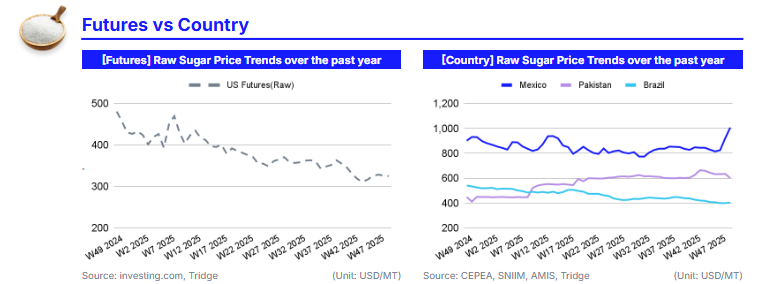

In W49 2025, global sugar markets showed mixed but contained movements across key origins. Brazilian sugar prices increased 1.13% WoW to USD 403.6/mt, supported by late-harvest dynamics, but remain in a deep decline (-25.38% YoY) amid ample Center-South supply and high cumulative output. Mexican sugar prices surged 9.50% WoW to USD 1,007.4/mt, reflecting policy-driven tightening rather than production constraints, while prices are also elevated on a YoY basis. By contrast, Pakistan’s sugar prices declined 5.11% WoW to USD 601.7/mt as delayed crushing weakened spot demand despite still-tight farmer margins. In the derivatives market, US raw sugar futures eased 0.41% WoW to USD 325/mt, remaining significantly lower on a YoY basis in line with USDA projections for higher global production and rising ending stocks in 2025/26.

For global food manufacturers sourcing Brazilian sugar, current conditions favour maintaining near-term coverage from Brazil, where prices remain the lowest among major origins despite brief late-harvest support. Elevated prices in Mexico reflect temporary policy-driven tightening and may normalise as trade flows adjust, while softer prices in Pakistan reflect demand disruption rather than structural oversupply. Overall, with global balances still comfortable, sugar prices are expected to remain range-bound with limited upside into early 2026.

1. Weekly Price Overview

Global Sugar Prices Diverge as Brazil Stabilises Late-Harvest, Mexico Surges on Export Strategy, and Surplus Outlook Caps Futures

In W49 2025, global sugar markets showed mixed price movements over the past two weeks, reflecting contrasting regional fundamentals amid a broadly well-supplied outlook for the 2025/26 season. Brazil’s sugar prices increased by 1.13% week-on-week (WoW) to USD 403.6/mt, supported by late-harvest dynamics in the Center-South region, including an accelerated pace of mill shutdowns and improving short-term cane quality, with Total Recoverable Sugars (TRS) in early November rising 6.23% year-on-year (YoY). However, prices remain sharply lower by 25.38% YoY, as cumulative milling volumes remain near last year’s levels despite a slight 1.26% decline YoY, and as mills continue to divert less cane to sugar for the sixth consecutive fortnight due to weaker relative sweetener margins and end-of-season quality deterioration. Sugar output reached 39.18 million metric tons (mmt) by mid-Nov-25, reinforcing expectations of an ample Brazilian supply despite localized tightening late in the crush.

In Mexico, sugar prices surged by 9.50% WoW to USD 1,007.4/mt, driven by export-related logistics and policy coordination rather than immediate supply shortages. Autumn sugar is expected to account for around 22% of total production this season, supported by reserves carried over from the previous cycle, which will enable Mexico to meet international export commitments, particularly to the United States (US), without disrupting domestic availability. Ongoing discussions with the Federal Government to prioritize domestically produced sugar for programs such as IMEX have further tightened near-term market sentiment, lending strong support to prices.

By contrast, Pakistan’s sugar prices declined by 5.11% WoW to USD 601.7/mt amid delayed crushing in Sindh, which has disrupted cane off-take, weakened spot demand, and raised concerns over farmer incomes and downstream wheat sowing. US raw sugar futures eased by 0.41% WoW to USD 325/mt, remaining under pressure from global surplus expectations outlined by the United States Department of Agriculture (USDA), which forecasts a 4.7% YoY increase in global production and a 7.5% rise in ending stocks for 2025/26. While news of a potential 10% cut in European Union (EU) sugar acreage for 2026/27 offered limited bullish support, strong output prospects in Brazil, India, and Thailand continue to cap upside in international prices.

2. Price Analysis

Sugar Prices Lose Momentum as Brazil Supply Caps Gains and Policy-Driven Spikes Mask a Persisting Global Surplus

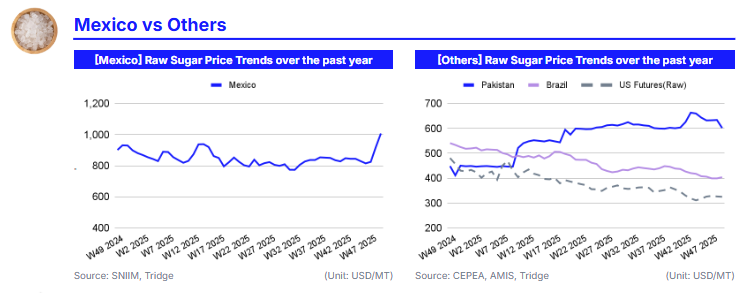

As of W49 2025, sugar prices have softened after a brief recovery, reflecting a market that has largely absorbed recent supply-side revisions and is reverting to surplus-driven fundamentals. In Brazil, prices declined by 1.02% MoM to USD 407.8/mt, as the bullish impact of downward revisions to Center-South production estimates faded. The reduction in projected 2026/27 output, from 42.1 mmt to 41.5 mmt, temporarily lifted prices in Nov-25 by shifting expectations toward tighter future availability. However, this support proved insufficient to sustain momentum, as current physical supply remains ample and accumulated Nov-25 prices still fell 4.53%, indicating that the market views the adjustment as marginal rather than structural. Stable London white sugar contracts at around USD 430 to 436/mt further suggest that global pricing is consolidating rather than entering a new uptrend.

