W45 2025: Cheese

In W45, global cheese markets remained bearish, driven by abundant milk production and steady-to-weak demand across major regions. EU cheddar faced downward pressure as strong milk flows sustained high output, while Oceania experienced falling prices amid peak production and softening demand. In the US, spot prices eased despite modest gains in futures, reflecting ample milk supplies and expectations of year-end demand. Meanwhile, FAO’s global dairy price index fell, with cheese prices declining, partly offset by firm Oceania prices supported by Asian orders. The narrowing price gap between US and EU cheddar, combined with rising EU and New Zealand competitiveness, has softened US exports. To navigate these conditions, producers are advised to hedge futures, manage inventories, moderate production, diversify export markets, and develop value-added products. They should also strategically collaborate with international buyers to mitigate volatility and sustain market share.

1. Weekly Price Overview

Cheddar Markets Under Pressure as Milk Output Rises Across Key Region

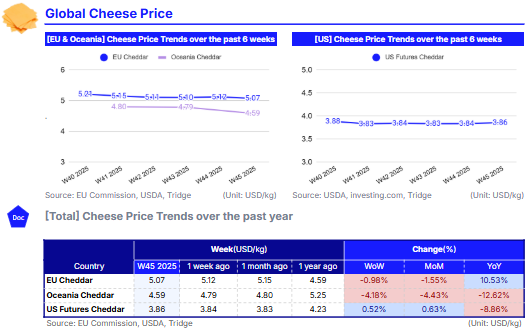

In W45, European Union (EU) cheddar prices averaged USD 5.07 per kilogram (kg), marking a slight 0.98% week-on-week (WoW) and a 1.55% month-on-month (MoM) decline but remaining 10.53% higher year-on-year (YoY). Overall, the EU cheddar market remains bearish, as strong milk production across major dairy regions continues to drive high cheese output, while demand has been steady to weak.

In Oceania, cheddar averaged USD 4.59/kg, down 4.18% WoW, 4.43% MoM, and 12.62% YoY. The drop is attributed to a fading demand as production remains elevated under peak spring flush conditions.

In the US, cheese prices also eased, with barrels averaging USD 1.71, down 0.10% WoW and 40-pound (lb) blocks averaging USD 1.66, down 0.15% WoW. The decline reflects strong production amid steady to light demand, along with ample spot milk availability that continues to weigh on cheese values. In contrast, US cheese futures increased 0.52% WoW and 0.63% MoM, though they remain 8.86% lower YoY at USD 3.86/kg. Futures’ strength may reflect seasonal expectations of improved end-year cheese use, such as holiday baking and food-service needs, as well as possible inventory liquidation by processors ahead of year-end.

2. Price Analysis

Cheese Market Softens as EU Output Remains High and US Export Competitiveness Slips

According to the Food and Agriculture Organization (FAO), the global dairy price index averaged 142.2 points in Oct-25, marking a 3.42% MoM decline driven by lower prices across key dairy commodities. The cheese price index fell to 146.99 points, down 1.51% MoM, reflecting easing prices in the EU where milk supplies remain ample and export demand subdued. This weakness was partly offset by firmer prices in Oceania, supported by strong Asian buying and tighter early-season milk availability. The Global Dairy Trade (GDT) auction on November 4 mirrored this trend, with cheese prices averaging USD 4,449 per metric ton (mt), a 6.6% decrease from the prior event.

The overall global bearish market is largely driven by abundant milk production. In the US, the United States Department of Agriculture (USDA) reported milk output of 18.99 billion lb in Sep-25, a 4% MoM increase supported by both herd expansion and higher yields per cow. As a result, milk supplies remain plentiful, allowing plants to maintain consistent production schedules. Although inventories are manageable, production has begun to slow slightly as processors conclude holiday orders.

Europe follows this trend, with unseasonably strong milk flows sustaining high cheese output while demand ranges from steady to weak. This has continued to pressure prices and has made EU cheese increasingly competitive in global markets, further squeezing US exporters. The price gap between US Chicago Mercantile Exchange (CME) block cheddar and EU spot cheddar has narrowed to its smallest margin since mid-2024. As US price competitiveness erodes, export volumes have weakened, with buyers increasingly shifting toward more attractively priced EU and New Zealand offerings.

3. Strategic Recommendations

Mitigate Margin Pressure and Capture Opportunities in Global Cheese Markets

Given the bearish global cheese market, US producers should consider hedging cheese futures to lock in expected seasonal demand for the year-end period, taking advantage of modest futures strength despite falling spot prices. Inventory management is also critical, with processors encouraged to evaluate slowing production or selectively reducing output to avoid further downward pressure on spot prices while maintaining flexibility for higher holiday demand.

On the export front, US suppliers should diversify markets beyond traditional destinations such as Mexico, targeting regions where European and New Zealand prices are less competitive, and explore value-added or niche cheese products to mitigate margin erosion. Strategic collaboration with international buyers, through forward contracts or long-term supply agreements, can further reduce price volatility and preserve market share.

In the EU, producers should consider moderating production slightly to prevent further price erosion. They should also explore value-added or specialty cheese products to differentiate themselves in international markets. Oceania exporters, facing weakening demand despite solid Asian orders, should prioritize market diversification and negotiate forward sales or long-term contracts in Asia to secure volumes and reduce exposure to short-term price declines.