W44 2024: Beef Weekly Update

.jpg)

1. Weekly News

European Union

EU Beef Production and Consumption Expected to Decline Amid Tight Supply and High Prices

The latest European Union (EU) short-term outlook report forecasts a gradual decline in EU beef production due to structural adjustments. As a result, a 0.5% year-on-year (YoY) beef production drop is expected in 2024 and a further 1% YoY decrease in 2025 as herds shrink. Despite limited cattle supplies, EU beef exports remain strong, particularly driven by demand from the Turkish market.

Despite the pessimistic outlook, EU beef production rose by 3% YoY in the first half of 2024, largely due to increased slaughters in Italy (+9% YoY) and Poland (+20% YoY. This situation was spurred by factors such as poor pasture conditions in Central Europe and higher demand from export markets like Turkey. However, this growth is expected to taper off by year-end as some EU countries, including Italy and Spain, face a shortage of young cattle.

Producer prices for beef remain high, supported by limited supplies and strong live animal prices. Stabilizing feed costs and elevated carcass prices improve feeders' margins. With tight supplies keeping consumer prices high, per capita beef consumption in the EU is projected to decrease by 1.7% YoY, reaching 9.6 kilograms (kg) in 2024. It is further expected to drop an additional 1.2% YoY in 2025.

Brazil

Brazil’s Beef Industry Faces Challenges and Opportunities for Sustainable Growth

Brazil, the world’s leading beef exporter, faces new challenges in consumer markets, particularly with the EU’s upcoming anti-deforestation law, the European Union Deforestation Regulation (EUDR). To address this, the Brazilian Sustainable Livestock Board (MBPS) held the “Inclusive Dialogue - Opportunities and Solutions for Producers to Comply with the EUDR,” where industry leaders discussed solutions for meeting these environmental standards and maintaining market access.

Brazil’s livestock sector is known for its sustainable practices, with programs like “Boi na Linha” and the AgroBrasil+Sustentável platform supporting environmental compliance. Despite this progress, participants highlighted challenges in monitoring indirect suppliers and providing technical support to rural producers, which will be crucial to aligning with EUDR requirements.

As global environmental regulations become more common, even in markets like China, Brazil’s efforts in sustainable cattle farming present a competitive advantage. Panelists emphasized the importance of collaboration across the supply chain to maintain Brazil’s position in global markets and ensure that its environmental assets are recognized and valued globally.

Brazil’s Meat Production Expected to Increase by 22.21% Over the Next Decade

According to the Ministry of Agriculture, Livestock and Food Supply (MAPA), Brazil’s meat production is projected to grow by 22.21% over the next decade, increasing from 30.776 million metric tons (mmt) in 2024 to 37.597 mmt by 2034. This growth reflects an annual production increase of 2.4% for chicken and pork, and 1.1% for beef.

Specifically, beef production is expected to rise by 10.2% over the period, from 10.221 mmt in 2024 to 11.26 mmt in 2034. Domestic demand for beef is anticipated to grow by 0.6% over the decade, reaching 6.753 mmt by 2034. Meanwhile, beef exports are expected to see significant 27.9% growth, rising from 9.907 mmt in 2024 to 12.671 mmt in 2034.

This expansion is supported by various trade agreements made by the Brazilian government with key consumer countries. These agreements reinforce established markets and open doors to new countries importing Brazilian meat, solidifying Brazil’s competitive position in the global meat market.

China

China to Enforce Full Traceability for Brazilian Beef Imports by 2025

China, the leading importer of Brazilian beef, plans to enforce full traceability for Brazilian meat by 2025, marking a shift in trade protocols between the two countries. Although traceability has been part of existing agreements, it has not been strictly applied. During a recent technical visit to Brazil, Chinese authorities indicated they would soon require traceability across the entire supply chain, from the animal's birth to its export. This new requirement still needs to mandate deforestation data, but experts believe such demands may eventually be introduced following Europe's lead.

In response to these upcoming requirements, China and Brazil will start discussions on traceability solutions in Dec-24, aiming to launch the first shipments of fully traceable meat in 2025. A study by the Chinese Academy of Social Sciences and the Getúlio Vargas Foundation, with support from the Nature Conservancy, found that Chinese consumers are willing to pay up to 22.5% more for beef certified as deforestation-free. China recently granted export licenses to 38 new Brazilian meat plants, including 24 for beef, the largest single authorization in the history of trade relationships.

United States

US Beef Industry Consolidates: Fewer Farms, Larger Herds Dominate

The 2022 United States Department of Agriculture (USDA) Census of Agriculture highlights a continued consolidation trend in American agriculture. United States (US) farms dropped to 1.9 million, a 7% decrease from 2017 and the lowest since 1950. Over 25 years, farm numbers have fallen by 14%, while the farming population ages, as nearly 40% of producers are now over 65 years. The US beef industry follows this trend, with beef operations down 15% since 2017 to 622,162 and the beef cow herd shrinking by 8% due to economic pressures and drought.

Agricultural consolidation is stark, with 6% of farms generating three-quarters of sales on 31% of farmland. The number of acres in production has dropped 8% over 25 years. In the beef sector, small producers face challenges as 79% of operations with fewer than 50 cows make up just 25% of the herd, while 60.5% of beef cows are in larger herds of 100 or more heads, emphasizing growth in large-scale operations.

Larger herds have expanded, with operations of more than 500 cows up by 16% since 2017. Herds of between 1,000 cows and 2,499 cows grew by 11%, and those with more than 2,500 cows increased by 4%. These two largest categories added 275,912 cows, a 10% increase. The average beef herd size rose to 47 head in 2022, reflecting the steady shift toward larger operations.

