1. Weekly News

Global

USDA Lowers Milk Production Forecasts for 2024 and 2025

In its Oct-24 World Agricultural Supply and Demand Estimates (WASDE) report, the United States Department of Agriculture (USDA) reduced its milk production forecast for 2024 to 225.8 billion pounds (lbs), down by 100 million lbs from the previous estimate. The production forecast for 2025 was also slightly reduced to 227.7 billion lbs. Dairy imports, particularly cheese and butter, are expected to rise by 2024 and 2025. Skim-solid imports will remain steady in 2024 but are projected to increase in 2025.

Fat-based product exports remain stable for 2024, with a potential rise in butter exports for 2025. Skim-solid exports are up in 2024 due to higher nonfat dry milk (NDM) shipments. However, a competitive market may impact 2025 exports.

Lower butter and cheese prices have reduced price forecasts for 2024 and 2025. In contrast, NDM and whey prices are expected to rise. Due to weaker cheese and butter prices, Class III and Class IV milk price forecasts have been lowered, with the all-milk price projected at USD 22.80 per hundredweight (cwt) for 2024 and USD 22.75/cwt for 2025.

China

China's New Sterilized Milk Standards Shifts to Raw Milk

On October 8, 2023, China's National Food Safety Standards Department proposed amendments to its sterilized milk standards (GB25190), significantly impacting the dairy industry. Key changes include prohibiting reconstituted milk and milk powder in sterilized milk production and mandating the use of raw milk exclusively. Labeling requirements for products containing milk powder have also been removed, signaling a shift away from milk powder-based formulations.

These changes are expected to raise production costs, potentially increasing retail prices. While consumers favor the shift towards natural ingredients, industry experts highlight the potential price implications if raw milk prices rise. The amendments may also reduce the demand for milk powder and help balance the domestic raw milk surplus.

Russia

Russia's Daily Milk Sales Rise by 2.7% in 2024

As of October 7, 2024, Russia's Ministry of Agriculture (Minselkhoz) reported that the daily milk sales by agricultural organizations reached 54.5 thousand metric tons (mt), a 2.7% increase compared to last year. The Republic of Tatarstan, Udmurt Republic, Krasnodar Krai, and the Voronezh and Kirov regions led in sales, each achieving around 2 thousand mt. The national average daily milk yield per cow rose to 21.6 kilograms (kg), up 0.9 kg from the previous year, with Krasnodar Krai, Kursk, Kaluga, and Kaliningrad regions leading in productivity at over 27 kg per cow.

Ukraine

Poland Becomes Leading Importer of Ukrainian Dairy

In Sep-24, Poland became the largest importer of Ukrainian milk and cream, contributing significantly to Ukraine's dairy exports. From Jan-24 to Sep-24, Ukraine exported 92.54 thousand mt of dairy products, a 19% increase from the previous year, with Poland leading in purchases of condensed milk. Total dairy export revenue reached USD 224.74 million, with Poland receiving 25.5% of milk and cream exports. Ukraine's condensed milk exports increased by 13%, generating USD 57.37 million. Ice cream exports also surged, with Poland and Germany among the top importers.

United Kingdom

UK Milk Supplies Rise in Sep-24 Despite Seasonal Decline, Outlook for 2024/25 Remains Cautious

According to the United Kingdom's (UK) Agriculture and Horticulture Development Board (AHDB), milk supplies in the UK increased by 0.8% in Sep-24, reaching 970 million liters (L), with an average daily supply of 32.3 million L. Despite higher Sep-24 production, total output for the Apr-24 to Sep-24 dairy season was down 0.6% year-on-year (YoY), at 6.23 billion L. Abundant rainfall in Sep-24 boosted grass growth, positively affecting milk production. The 2024/25 forecast projects total production at 12.28 billion L, a 0.3% decrease from the previous season. Rising milk and fat prices offer some relief to farmers, though high cull prices, financial constraints, and environmental regulations remain challenges for expanding dairy operations.

