.jpg)

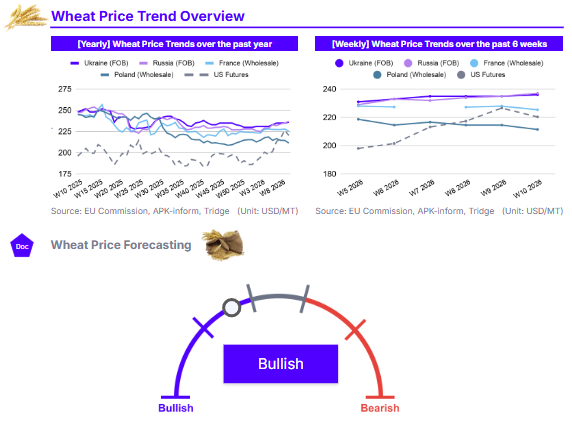

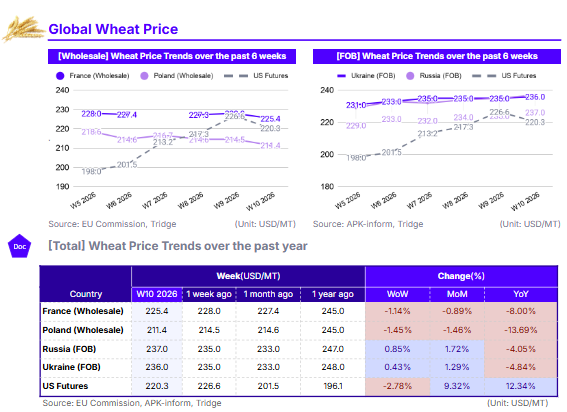

As of W10 2026, the global wheat market is increasingly shaped by escalating geopolitical tensions in the Middle East, specifically the conflict involving the US and Iran. While long-term prices remain down YoY in most regions due to the record 2025 harvest, short-term metrics show significant volatility. US Futures, despite a 2.78% WoW correction to USD 220.3/mt, have surged 12.34% YoY and 9.32% MoM. In the Black Sea, Russian and Ukrainian FOB prices rose MoM by 1.72% and 1.29% respectively, trading in a narrow band as risk premiums offset high supply. Conversely, Polish and French markets fell in USD terms due to dollar strength, despite slight gains in Euro terms. The March WASDE report lowered global ending stocks to 276.7 mmt while raising global consumption to a record 824.8 mmt. Sourcing should focus on Poland for cost-competitive EU supply and the Black Sea for price-aligned volume, provided maritime risks are managed.

1. Weekly Price Overview

Geopolitical Tensions in the Middle East Drive Short-Term Gains Amid Currency Fluctuations

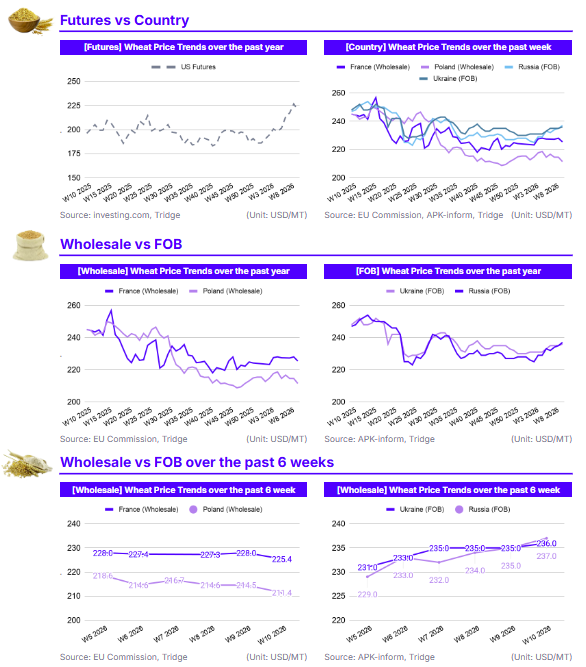

W10 2026 shows a market highly reactive to escalating geopolitical tensions in the Middle East, despite divergent price movements across regions. In Russia, the Free on Board (FOB) price rose 0.85% week-on-week (WoW) to USD 237 per metric ton (mt), while Ukraine’s FOB price followed a similar trajectory, increasing 0.43% WoW to USD 236/mt. These increases are primarily attributed to heightened risk premiums following the outbreak of conflict involving the United States (US) and Iran, which has sparked concerns over maritime security and logistical stability in the broader region.

