W26 2025: Sugar Weekly Update

In W26 in the sugar landscape, some of the most relevant trends included:

- Brazil's sugar output fell 21.5% in early Jun-25 due to rains, while ethanol blending mandates and export activity helped stabilize domestic prices.

- US futures softened slightly, but lower production forecasts and trade policy tensions suggest possible price rebounds in the near term.

- Mexico’s sugar exports face headwinds from US tariffs, leading to mixed domestic price movements and potential oversupply.

- Pakistan's sugar prices climbed again due to tight supplies, triggering merchant pushback and emergency import approvals.

1. Weekly News

Brazil

Cane Crush Contracts While Ethanol Mandate Expands

Brazil’s centre‑south cane crush rate plunged 21.5% in early Jun-25 due to heavy rains, with only 38.78 million metric tons (mmt) processed, a significant contraction compared to last year, signaling a lighter feedstock supply this cycle. Concurrently, ethanol sales in the region dropped nearly 14% in the first half of Jun-25, underlining a broader slowdown in biofuel off‑take.

The federal government approved a higher ethanol blend mandate, increasing corn-ethanol output. This surge in production, reaching 3 billion liters, allowed Brazil to balance rising fuel demand without raising pump prices.

India

Co-op Consolidates Power and Tightens Export Rules Amid Positive Crop Prospects

The NCP faction secured a commanding victory in Maharashtra’s Malegaon sugar‑mill elections, winning 20 of 21 seats. This reinforces the cooperative’s dominance and directs future mill policies. These outcomes may shape pricing and procurement strategies during the upcoming season.

Meanwhile, market sentiment remains bullish despite earnings pressure: India’s biggest sugar‑producer federation forecasts a 19–25% production surge to over 35 mmt in 2025/26, yet sugar stocks dipped this week following weak market sentiment. Early monsoon patterns are expected to underpin crop volumes, though uneven regional rains will require close monitoring.

Mexico

US Tariffs Curtail Exports as Supply Recovers

Mexico’s 2025/26 crop is expected to reach 5.094 mmt, bouncing back 7% from last year. However, US tariff barriers under suspension agreements are likely to tamp down shipments of specialty and raw sugar, potentially straining local processors by increasing domestic inventories. The USDA’s outlook keeps Mexican exports steady at approximately 572,489 STRV to the US, but incoming US quota announcements could tighten balances further.

Pakistan

Prices Rise Amid Supply Measures and Merchant Pushback

Pakistan reported a further 0.88% weekly rise in domestic sugar prices, with wholesale rates climbing to USD 0.61-0.62 per kilogram (PKR 174–177/kg) and retail reaching USD 0.67/kg (PKR 190/kg), provoking merchants to threaten a sales halt unless prices stabilize. In response, the Sugar Advisory Board approved the import of 500,000 metric tons (mt) of sugar to replenish supply.

Earlier last week, the Food Security Minister reaffirmed a commitment to block “unjustified increases” in sugar pricing, though public trust remains low after prior assurances failed to curb volatility.

United States

Futures Activity Picks Up, Production Outlook Tapers

Intercontinental Exchange (ICE) sugar futures saw enhanced trading this week: prices held firm at 126,301 contracts with open interest dropping to 832,608 by June 30, indicating tightening positions. The United States Department of Agriculture (USDA) cut its 2025/26 sugar production forecast by 17,000 stocks-to-use ratio (STRV) amid a tighter supply outlook. Moreover, consolidating trends continue; United States (US) sugar production rose 16% since 1997 despite halved farm counts, highlighting improved efficiency in beet and cane sectors.

2. Weekly Pricing

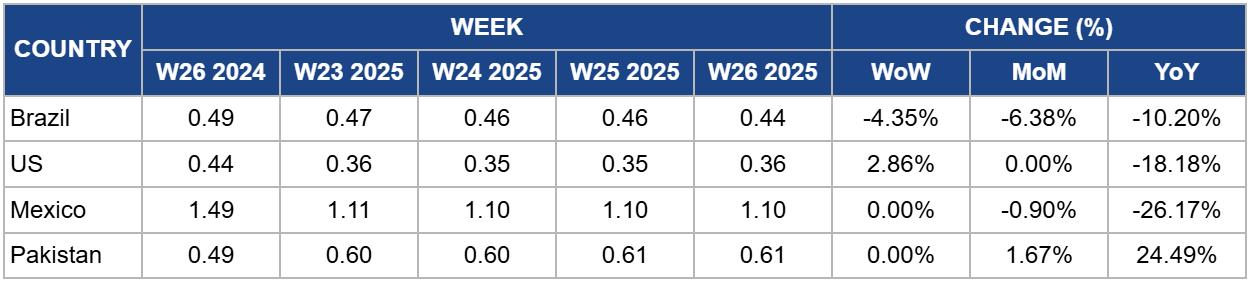

Weekly Sugar Pricing Important Producers (USD/kg)

