W10 2025: Potato Weekly Update

.jpg)

In W10 in the potato landscape, some of the most relevant trends included:

- Farmers in Boyacá, Colombia, are shifting to dairy farming due to high costs, labor shortages, and competition from imports despite a strong 2024 harvest.

- Driven by competitive pricing and seasonal demand, Egypt shipped 156 thousand mt of potatoes in MY 2023/24, which accounted for 65% of Greece’s imports.

- Ukraine's potato prices fell WoW but remained 18% higher YoY, with producers expecting a rebound due to limited high-quality stocks. France and Germany saw MoM price increases due to supply constraints, while Egypt and Pakistan experienced declines due to oversupply.

1. Weekly News

Colombia

Colombia’s Potato Sector Faces Crisis Amid High Costs and Low Profitability

In Colombia, producers are abandoning their potato crops in favor of livestock farming due to a lack of profitability. Despite a good harvest in 2024, farmers struggled to make significant profits and criticized the lack of government support and competition from processed potato imports.

Potato production in Boyacá is in crisis as high production costs, labor shortages, free trade agreements, and the absence of irrigation infrastructure push farmers toward other economic activities, mainly dairy production. With limited government support, many have found it increasingly difficult to sustain their livelihoods in potato farming.

Egypt

Egypt’s Potato Exports to Greece Hit Record 156 Thousand MT in MY 2023/24

Egypt has boosted its potato exports to Greece, reaching a record 156 thousand metric tons (mt) in the 2023/24 marketing year (MY), with a total value of USD 64 million. This represents a 12% increase from the previous season and a 71% surge from 2021/22. Greece remains Egypt's second-largest potato market after Russia. Egyptian exporters ship the highest volumes to Greece between February and April when Greek stocks are low. Since 2002, Egypt has dominated Greece's potato imports, leveraging cost-effective logistics and competitive pricing. In MY 2023/24, Egyptian potatoes accounted for 65% of Greece’s total imports, while France and Cyprus supplied 12.8% and 9.1%, respectively. Rising domestic consumption in Greece and re-exports continue to drive demand for Egyptian potatoes.

India

West Bengal’s Potato Farmers Face Crisis Despite Record Production in 2025

Potato farmers in West Bengal struggle with a severe economic crisis despite achieving record-high production levels in 2025. The state produced an unprecedented 14 million metric tons (mmt) of potatoes, yet farmers cannot secure fair prices for their crops. In the Bankura district, traders purchase Pokhraj potatoes at just USD 6.32 per quintal in W10, far below production costs causing significant losses. The situation worsens as Jyoti potatoes, the state's most widely cultivated variety, also sell at disappointingly low prices. Although the West Bengal government set a procurement price of USD 10.34 per quintal for Jyoti potatoes, farmers remain worried about unsold stocks.

Ukraine

Ukraine’s Potato Prices Declined in W10 but Remained Above 2024 Levels

In W10, Ukrainian farmers sold potatoes at USD 0.43 to 0.67 per kilogram (kg), lower than 10% week-on-week (WoW). The price drop followed a surge in potato prices the previous week, which led buyers to resist purchasing at higher rates. Despite the decline, potato prices in Ukraine remain 18% higher than in early Mar-24. Some producers believe this downturn is temporary, citing a shortage of high-quality potatoes as household and commercial stocks continued shrinking. Meanwhile, the Ministry of Finance notes that inflation will rise in the coming months due to poor harvest in 2024 and increasing production costs for enterprises.

2. Weekly Pricing

Weekly Potato Pricing Important Exporters (USD/kg)

Yearly Change in Potato Pricing Important Exporters (W10 2024 to W10 2025)