2. Weekly Pricing

Weekly Beef Pricing Important Exporters (USD/kg)

Yearly Change in Beef Pricing Important Exporters (W44 2023 to W44 2024)

.png)

Brazil

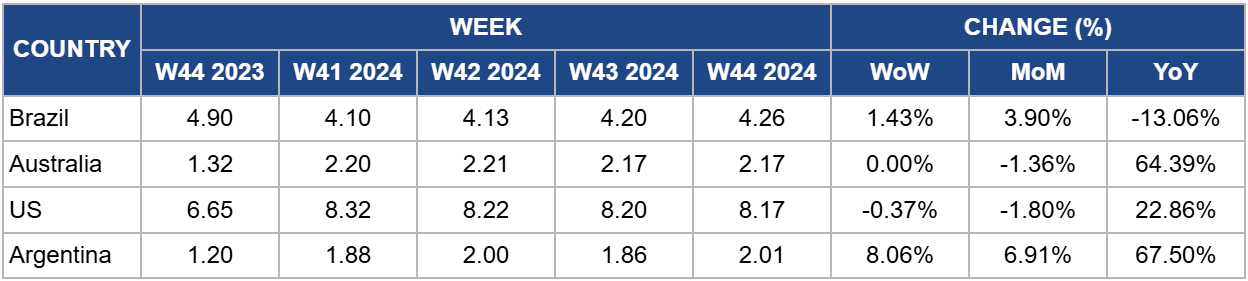

In W44, Brazil's wholesale price for boneless rear beef reached USD 4.26/kg, marking a 1.43% week-over-week (WoW) increase but remaining 13.06% lower YoY. This fourth consecutive weekly rise reflects rising demand and limited supply from restricted slaughter schedules, which Canal Rural reports as among the tightest of the season. Aggressive exports, absorbing nearly 40% of Brazilian beef production, also contribute to firm prices in the wholesale market. Safras and Mercado noted that Oct-24 saw a strong shipment pace and tight slaughter scales, leading to new seasonal price highs. This limited beef supply is expected to push up prices for competing proteins, particularly chicken meat, as wages enter the economy and drive retail and wholesale price adjustments.

Australia

Australia’s National Young Cattle Indicator averaged USD 2.17/kg in W44, remaining stable. According to Meat and Livestock Australia (MLA), the cattle market experienced modest positive movement across all indicators as yardings eased by 4,784 heads to 55,545 heads. However, processor cow prices remained stable, with throughput decreasing by 774 heads to 6,864 heads. Strength in the indicator was driven by elevated markets in Queensland and New South Wales, while the southern states of Victoria, South Australia, and Tasmania saw consecutive weeks of price declines, likely due to quality issues caused by limited feed availability.

United States

In W44, the average price of lean beef (92% to 94% lean) in the US was USD 8.17/kg, marking a 0.37% WoW decrease but a significant 22.86% YoY increase. This decline represents the eighth consecutive week of falling prices, bringing lean beef to its lowest level since W23. The drop is likely driven by a seasonal reduction in beef demand as winter approaches, following the peak summer consumption period. However, despite the decline, lean beef prices remain relatively high due to limited domestic production, driven by a shrinking cow herd and a tighter overall supply.

Argentina

In W44, Argentina's average steer beef price rose to USD 2.01/kg, reflecting an 8.06% WoW increase and marking the highest weekly price since W35. However, beef prices in Argentina have remained generally low throughout 2024, primarily due to reduced domestic demand amid the country's ongoing economic crisis. According to data from the Chamber of Industry and Commerce of Meat and Derivatives of the Argentine Republic (CICCRA), per capita beef consumption dropped by 12.3% in the first nine months of 2024, averaging 46.8 kg, which represents a 6.6 kg annual decline per person. The 12-month moving average showed a per capita consumption of 47.5 kg as of Sep-24, a 10.9% YoY decrease.

3. Actionable Recommendations

Strengthen Partnerships in Export Markets

Given the high demand for EU beef in markets like Turkey, the EU should continue to foster strong trade partnerships, particularly with countries that show stable demand for beef imports. By collaborating on trade policies and reducing barriers, EU producers can secure a steady stream of demand, helping mitigate the impact of declining domestic production. This may include offering incentives for exports to priority markets and expanding into emerging regions interested in European beef.

Implement Comprehensive Traceability Systems

To meet the EU’s deforestation regulation and upcoming Chinese traceability requirements, Brazil should prioritize a nationwide traceability system for its beef exports. Investment in technology for tracking livestock from birth through export will ensure regulatory compliance and strengthen Brazil’s standing in environmentally conscious markets. Collaboration with industry stakeholders to streamline traceability technology and data-sharing platforms will be crucial for implementation by 2025.

Additionally, as indirect suppliers present challenges for environmental compliance, Brazil should enhance support for rural producers, including training on sustainable practices and monitoring standards. By establishing partnerships with local organizations, Brazil can improve the transparency and accountability of indirect suppliers, increasing market access and ensuring sustainability across the supply chain.

Promote Diversification and Value-Added Products

Encouraging small US beef producers to diversify into value-added products, such as organic, grass-fed, or niche beef products, can help them compete in a market dominated by large-scale operations. Programs providing training in niche marketing and certifications for quality can enable smaller operations to attract premium prices in niche markets.

Sources: Portal Do Agronegocio, Canal Rural, Elagro, Beefpoint, Agromeat