In W23 in the soybean landscape, some of the most relevant trends included:

- New US tariffs risk long-term disruption to global soybean trade, accelerating China’s shift toward South American suppliers amid record global production forecasts.

- Brazil’s 2024/25 harvest faced weather extremes but achieved strong yields.

- US planting progressed ahead of five year average in early Jun-25, with 67% of crops in good-to-excellent condition.

- US soybean prices rose slightly WoW in W23 due to strong exports and weather delays. Meanwhile, Brazil and Argentina saw steady WoW prices but declining YoY prices due to ample supply and subdued demand.

1. Weekly News

Global

Trade Disruptions Shifted Soybean Market Dynamics

The United States (US) has reignited concerns over tariff-driven trade policies, particularly with China, America’s top soybean buyer. While global soybean markets initially showed resilience, falling only 1% year-on-year (YoY) by the end of Feb-25, renewed tensions could still carry significant long-term consequences. With the United States Department of Agriculture (USDA) forecasting a record 427 million metric tons (mmt) of global soybean production in the 2025/26 season, such trade measures could accelerate existing trends, including China’s deepening trade ties with South American suppliers like Brazil and Argentina. As South America strengthens its dominance in global soybean exports, US tariffs risk disrupting short-term trade flows and cementing a lasting realignment in global soybean trade dynamics.

Argentina

Argentina’s Late Soybean Harvest Nears Completion Despite Adverse Weather

Between May 28 and June 3, 2025, late soybean crops in the north and north-central areas in Argentina reached full maturity. This is despite facing heat stress and drought, though high humidity delayed harvesting, which had progressed to about 75%. In contrast, the central and southern regions completed their harvest with strong results, achieving average yields of 3.5 to 4.8 metric tons (mt) per hectare (ha), 0.5 mt/ha higher than initial estimates, across approximately 365,400 ha.

Brazil

Brazil’s 2024/25 Soybean Harvest Faced Extreme Weather

The 2024/25 Brazilian soybean harvest was marked by extreme and unpredictable weather, significantly affecting crop development and yields. The season began under drought conditions and ended with regional imbalances in rainfall, either excessive or insufficient, impacting all stages of cultivation. Sowing began in Sep-24 after the sanitary gap ended, with initial planting limited to irrigated areas in the Central-West due to irregular weather. Meanwhile, Paraná progressed on schedule thanks to favorable conditions. Oct-24 saw a slow start to planting, which picked up pace later in the month, with Mato Grosso completing sowing for areas designated for the second crop just in time. Nov-24 brought normal rains to the Central-West and Southeast, aiding crop establishment. However, dry spells began affecting the South, and early pest outbreaks were reported in Mato Grosso, adding further stress to the season.

United States

US Soybean Planting Progresses Ahead of Schedule in 2025

As of June 1, 2025, the USDA reported that US soybean planting was progressing slightly ahead of 2024, with 84% of the estimated area planted, 7% higher than the same period in 2024 and 4% above the five-year average. In Minnesota, planting had nearly concluded, reaching 97% of the intended area. Moreover, 63% of soybean crops had emerged nationwide, with 67% rated in good to excellent condition, reflecting generally favorable early crop development.

2. Weekly Pricing

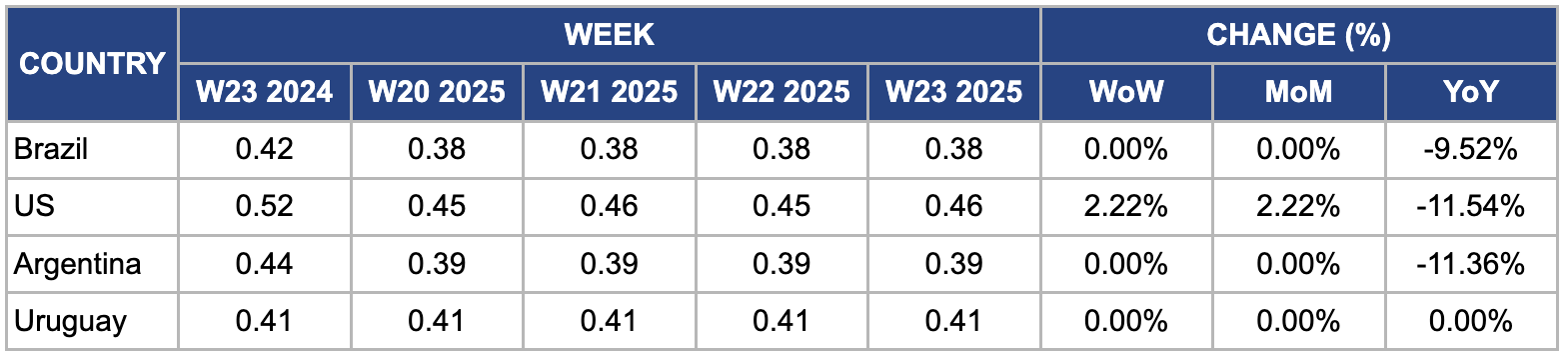

Weekly Soybean Pricing Important Exporters (USD/kg)

