In W19 in the palm oil landscape, some of the most relevant trends included:

- Indonesia is prioritizing modernization in its palm oil sector amid stagnant productivity, with the 2025 Hai Sawit Symposium focusing on mechanization, digitalization, and innovation. Stakeholders are investing in technology to improve efficiency, transparency, and global competitiveness.

- Malaysia is promoting its integrated palm oil model in emerging markets like Kenya, emphasizing efficient logistics, supportive policies, and long-term planning. It has offered technical and infrastructure support to help Kenya reduce high transport costs that inflate product prices.

- Myanmar's palm oil reference price declined slightly in W19, though actual market prices remain higher due to import reliance and domestic shortfalls. Authorities are targeting price manipulation and reinforcing legal measures to ensure fair pricing and stable supply.

- Indonesia saw palm oil prices rise 3.45% WoW in W19 due to strong global demand, but geopolitical tensions between India and Pakistan pose risks to future exports.

1. Weekly News

Indonesia

Indonesia’s Seeks to Revive Palm Oil Sector Through Technology

Despite its strategic importance, Indonesia's palm oil industry, a key driver of national economic growth, is facing stagnant productivity. To address this, Hai Sawit, a media company focused on news and insights for the palm oil industry, organized the 2025 Hai Sawit Symposium (HASI) in Jakarta. The symposium focused on mechanization, digitalization, and technological innovation. The event brought together professionals from Indonesia and Malaysia to exchange expertise to improve efficiency, sustainability, and global competitiveness.

Hai Sawit's chief executive officer (CEO) emphasized that technological advancement is essential for overcoming production stagnation and addressing global market and environmental challenges. The Plantation Fund Management Agency (BPDP) also reaffirmed its support through funding for research, mechanization, and digital systems to enhance transparency and productivity across the sector.

Kenya

Kenya Looks to Malaysia’s Palm Oil Model to Tackle Logistics and Boost Sector Efficiency

Kenyan industry stakeholders are seeking to enhance their palm oil sector by learning from Malaysia's integrated model, following a high-level roundtable in Nairobi with Malaysia's Plantation and Commodities Minister. The dialogue highlighted Malaysia's success in combining efficient logistics, supportive policies, and long-term planning to strengthen its palm oil industry. In contrast, high transport costs in East Africa are inflating the prices of palm-based products by up to 40%. Malaysia has offered collaboration on infrastructure and technical support to help Kenya improve supply chain efficiency. This initiative aligns with Malaysia’s broader strategy to foster trade and innovation with emerging markets.

Myanmar

Myanmar's Palm Oil Wholesale Price Slightly Drops, Authorities Tackle Overcharging and Market Manipulation

Myanmar’s wholesale reference price for palm oil fell slightly to USD 3.19 per 1.63 kilograms (MMK 6,700/1.63 kg) in W19, down from USD 3.20/1.63 kg (MMK 6,735/1.63 kg) the previous week, as set by the Supervisory Committee on Edible Oil Import and Distribution (SCEOID). This rate is calculated based on Malaysia and Indonesia's free-on-board (FOB) prices, plus transport, tariffs, and banking costs. Despite this official benchmark, market prices remain significantly higher. In response, the Ministry of Commerce (MoC) has urged consumers to report overcharging and warned that those engaging in price manipulation or hoarding will face legal action under the Essential Goods and Services Law. With domestic demand at 1 million metric tons (mmt) annually and local production at only 400,000 mt, Myanmar relies heavily on palm oil imports, primarily from Malaysia and Indonesia, to bridge the gap. Authorities are working with industry stakeholders to ensure fair pricing and stable supply.

