W49 2025: Orange

.jpg)

In W49 2025, global orange prices were largely bearish, with the notable exception of the US. Physical prices in Brazil (-4.27% WoW to USD 215.3/mt) and Mexico fell as supply fundamentals normalized across the Americas. Conversely, US Futures surged 11.98% WoW following government purchase announcements. Long-term trends confirm a massive correction from 2024 crisis levels, with Brazil down 50.95% YoY and US Futures down 67.63% YoY. Spain remains the outlier, with farmgate prices up 7.84% YoY and 10.47% MoM due to a severe 16-year production low forecast by the WCO. This structural deficit in Spain persists despite increased competition and stagnant consumption. Given the supply delays in Mexico and the recovered harvest in Brazil, buyers should prioritize Brazilian origin for cost efficiency and volume stability.

1. Weekly Price Overview

US and European Prices Trend Upward While Latin American Prices Face Downward Pressure

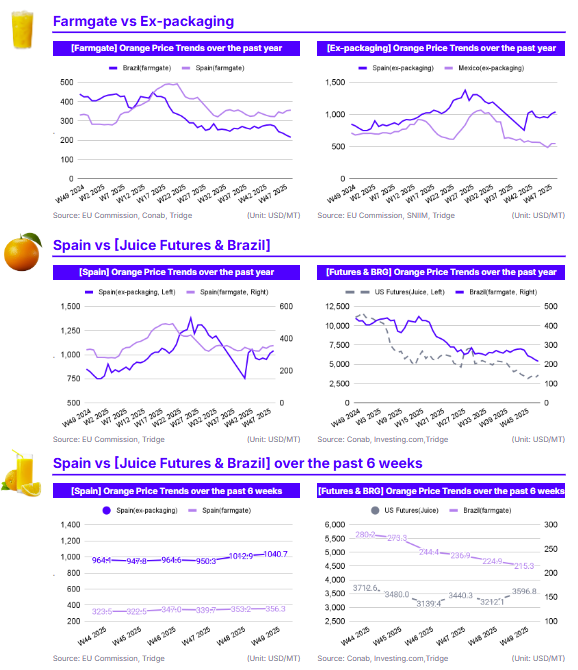

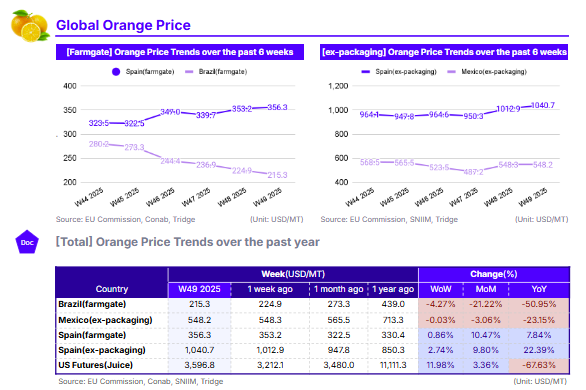

In Brazil, the farmgate price for oranges was USD 215.3/metric ton (mt) in W49, representing a 4.27% decrease week-on-week (WoW). Mexico’s ex-packaging price remained virtually flat at USD 548.2/mt, declining a marginal 0.03% WoW. In Spain, prices trended upward, with the farmgate price rising 0.86% WoW to USD 356.3/mt and the ex-packaging price increasing 2.74% WoW to USD 1,040.7/mt. US Orange Juice Futures posted the most significant gain, surging 11.98% WoW to USD 3,596.8/mt.

The week’s price movements highlight a sharp contrast between the North American and South American markets. The 11.98% WoW surge in US Orange Juice Futures is largely attributed to positive industry sentiment following the USDA’s announcement of a USD 30 million citrus purchase program, which has provided immediate liquidity and support to domestic growers. Conversely, Brazil’s 4.27% WoW price drop occurred despite a downwardly revised crop forecast. This downward price movement is likely a result of the sector's relief following orange juice's exclusion from US tariff hikes, which has normalized market liquidity and adjusted pricing down from previous speculative highs. In Spain, prices edged higher WoW as the market continues to grapple with a significant production downturn in the Northern Hemisphere, which is currently outweighing the bearish impact of stagnant domestic consumption and competition from extended import seasons.

2. Price Analysis

Northern Hemisphere Shortfalls Support Spanish Strength While Americas Stabilize Post-2024 Crisis

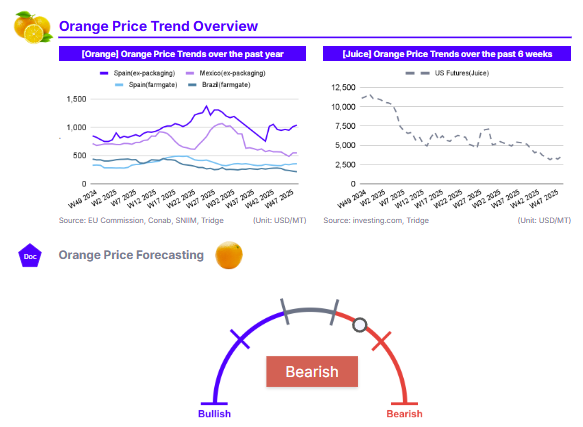

US Orange Juice Futures prices rose 3.36% month-on-month (MoM) to USD 3,596.8/mt, though they remain down a staggering 67.63% year-on-year (YoY). Brazil’s farmgate price fell 21.22% MoM and 50.95% YoY to settle at USD 215.3/mt. Mexico’s ex-packaging price followed a similar long-term trend, dropping 3.06% MoM and 23.15% YoY. Spain remains the outlier, with farmgate prices climbing 10.47% MoM and 7.84% YoY, while ex-packaging prices surged 9.80% MoM and 22.39% YoY.

The massive YoY collapse in Brazil (-50.95%) and US Futures (-67.63%) continues to reflect the broad supply recovery in 2025 compared to the record-low 2024 harvest, which was the worst in nearly four decades. However, the recent MoM recovery in the US (+3.36%) and the rising prices in Spain point to emerging supply constraints in the Northern Hemisphere. The World Citrus Organisation (WCO) projects a significant production decrease for Northern Hemisphere producers in the 2024/25 season, which is the primary driver behind Spain’s 10.47% MoM price jump.

This structural deficit in Europe is currently so severe that increased competition from foreign imports and reduced domestic consumption have been unable to counteract the upward price pressure. In Brazil, the 21.22% MoM decline defies the recent crop revision and localized weather concerns (winds and hail), primarily because the market is re-adjusting following the removal of trade uncertainty and the restoration of normal trade flows with the US.

3. Strategic Recommendations

Prioritize Brazilian Sourcing to Leverage Normalized Supply and Tariff Relief

Global buyers, particularly juice processors in the US, should prioritize sourcing from Brazil to capitalize on its significant cost advantage and the re-stabilization of its export channels. In W49, the Brazilian farmgate price of USD 215.3/mt represents the most competitive price point among major origins, following a massive 50.95% year-on-year (YoY) correction from the 2024 supply crisis. While the 2025/26 harvest was recently revised downward to 295 million boxes, this volume still signifies a robust recovery compared to the multi-decade lows of the previous season.

The exclusion of orange juice from recent US tariff hikes has restored liquidity and normalized trade flows, making Brazilian origin even more attractive for the US market. Importers should act quickly to secure long-term contracts as historically, Brazilian prices tend to trend upward toward the end of the calendar year as the production season winds down. Sourcing from Brazil also hedges against the structural supply deficit in Spain, where production is hitting a 16-year low, and mitigates risks from rising competition in the Mediterranean region.