In Mexico, sugar prices rose sharply by 21.46% MoM and 11.74% YoY to USD 901.6/mt, driven primarily by policy-induced tightening rather than production fundamentals. Earlier price weakness caused by imports exceeding 1 mmt triggered strong reactions from producer groups, culminating in a 156% increase in import tariffs. This materially reduced competitive import pressure and restored domestic pricing power, amplifying the price rebound. While initiatives to improve productivity through technology adoption may support medium-term supply growth, the current price surge is largely defensive and policy-driven, making it vulnerable to normalization once trade flows adjust.

Pakistan’s sugar prices fell 6.53% MoM to USD 448.8/mt despite remaining elevated on a YoY basis, reflecting short-term demand disruption rather than surplus production. Delays in the crushing season have constrained market activity, weakened spot demand, and introduced uncertainty for growers, weighing on prices in the near term. However, prolonged delays risk future supply tightening if farmers reduce cane sowing, which could reintroduce upside risk later in 2026. In the US, raw sugar futures rose 2.50% MoM but remain deeply lower YoY, underscoring that recent gains are corrective rather than trend-changing within a globally oversupplied market.

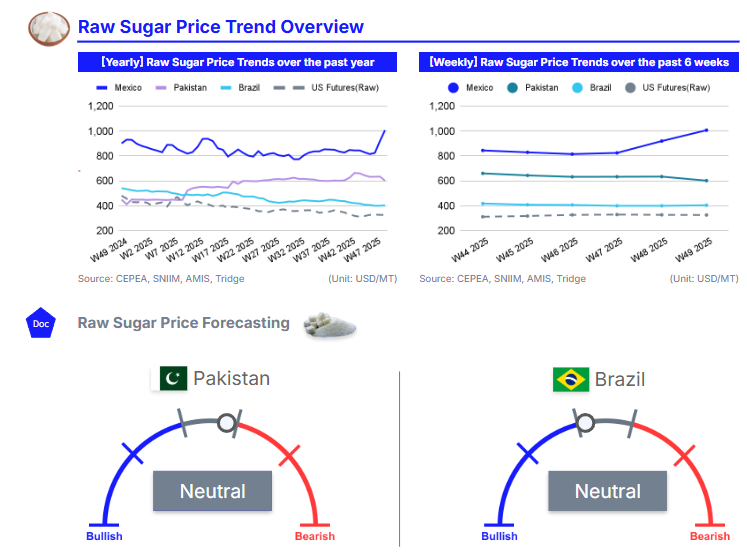

Global sugar prices are likely to remain range-bound with a bearish-to-neutral bias over the next two to three months. Brazil’s modest downward revision to future output may continue to offer episodic support, but without clearer evidence of a broader production shortfall, current supply levels and large global inventories should cap upside. Mexico’s prices are expected to stabilize at elevated levels in the near term but could ease if imports gradually resume under adjusted trade dynamics. Pakistan faces higher volatility tied to policy enforcement and planting decisions. Overall, unless adverse weather materially alters production expectations in Brazil or Asia, sugar prices are more likely to consolidate or drift lower than to sustain a durable recovery into early 2026.

3. Strategic Recommendations

Maintain Defensive Positioning and Exploit Regional Price Dislocations in a Surplus-Driven Sugar Market

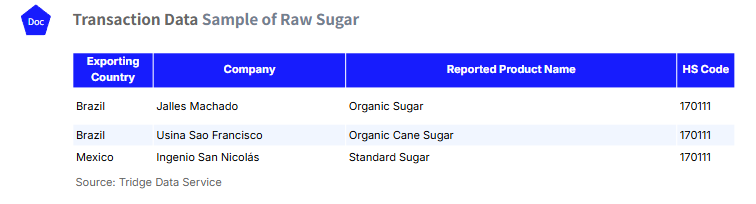

Given the broadly well-supplied global balance and the bearish-to-neutral price bias expected over the next two to three months, buyers should prioritize short- to medium-term coverage rather than aggressive forward locking. International importers are advised to stagger purchases and favor spot or short-dated contracts, particularly from Brazil, where prices remain competitive despite brief late-harvest support. According to Tridge’s Eye transaction data, the continued availability of Brazilian exports, including organic sugar from suppliers such as Jalles Manchado and Usina São Francisco, suggests that physical supply risks are limited and that price rallies are likely to fade. Buyers should use any technical rebounds in futures or free-on-board (FOB) offers to extend coverage incrementally rather than committing to large forward volumes.

For exporters and traders, Mexico’s elevated domestic prices present selective arbitrage opportunities, but exposure should be managed cautiously. The current price strength is largely policy-driven and vulnerable to normalization once import flows adjust or carryover stocks are depleted. Traders with access to Mexican supply, including standard sugar from mills such as Ingenio San Nicolás, according to Tridge’s Eye transaction data, should consider accelerating sales into the current high-price window while avoiding long inventory positions. Hedging downside risk through short futures or options is advisable to protect margins against a potential correction in early 2026.

In Pakistan, near-term price weakness linked to delayed crushing favors a wait-and-see approach for buyers, but exporters and regional traders should monitor planting decisions closely. Prolonged delays could tighten supply later in 2026, creating deferred upside risk. Overall, a conservative trading stance is recommended: remain lightly long physical coverage in low-cost origins such as Brazil, monetize policy-driven price spikes in Mexico, and maintain optionality through flexible contracts and hedging structures. Absent a major weather shock or abrupt policy shift, this strategy balances cost control with protection against episodic volatility in an otherwise range-bound sugar market.