1. Weekly News

Argentina

Rainfall Improves Corn Planting in Argentina

Recent rainfall in Argentina benefited the eastern and southeastern regions, while much of the country has remained dry and warm. The forecast indicates improved chances of rains in W42, along with cooler temperatures, particularly in Central and Northern Argentina. As of late W41, farmers had planted 13.7% of their 2024/25 corn, marking a weekly advance of 3.2%. In Central Entre Rios, 65% of the corn acreage has been planted, while core production areas are 40 to 50% planted. The overall corn acreage for 2024/25 is estimated at 6.0 million hectares (ha), down by 1 million ha. The final acreage may be influenced by Oct-24's rainfall, with a dry month potentially reducing acreage, whereas a wetter month could allow for more planting. Current estimates project the corn production at 48 million metric tons (mmt), although this will depend on weather conditions and pest infestations.

Brazil

Brazil's Oct-24 Corn Exports Estimated at 6.22 MMT

According to the National Association of Cereal Exporters (ANEC), Brazil's corn exports in Oct-24 are estimated at 6.22 mmt, an increase from 5.68 mmt forecasted last week. This upward revision is due to strong export demand for Brazil's agricultural commodities.

Mato Grosso Safrinha Corn Production Declines in 2023/24

According to the Mato Grosso Institute of Agricultural Economics (IMEA), Mato Grosso's safrinha corn production in the 2023/24 season totaled 47.17 mmt. This marks a 10.1% year-on-year (YoY) decline from the previous year but remains the second-largest safrinha corn harvest in the state's history. Farmers planted 6.8 million ha, down 9.2% YoY, due to low corn prices, high production costs, and delays in planting caused by a late soybean harvest. The average yield for 2023/24 was 115.5 sacks/ha. For the 2024/25 safrinha season, IMEA projects a slight reduction in the planting area, with 6.79 million ha, down 0.14% YoY. The decrease is again due to low corn prices and delays in soybean planting due to hot, dry conditions. The expected yield is 111.7 sacks/ha, leading to an estimated production of 45.54 mmt, a 3.4% YoY decline compared to 2023/24. Mato Grosso remains Brazil's top Safrinha corn producer, accounting for about 75% of the country’s total corn output.

France

France's Corn Harvest Faces Major Delays Due to Heavy Rains

France's corn harvest in 2024 is progressing at its slowest pace in 11 years due to heavy rains, particularly in the northern regions. As of October 7, only 6% of the planned corn area had been harvested, compared to 50% at the same time last year, marking the lowest rate since 2013. The largest corn producer in Europe, France typically produces around 15 mmt annually, exporting about 40% of this output. The delays could impact both domestic supply and export schedules.

United States

USDA Raises 2024/25 Corn Production Estimates

The United States Department of Agriculture's (USDA) Oct-24 report raised the United States (US) corn production estimate for the 2024/25 season, now forecasting 15.2 billion bushels, up 17 million bushels from Sep-24's forecast, due to a slight yield increase to 183.8 bushels per acre. Despite unchanged harvested acreage at 82.7 million acres, tighter supplies and higher consumption are expected to drive ending stocks down by 58 million bushels to 2 billion.

2. Weekly Pricing

Weekly Maize Pricing Important Exporters (USD/kg)

* Varieties: US (feed grade), all others (overall average)

Yearly Change in Maize Pricing Important Exporters (W42 2023 to W42 2024)

* Varieties: US (feed grade), all others (overall average)

* Blank spaces on the graph signify data unavailability stemming from factors like missing data, supply unavailability, or seasonality