Yearly Change in Sugar Pricing: Important Producers (W26 2024 to W26 2025)

.png)

Brazil

In W26, Brazil’s sugar prices remained relatively bearish despite adverse weather conditions at USD 0.44/kg, down 4.35% week-on-week (WoW) and 10.20% year-on-year (YoY). The spot market saw little volatility as center-south crushing activity was disrupted by persistent rains, which pushed the first-half Jun-25 crush volume down by over 21% YoY. Export volumes remained strong, but domestic pricing was cushioned by steady demand and strong ethanol market signals.

For the coming week, prices are expected to remain under pressure. While recent rainfall may lead to short-term logistical delays and localized tightening, overall production estimates remain solid. Continued strength in the Brazilian real (BRL) against the US dollar may also help provide a modest floor to prices, but without a major catalyst, upside is likely to be limited.

United States

Wholesale sugar prices rose slightly in W26 to USD 0.36/kg, a 2.86% WoW rise. However, prices remain relatively lower than the previous year, down 18.18% YoY. This bearish trend occurs alongside a fall in open interest (to 832,608 contracts by June 30) and a decline in volume, suggesting weakening bullish sentiment. Moreover, the USDA reduced its 2025/26 production forecast slightly, citing lower beet yields, however, this did not have a significant near-term impact on spot prices.

Looking ahead, US sugar prices may edge slightly higher in W27. The imposition of new tariffs on Brazilian sugar and a tapering production outlook suggest a tighter market balance heading into late Jul-25. Traders should watch for USDA quota updates and any revisions to Brazilian export data, which could trigger short-term speculative interest.

Mexico

In W26, domestic wholesale prices remained relatively flat at USD 1.10/kg. The Mexican sugar sector continues to grapple with the impact of US tariffs, which are expected to limit export volumes under suspension agreements, potentially creating domestic oversupply.

For the coming week, prices are likely to trend downward. While harvest prospects for 2025/26 have improved, forecast at 5.094 mmt, the inability to redirect surplus volumes into the US could weigh on processor margins and inflate inventories. Local market participants should brace for price resistance unless alternative export channels materialize.

Pakistan

Sugar prices in Pakistan remained flat WoW at USD 0.61/kg in W26. Despite this, prices remain on an upward trajectory, rising by 1.67% month-on-month (MoM) and 24.49% YoY. This rise is being fueled by reduced domestic availability, speculative hoarding, and delayed import arrivals, prompting widespread merchant discontent and even threats of a trading halt if price controls are not enforced.

Looking ahead, prices in Pakistan are likely to rise further in W27. With government imports of 500,000 tons still pending clearance and no structural improvement in supply chain flows, upward pressure remains strong. Market expectations suggest sugar could continue rising, particularly in high-demand regions, unless regulatory enforcement intensifies or imports are expedited.

3. Actionable Recommendations

Strengthen Hedging Strategies Amid Global Price Volatility

With ICE sugar futures slipping below US¢ 0.16 per pound (lb) and signs of global surplus weighing on sentiment, traders and producers, especially in Brazil, India, and the US, should reinforce hedging programs to lock in prices. Employing forward contracts and options can help mitigate downside risk amid fluctuating weather patterns, shifting production forecasts, and ongoing macroeconomic pressures.

Secure Alternative Export Channels in Protectionist Markets

Exporters in Mexico and Brazil should actively pursue diversification of export destinations beyond the US, where tariff regimes and quota uncertainty are suppressing volumes. Building commercial relationships in markets across North Africa, Southeast Asia, and the Middle East will help de-risk revenue streams and avoid inventory build-ups caused by constrained trade flows.

Increase Inventory Monitoring and Import Coordination in Tight Markets

Stakeholders in Pakistan should coordinate closely with government import schedules and warehouse managers to stabilize retail pricing. With domestic supply tight and prices rising, processors and large distributors may benefit from pre-emptive stockpiling or temporary import partnerships to alleviate local pressure and avoid disruptive trade boycotts or regulatory penalties.

Sources: Tridge, AP News, The Guardian, Nasdaq, Reuters, Times of India, Barchart, Sugar Online