Conversely, Western European wholesale markets appeared to decline in USD terms, though this was largely a function of USD strength against the Euro rather than local market weakness. In France, the wholesale price was USD 225.4/mt, a decline of 1.14% WoW, while Poland’s wholesale price dropped 1.45% WoW to USD 211.4/mt. In Euro terms, both markets actually saw modest gains, approximately EUR 1.0 in France and EUR 0.5 in Poland, driven by the same Middle Eastern geopolitical tensions. However, a strengthening US Dollar (USD) against the Euro (EUR) ultimately resulted in lower reported prices in dollar terms. US Futures experienced the sharpest correction, falling 2.78% WoW to USD 220.3/mt. This decline represents a market stabilization after futures reached multi-month highs in late Feb-26, as the initial shock of the US-Iran conflict was priced in and profit-taking ensued.

2. Price Analysis

US Futures Bucking the Trend of Relatively Stability in European and Black Sea Markets

The long-term price analysis for W10 2026 reveals a significant divergence between US and European markets, exacerbated by escalating conflict in the Middle East. In the US, wheat futures surged 12.34% year-on-year (YoY) to USD 220.3/mt, while posting a substantial 9.32% month-on-month (MoM) increase. US wheat futures have surged USD 35 since the start of the year, fueled by lower global ending stocks of 276.96 mmt, as supported by the Mar-26 World Agricultural Supply and Demand Estimates (WASDE) report. This sharp rally was further exacerbated by the outbreak of conflict between the US and Iran, which drove futures to multi-month highs in late February before the recent weekly correction.

Conversely, European markets continue to struggle under the weight of the record 2025 global harvest. In Poland, the wholesale price dropped 13.69% YoY to USD 211.4/mt, reflecting a 1.46% MoM decline. Similarly, France’s wholesale price of USD 225.4/mt is down 8% YoY. While both European markets saw slight MoM stability in local currency, the strengthening US Dollar (USD) has masked these gains in dollar terms.

In the Black Sea region, Russia’s FOB price of USD 237/mt reflects a 4.05% YoY decline, despite a 1.72% MoM increase. The recent MoM strength is a result of logistical disruptions at Black Sea ports, but the YoY decline highlights the impact of Russia's large 2025 production levels coupled with high global supplies. Ukraine’s FOB price followed a similar pattern, down 4.84% YoY to USD 236/mt but up 0.43% MoM due to tightening domestic supply and increased seasonal demand. The recent increase in both countries are exacerbated by the ongoing conflict in the Middle East.

3. Strategic Recommendations

Capitalize on Black Sea Price Convergence But Beware Geopolitical Risks

For importers and large-scale processors able to manage significant logistical and geopolitical uncertainty, the Black Sea region currently offers a unique pricing environment where Russian and Ukrainian wheat are trading in an unusually narrow band. In W10 2026, Russia’s FOB price stands at USD 237/mt, while Ukraine’s FOB price is nearly identical at USD 236/mt. This narrow spread is a departure from the discounts seen in Russian origins in Q4-25 and creates a simplified procurement landscape for buyers seeking wheat from the Black Sea region. However, buyers must factor in the volatility of shipping through the Black Sea, as geopolitical tensions and maritime security risks can lead to sudden spikes in freight insurance and delivery delays. It is recommended to secure flexible shipping contracts or prioritize immediate shipments to mitigate the risk of a closed or restricted corridor.

Prioritize Poland for Cost-Competitive European Sourcing Amid Logistical Risks in the Black Sea

European wheat buyers should continue to prioritize Poland as their primary origin to optimize procurement costs while avoiding the heightened logistical risks associated with the Black Sea and Middle Eastern conflicts. As of W10 2026, Poland’s wholesale price of USD 211.4/mt represents the most significant YoY discount among major European producers, down 13.69%. This makes Polish wheat substantially more affordable than French wheat, which carries a premium at USD 225.4/mt. While the Black Sea origins offer competitive pricing, they are currently subject to extreme geopolitical volatility that does not affect Poland’s stable inland and Baltic logistical networks. Although the Polish market saw a 1.45% week-on-week (WoW) decline in USD terms, this was primarily due to a stronger US Dollar (USD) rather than a lack of demand. Securing volumes from Poland now allows buyers to capitalize on steep YoY declines and hedge against the projected medium-term upward pressure as global ending stocks continue to tighten.