France

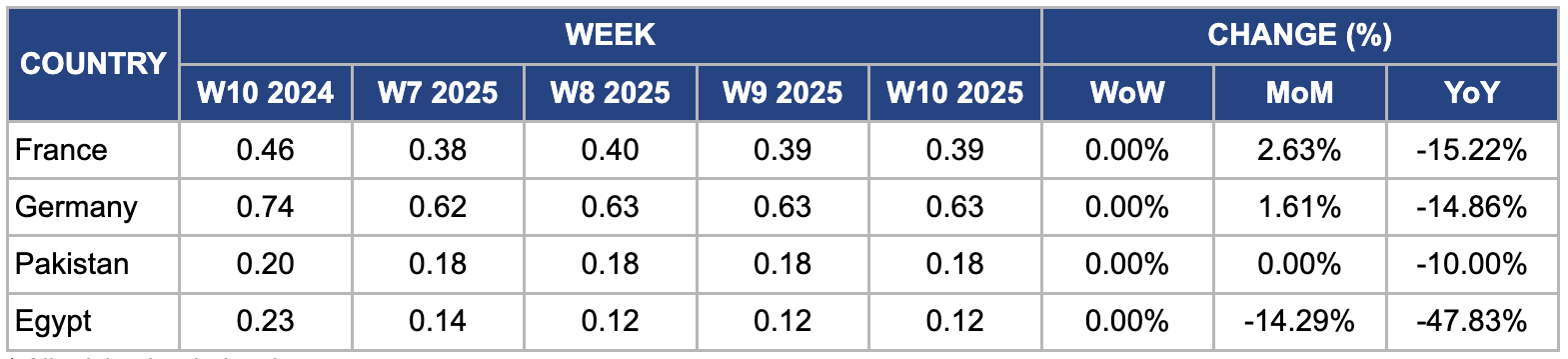

In W10, France’s potato prices remained unchanged WoW but increased 2.63% month-on-month (MoM) to USD 0.39/kg. This MoM increase was due to reduced market availability following lower-than-expected storage volumes from the 2024 harvest, which totaled approximately 7.9 mmt, down from 8.3 mmt in 2023. Furthermore, persistent rainfall in key production regions such as Hauts-de-France and Normandy in Feb-25 caused logistical delays, limiting fresh supply to the market. Meanwhile, steady demand from processors and exporters, particularly Spain and Italy, supported prices.

Germany

In W10, German potato prices remained unchanged WoW but rose 1.61% MoM to USD 0.63/kg. This price increase over the past month is due to high demand outpacing supply. According to the Lower Saxony Chamber of Agriculture, processors from neighboring countries, particularly the Netherlands and Belgium, have ramped up purchases, tightening available stocks. Moreover, due to adverse weather conditions affecting yields, Germany’s 2024 potato harvest was estimated at around 10.3 mmt, lower than the 10.7 mmt recorded in 2023. With limited free-market industrial potatoes available and domestic contract obligations prioritized, supply constraints continue to exert upward pressure on prices. Farmers expect prices to remain firm as demand from processors persists.

Pakistan

In W10, Pakistan's potato prices remained stable WoW and MoM but dropped 10% year-on-year (YoY) to USD 0.18/kg from USD 0.20/kg in W10 2024. The ongoing harvest in Punjab, Pakistan’s key potato-producing region, has increased supply, driving prices down. Higher acreage and improved yields have boosted market availability while easing inflation and stable input costs, particularly for fertilizers and fuel, have lowered production expenses. Furthermore, weaker export demand and improved domestic distribution have kept the market well-supplied, preventing price surges.

Egypt

In W10, Egypt’s potato prices remained stable WoW but declined 14.29% MoM and 47.83% YoY, continuing the recent downward trend due to increased supply from the ongoing Nile season harvest. Top-producing governorates, including Minya, Dakahlia, Beheira, and Menoufia, have boosted domestic market availability, intensifying oversupply pressure. Moreover, weaker export demand and seasonal price fluctuations have accelerated the decline. However, market stabilization could occur in the coming weeks as demand adjusts to shifting supply levels and post-harvest storage slows market inflows.

3. Actionable Recommendations

Strengthen Local Market Support to Improve Potato Profitability in Colombia

Potato producers in Colombia, particularly in Boyacá, are abandoning the crop due to high production costs, labor shortages, and competition from processed potato imports. To counteract this trend, cooperatives and agricultural organizations should focus on strengthening local market access through direct farm-to-consumer sales, regional branding, and improved logistics. Establishing cooperatives or farmer-led distribution networks can reduce dependency on intermediaries, ensuring farmers receive higher margins. Moreover, promoting value-added potato products, such as frozen or processed potato items, can create new revenue streams and improve competitiveness against imported alternatives. By fostering local demand and reducing reliance on bulk commodity sales, Colombian potato farmers can enhance profitability and sustain production in the long term.

Expand Egypt’s Export Market Beyond Traditional Destinations

Egypt's record-breaking potato exports to Greece highlight the country's dominance in supplying the Greek market. However, to mitigate risks associated with over-reliance on a few key markets like Greece and Russia, Egyptian exporters should actively explore new trade partnerships in high-demand regions such as the Middle East and Asia. Countries like the United Arab Emirates, Saudi Arabia, and India have a growing demand for fresh and processed potatoes, presenting opportunities for market expansion. Moreover, securing long-term contracts with retailers and food processors in these new markets can stabilize and reduce vulnerability to seasonal fluctuations. By diversifying export destinations and strengthening trade agreements, Egypt can maintain steady growth in its potato exports while reducing dependency on a limited number of buyers.

Improve Storage and Market Coordination to Stabilize Prices in West Bengal

Despite record-high potato production in West Bengal, farmers experienced severe financial losses due to low farm-gate prices. One way to mitigate this crisis is by improving post-harvest storage and better coordinating market supply. Encouraging investment in modern cold storage facilities would allow farmers to store their produce during periods of oversupply and sell when prices are more favorable. Furthermore, implementing a structured procurement system, where farmer cooperatives negotiate better prices directly with bulk buyers, could help stabilize income levels. Regional price monitoring and predictive analytics could also guide farmers on optimal selling periods to avoid price crashes. By addressing storage limitations and improving market timing, West Bengal’s potato farmers can achieve more sustainable earnings despite fluctuating production levels.

Sources: Tridge, Potato Pro, The Wire