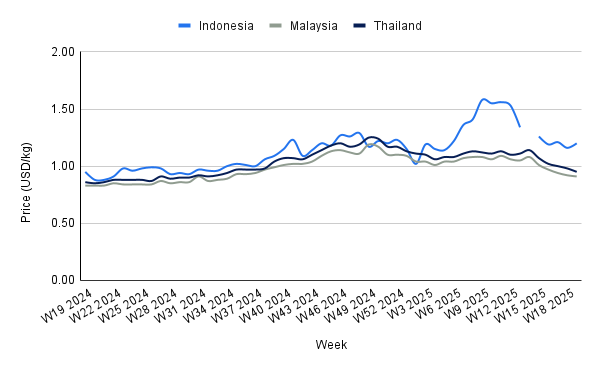

2. Weekly Pricing

Weekly Palm Oil Pricing Important Exporters (USD/kg)

Yearly Change in Palm Oil Pricing Important Exporters (W19 2024 to W19 2025)

Indonesia

In W19, Indonesia's palm oil prices rose to USD 1.20/kg, up 3.45% week-on-week (WoW) and 26.32% year-on-year (YoY), reflecting continued market strength amid robust international demand. However, geopolitical tensions between India and Pakistan, two of Indonesia’s largest palm oil importers, pose a potential risk to future price stability. Although current trade flows remain unaffected, prolonged conflict could weaken demand, particularly from India, which annually imports 5 mmt of Indonesian crude palm oil (CPO), and Pakistan, which imports 3 mmt. An extended disruption could lead to rising domestic inventories, placing downward price pressure. This would not only affect CPO but may also spill over into the broader vegetable oil market, including soybean and sunflower oil.

Malaysia

Malaysian palm oil prices declined to USD 0.91/kg in W19, representing a 1.09% WoW decrease, though 9.64% higher YoY from USD 0.83/kg. This marks the fifth consecutive week of decline, driven by several interrelated factors. The strengthening of the ringgit (MYR), which appreciated 1.48% against the United States dollar (USD), has reduced export competitiveness by making Malaysian palm oil more expensive for international buyers. Concurrently, weaker prices in rival markets, particularly soybean oil and global crude oil, have diminished palm oil's appeal, especially as a biodiesel feedstock. Market sentiment is also weighed down by expectations of rising inventories and seasonal production gains, as the industry enters its peak output period. The outlook remains bearish in the short term, with continued currency strength, subdued energy markets, and increased supply likely to keep prices under pressure unless offset by stronger global demand or supportive policy measures.

Thailand

Thailand’s palm oil prices declined to USD 0.95/kg in W19, despite a 3.06% WoW decrease and a 10.47% rise YoY. The small price increase does not match weak market sentiment, highlighting deeper problems in Thailand’s palm oil sector. Rising input costs, particularly fertilizers, energy, and labor, are squeezing producer margins, while regional competition from lower-priced exporters like Indonesia and Malaysia limits Thailand's ability to lift prices meaningfully.

The combination of elevated production costs and limited price growth has fueled discontent among smallholders, prompting calls for government intervention to safeguard farm incomes. Without policy support or improved export demand, there is a risk that financially strained producers may scale back output, potentially tightening future supply. However, with regional production expected to rise seasonally and global vegetable oil markets facing soft demand, Thai palm oil prices may face continued downward pressure, especially if domestic consumption and export competitiveness fail to improve.

3. Actionable Recommendations

Advance Mechanization and Digitalization to Boost Yields

Producers and stakeholders in Indonesia’s palm oil sector should accelerate investment in mechanized harvesting tools, precision agriculture, and digital supply chain platforms. With stagnant productivity threatening future competitiveness, such innovations, backed by initiatives like the BPDP support, can increase output, reduce labor dependency, and enhance traceability.

Adopt Malaysia's Integrated Industry Model in Emerging Markets

Kenyan and other East African industry leaders should adapt Malaysia's proven model of integrated palm oil development, focusing on efficient logistics, targeted infrastructure, and policy alignment. Partnerships with Malaysian technical experts can help reduce regional transport costs and improve supply chain efficiency, ultimately enhancing price competitiveness for palm-based products.

Diversify Export Markets and Invest in Inventory Risk Mitigation

With geopolitical tensions threatening demand from major importers like India and Pakistan, Indonesian exporters should expand market outreach to emerging regions such as Africa and the Middle East. Simultaneously, develop strategic storage and inventory management systems to mitigate the risk of oversupply and price volatility in case of prolonged trade disruptions.

Sources: Tridge, Republika, Hellenic Shipping News, Ukr Agroconsult