2. Weekly Pricing

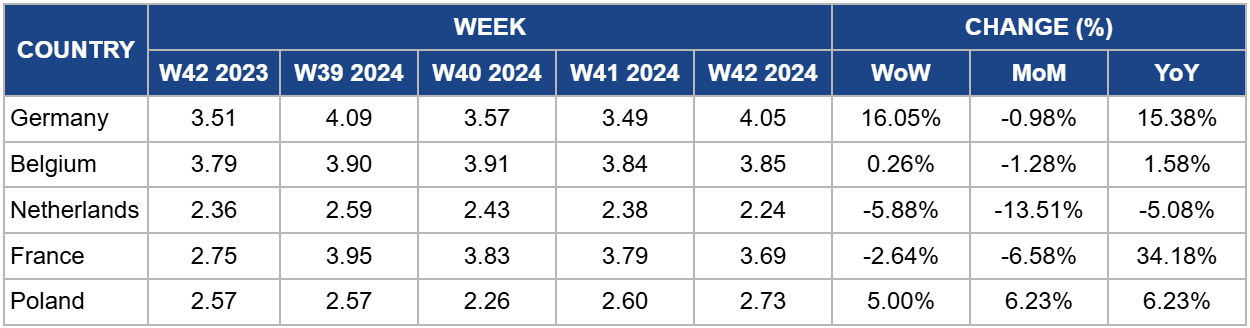

Weekly Powdered Milk Pricing Important Exporters (USD/kg)

Yearly Change in Powdered Milk Pricing Important Exporters (W42 2023 to W42 2024)

.png)

Germany

Germany's whole powdered milk prices rose to USD 4.05/kg in W42, reflecting a 16.05% week-on-week (WoW) increase and a 15.38% YoY rise. Previously, prices were driven higher due to reduced supply caused by heat waves and the outbreak of the bluetongue virus, both of which strained production. Cooler temperatures and easing supply constraints are starting to moderate price pressures. As winter approaches and milk production is forecasted to rise, prices may stabilize further, relieving producers and consumers. However, ongoing market monitoring will be essential to assess whether these trends continue into the colder months.

Belgium

In W42, Belgium's milk prices fell slightly to USD 3.85/kg, a 0.26% WoW decline. Despite this minor price drop, Belgium's dairy sector continues to experience productivity improvements. The average lifetime milk production of dairy cows rose to a record 31,323 kg in the 2023/24 financial year (FY), with 4.23% fat and 3.49% protein content. This increase is due to longer productive lifespans and higher daily milk output. The number of high-yield cows — those producing over 100,000 kg of milk — reached 217, compared to 173 in the previous year. These productivity gains highlight the efficiency improvements in the Belgian dairy sector, which could help stabilize milk prices in the long term despite recent price fluctuations.

Netherlands

In W42, milk prices in the Netherlands fell to USD 2.24/kg, reflecting a 13.51% WoW and 5.08% YoY decrease from USD 2.36/kg. This price drop occurs amid supply constraints tied to disease outbreaks in major dairy regions. The Netherlands, Belgium, and Germany are contending with bluetongue, a viral disease affecting dairy cattle health and fertility, leading to reduced milk production. In severe cases, infected cows show significant drops in output, tightening milk supplies across Europe. Global factors are also contributing to constrained milk supplies, including highly pathogenic avian influenza (HPAI) impacting US dairy operations. Given these challenges, European milk prices are expected to remain high until disease outbreaks are controlled and production stabilizes despite steady demand across markets.

France

France's milk prices decreased to USD 3.69/kg in W42, marking a 2.64% WoW decline and a significant 6.58% month-on-month (MoM) drop. While milk supply in France and across Europe is recovering after earlier disruptions caused by unfavorable weather and the bluetongue virus, prices are still elevated, reflecting ongoing supply challenges. Despite the recent decline, prices remain 34.18% higher YoY, up from USD 2.75/kg, underscoring the lingering effects of production constraints and sustained strong demand compared to the abundant supply conditions in 2023.

Poland

Poland's milk prices rose to USD 2.73/kg, reflecting a 5% WoW increase and a 6.23% rise in both MoM and YoY. This steady price growth aligns with increased demand and Poland's recent position as the largest importer of milk and cream from Ukraine. From Jan-24 to Sep-24, Poland accounted for a significant portion of Ukraine's dairy exports, including 25.5% of Ukrainian condensed milk and cream exports. This import surge has supported domestic supply and price stability amid broader European market fluctuations. Despite higher prices, Poland's strong dairy trade with Ukraine is likely contributing to sustained demand across the market.

3. Actionable Recommendations

Adapt to China's Sterilized Milk Regulations

Dairy exporters targeting China should adjust their strategies to comply with the newly proposed regulations prohibiting reconstituted milk and mandating raw milk in sterilized milk production. Producers should transition to using raw milk in export products, differentiating by marketing natural ingredients to appeal to consumer preferences for high-quality, raw milk-based products.

Capitalize on Rising Milk Prices in Key European Markets

With rising milk prices in countries like the Netherlands and Poland, milk exporters should focus on increasing supply to these regions. Expanding partnerships with European distributors can help meet the growing demand, particularly as local production faces challenges from disease outbreaks.

Sources: Tridge, MilkUA, All Retail, Milk News, Dairy Herd, Hoards