organizational support from entities, such as FNC and the government, to combat the upcoming challenges.

This year, Colombia has seen higher than average precipitation in March and April 2021, likely affecting the harvest in the first half of MY 2021/22, consequently slowing down the industry’s momentum for recovery. Lower production will also most likely reduce export volume.Brazil, Colombia’s major competitor for coffee export, is also experiencing production challenges resulting from climate change for the coming MY.

What is more is the ongoing national protests that began on April 28th, 2021. Although MY 2020/21 has seen an increase in production, it is now confronting domestic level supply chain disruptions. Current national protests were sparked by the tax reform proposed by the government in an effort to overcome the economic crisis. Since then, rock blockades and vandalism by protestors have halted all movements of coffee bags within the country, including lootings at warehouses for coffee at port Buenaventura where 70% of the country’s coffee gets exported.

As cargoes for shipment could neither enter nor leave the port due to blockades, exports of coffee beans have been delayed for 4-5 weeks. As a result, FNC reported a 52% drop in coffee exports in May 2021 (427,000 60-kg bags) compared to the same month in 2020 (894,000 bags). Fortunately, it was reported that Colombia’s coffee export was still able to sustain a 7% increase in the first five months of 2021 compared to the same period last year.

Colombia’s political unsettlement may pose a long-term economic threat to the country’s coffee industry. Road blockades not only have disrupted the domestic supply chain but also may have forced some importers to replace Colombian coffee with coffee from other countries due to prolonged delay in supply.

Wonjin Suh, a current deal manager for Colombian under grade (UG) coffee beans at Tridge, informed that his supplier has been able to re-route the shipments to port Cartagena for the export of UG coffee beans. While re-routing to port Cartagena is expected to relieve the situation to an extent, it still presents several problems, such as higher logistics cost due to increased travel distance to the port and congestion at port Cartagena as shipments to port Buenaventura are being redirected to port Cartagena.

A missed opportunity

As such, although Brazil’s struggle with low production due to severe drought and increasing demand for coffee beans to fill up the shortage in the international market are contributing to high international coffee prices, the Colombian coffee industry has not been able to take full advantage of the opportunity due to the aforementioned domestic challenges. New York stock price for arabica coffee beans in May peaked at USD 1.896/lb, a three-year high, which is a 21.62% increase compared to May 2020. Jose Caballero, Country Manager at Tridge in Colombia, has informed that prolonged national protests have led main coffee mill warehouses to stop their operations and a decrease in sales volumes for exporters in May. Though exact estimates for losses are yet to be announced, about 700,000 - 800,000 bags have been estimated to have been stuck. A 52% reduction in May export volume and continuing national protests pose some question marks for the Colombian coffee industry’s successful recovery. In fact, coffee roasters may shift to coffee beans from other countries to fulfill their demand. The offbeat between production recovery and export challenge for MY 2020/21 will determine the Colombian coffee industry’s growth direction.

Sources:

- AgroForumPeru. “Some 800,000 bags of Colombian coffee for export, blocked in May due to protests”.

- MXContexto. “Blockades and unemployment will halt the growth of the agricultural sector”.

- National Federation of Coffee Growers of Colombia. “Coffee grows 21.4% in the first quarter and marks the agricultural GDP of 3.3%”

- National Federation of Coffee Growers of Colombia. “Colombian coffee exports fall 52% in May”.

- National Federation of Coffee Growers of Colombia. "FNC warns of more aggressive races and new variants of rust in Colombia".

- Reuters. “Update 1-U.S. coffee importer sees delay of up to 5 weeks on Colombian cargos”.

- The Coffee Hunters. “Colombia update”.

- USDA. “Colombia: Coffee Annual”.

- YCharts. “New York Arabica Coffee Price".