* Varieties: Food grade soybean

Yearly Change in Soybean Pricing Important Exporters (W23 2024 to W23 2025)

* Varieties: Food grade soybean

* Blank spaces on the graph signify data unavailability stemming from factors like missing data, supply unavailability, or seasonality

Brazil

In W23, Brazil’s soybean prices remained unchanged week-on-week (WoW) and month-on-month (MoM) at USD 0.38 per kilogram (kg). However, prices declined 9.52% YoY due to ample supply and reduced international demand. Brazil’s 2024/25 soybean production is expected to remain high, with recent estimates from the National Supply Company (CONAB) projecting output at around 147.7 mmt, maintaining pressure on prices. Despite some logistical issues and currency fluctuations, the Brazilian real's (BRL) relative strength in recent months has also made exports slightly less competitive globally. Moreover, slow demand from major buyers like China amid concerns over their stock levels and economic outlook has limited upward price momentum, keeping domestic prices subdued compared to the previous year.

United States

In W23, US soybean prices slightly increased by 2.22% WoW and MoM to USD 0.46/kg, supported by improved export activity and weather-related concerns. The USDA reported higher-than-expected weekly export sales, particularly to China and Mexico, which boosted market sentiment. Furthermore, planting delays in parts of the Midwest due to scattered rainfall and cooler temperatures raised concerns over potential yield impacts, contributing to the slight price uptick. Despite favorable crop prospects, these short-term uncertainties and improved demand helped lift prices modestly.

Argentina

In W23, Argentina's soybean prices remained steady WoW and MoM at USD 0.39/kg. However, prices recorded an 11.36% YoY decline from USD 0.44/kg in W23 2024, primarily due to a significant rebound in production during the 2024/25 season. Following 2024’s drought-affected harvest, improved weather conditions in 2025, including adequate rainfall and moderate temperatures, have supported higher yields and larger harvested areas. The Rosario Grain Exchange (BCR) recently estimated soybean output at around 51 mmt, a sharp recovery from the previous season’s 20 mmt. This boost in supply has weighed on prices despite stable domestic demand and moderate export activity.

Uruguay

In W23, Uruguay’s soybean prices remained unchanged WoW, MoM, and YoY at USD 0.41/kg, reflecting a market in equilibrium. This stability is supported by Uruguay’s estimated 2024/25 soybean production of around 3.5 mmt, with average yields near 3.2 mt/ha, following favorable weather conditions throughout the growing season. Export volumes remained consistent, with Uruguay shipping approximately 2.8 mmt of soybeans in the first half of the year (H1-25), mainly to China and other Asian markets. Furthermore, no significant fluctuations occurred in currency exchange rates, and the Uruguayan peso remained relatively stable against the US dollar, helping maintain steady input costs and export competitiveness.

3. Actionable Recommendations

Diversify Soybean Sourcing Toward Stable and Competitive Suppliers Like Uruguay

Given the geopolitical uncertainty surrounding US-China trade and the potential reimposition of tariffs, China should diversify its sourcing beyond the US. Uruguay offers a stable, tariff-free alternative with consistent pricing, solid production, and reliable export volumes. With no YoY price fluctuation and a favorable exchange rate environment, Uruguay provides price stability and supply predictability. Building stronger procurement relationships with Uruguayan exporters could mitigate risks from trade tensions and enhance supply chain resilience.

Capitalize on Brazil’s Lower Prices for Short-Term Bulk Purchases

Brazilian soybean prices have fallen YoY due to high production and slow Chinese demand. Although some logistical and currency constraints exist, the high supply and soft global demand offer buyers an opportunity to secure competitively priced volumes in the short term. Importers should consider increasing purchases from Brazil while prices remain under pressure, especially before any weather-induced disruptions or recovery in Chinese buying tightens the market. This approach supports cost-effective procurement while balancing risk from other origins.

Monitor US Market Closely for Signs of Further Tariff Escalation and Yield Impacts

Despite a slight weekly price uptick, the US market remains vulnerable to policy shifts and weather volatility. The potential reimplementation of tariffs on Chinese goods could disrupt export flows. Moreover, Midwest weather concerns may impact yields and create further price instability. Therefore, importers in China, Vietnam, Thailand, South Korea, Japan, and the European Union (EU should closely track political developments and crop progress. Buyers in these countries should remain flexible with contracts and avoid overreliance on US-origin soybeans until there is greater clarity on trade policy and weather outcomes. Strategically using futures contracts or hedging tools can also help manage exposure to potential price spikes and supply disruptions.

Sources: Tridge, Agro Link, Chacra Magazine, Ukr Agro Consult