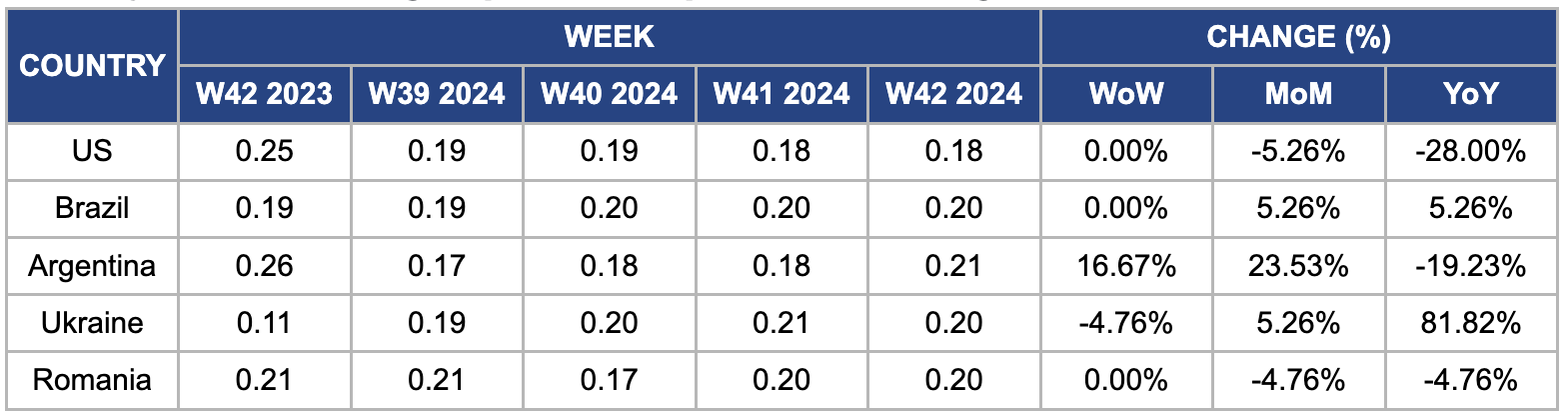

US

In W42, wholesale maize prices in the US held steady week-on-week (WoW) but dropped 5.26% month-on-month (MoM) and 28% YoY, settling at USD 0.18 per kilogram (kg). This decline is largely attributed to the USDA's upward revision of corn production and yield estimates, with output now forecasted at 15.186 billion bushels and an average yield of 183.6 bushels per acre. The improved production outlook has eased supply pressures, significantly contributing to the YoY price decline.

Brazil

In W42, wholesale maize prices in Brazil remained steady WoW but increased by 5.26% MoM and YoY, reaching USD 0.20/kg. Brazil's first corn crop planting is 37% completed in the south-central and southern regions, supported by recent rainfall. The total acreage for this first crop is estimated at 9.26 million acres, 6% YoY lower, resulting in a production estimate of 23 mmt, down 2%. Safrinha corn acreage is expected to cover 39.19 million acres, a 2% decrease, with production projected at 100 mmt, representing a 10% increase. Brazil's corn production for the 2024/25 season is estimated at 125 mmt, marking a 2.5 mmt increase from 2023.

Argentina

The wholesale price of Argentine corn surged by 16.67% WoW and 23.53% MoM, reaching USD 0.18/kg. According to the Buenos Aires Grains Exchange (BAGE), this price spike is primarily due to delays in the 2024/25 corn planting caused by ongoing dry conditions. Concerns are growing over a potential leafhopper plague, similar to the one that severely affected the previous corn harvest, which could result in approximately 2 million ha left unplanted. A significant portion of the unplanted area may shift to soybeans. These challenges have also led to delays in input sales and lowered planting expectations, with an anticipated production shortfall of around 21% YoY and the total corn planting forecast reduced to about 8 million ha.

Ukraine

Ukrainian wholesale maize prices fell 4.76% WoW, reaching USD 0.20/kg. This price decline is due to reduced demand in local and international markets. The rapid pace of the US corn harvest and favorable rains in Brazil have reduced the demand for Ukrainian corn, putting downward pressure on prices. However, Ukrainian maize prices increased by 5.26% MoM and 81.82% YoY. According to the Ukrainian Agrarian Council (UAC), this YoY price surge is mainly due to the USDA revising its corn harvest forecast for Ukraine down by 1 mmt to 26.2 mmt, slightly higher than the Ministry of Agriculture's forecast of 25 mmt.

Romania

In W42, Romanian maize wholesale prices stood at USD 0.20/kg, marking a decrease of 4.76% MoM and YoY. Despite this decline, Romania, Europe’s second-largest grain exporter, is contending with a notable reduction in corn harvests due to one of the most severe droughts in decades. Nearly 2 million hectares of farmland are impacted, with corn output projected to decrease by 10 to 15% for the Oct-24 to Sep-25 season. This anticipated reduction is raising concerns about tighter supply and potential market disruptions in the coming months.

3. Actionable Recommendations

Improve Pest Monitoring and Management

To combat the looming threat of pest infestations, particularly the potential leafhopper plague that has historically affected corn crops, Argentine farmers should enhance their integrated pest management (IPM) strategies. This involves implementing more rigorous pest scouting programs to monitor fields for early signs of infestations, using biological control methods such as introducing natural predators, and adopting chemical controls judiciously when necessary. Furthermore, leveraging predictive models that consider weather patterns can help farmers anticipate pest outbreaks and respond proactively. Encouraging the cultivation of pest-resistant corn varieties can also provide a buffer against crop losses, ensuring a more stable yield even in challenging conditions.

Diversify Export Markets

Given Brazil's robust corn export volumes, expanding its market reach is a significant opportunity. Brazilian exporters should focus on identifying and developing new trade agreements with emerging markets, particularly in regions like Africa and Southeast Asia, where demand for corn and other agricultural products is rising. Collaborating with trade organizations and farming cooperatives can facilitate these efforts. Moreover, investing in logistical improvements, such as streamlining port operations and enhancing transportation networks, can reduce shipment bottlenecks. This enhances Brazil's competitiveness in the global market and ensures timely delivery of products, ultimately supporting better price stabilization.

Optimize Planting Schedules and Irrigation

With France experiencing significant weather-related delays in corn harvesting due to heavy rains, farmers should adopt more adaptable planting schedules that better align with changing climatic conditions. Utilizing agronomic practices that account for weather variability can improve planting success. Furthermore, investing in advanced irrigation systems, such as drip or precision irrigation, can help mitigate the impact of excessive rainfall or droughts, ensuring a more consistent and reliable yield. These practices can enhance resilience against unpredictable weather patterns, reduce harvest delays, and ultimately maintain France's status as the largest corn producer in Europe.

Sources: NoticiasAgricolas, UkrAgroConsult, Milknews, Superagronom, APK inform