1. Weekly News

Brazil

Mato Grosso's 2024/25 Corn Harvest Forecast at 45.85 MMT

The Mato Grosso Institute of Agricultural Economics (IMEA) projects Mato Grosso's 2024/25 corn harvest at 45.85 million metric tons (mmt), increasing 0.68% from the previous forecast. Improved future state corn prices, which cover the producers' Effective Operating Costs, drive this upward revision. The second-crop corn area will expand by 0.70% from the Nov-24 forecast, reaching 6.84 million hectares (ha), reflecting a 0.56% rise compared to the previous season. However, production will decline by 2.81% from last season due to a forecasted drop in average productivity.

Brazil's 2024/25 Summer Corn Planting Progress Reached 96.6%, Outpacing Last Year

The planting of the 2024/25 summer corn crop in Brazil's center-south region has reached 96.6% of the estimated 3.512 million ha, surpassing last year's progress of 90.7% and the five-year average of 93.5%. Planting has been fully completed in key states, including Rio Grande do Sul with 886 thousand ha, Santa Catarina with 583 thousand ha, Paraná with 532 thousand ha, Mato Grosso do Sul with 28 thousand ha, and Mato Grosso with 10 thousand ha. São Paulo has reached 99.1% of its 294 thousand ha, Goiás and the Federal District have achieved 98.2% of 290 thousand ha, and Minas Gerais has planted 90.5% of its 858 thousand ha, marking a strong start to the planting season.

France

France's 2024 Corn Harvest Expected to Rise 10% Despite Challenging Growing Conditions

The French General Association of Corn Producers (AGPM) projects the 2024 corn harvest to reach 13.9 mmt, a 10% year-on-year (YoY) increase from 2023's 12.6 mmt. This growth is due to a 12% expansion in cultivated areas to 1.39 million ha, with 1.28 million ha dedicated to feed corn. Despite challenging sowing conditions due to heavy rainfall and pest pressure reducing crop density, harvest progress has been delayed by three weeks, with 80% of crops threshed as of November 18. Feed corn yields are satisfactory, averaging 12.3 metric tons (mt) per ha, slightly below last year's 12.6 mt/ha.

Ukraine

Ukraine's 2024/25 MY Corn Exports Up 11.5% YoY

As of December 2, in the 2024/2025 marketing year (MY), Ukraine exported 18.38 mmt of grain and leguminous crops, marking a 37.1% increase from 4.98 mmt exported in MY 2023/24. Corn exports reached 7.21 mmt, an increase of 11.5% YoY.

United States

US Corn Exports Surged to 1.73 MMT in W49

The United States (US) sold 1.732 million tons of corn in W48, surpassing projections of 750 thousand mt to 1.5 mmt. This represents a 63% week-on-week (WoW) increase and is 4% higher than the average of the last four weeks. Mexico was the primary destination for these sales, continuing its traditional role as the leading buyer. Throughout MY 2024/25, the US has already committed 34.191 mmt of corn for export, up from just over 25.7 mmt in the same period last year. The United States Department of Agriculture (USDA) projects that total North American corn sales will reach 59.06 mmt in 2024.

2. Weekly Pricing

Weekly Maize Pricing Important Exporters (USD/kg)

Yearly Change in Maize Pricing Important Exporters (W49 2023 to W49 2024)

United States

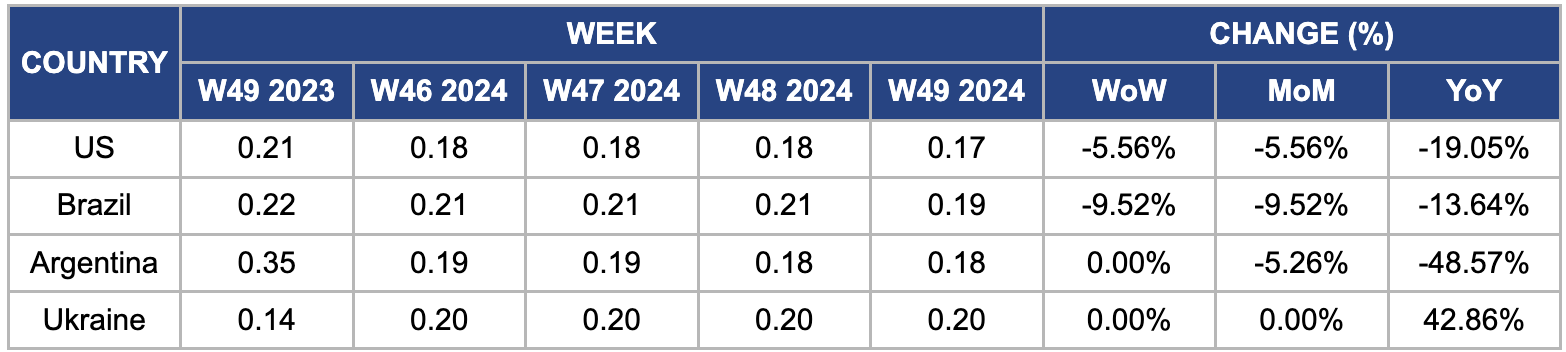

In W49, wholesale maize prices in the US fell by 5.56% WoW and month-on-month (MoM) to USD 0.17 per kilogram (kg), and by 19.05% YoY, driven by favorable weather forecasts in key corn-producing regions. These weather conditions are expected to result in strong harvests, expected to contribute to further price decline. This trend follows a forecast for a record corn yield in 2024, expected to surpass 12 mt/ha. The US corn sector has achieved significant productivity gains, with yields increasing sixfold since the 1940s, primarily due to advancements in hybrid seed genetics, biotechnology, and precision farming. Corn remains the most widely grown crop in the US in terms of acreage and output.

Brazil

In W49, wholesale maize prices in Brazil dropped significantly by 9.52% WoW and MoM to USD 0.19/kg, and by 13.64% YoY, driven by improved weather conditions and increased rainfall. According to the Center for Advanced Studies in Applied Economics (CEPEA), many corn producers, especially in São Paulo, are refraining from market negotiations as they focus on the development of the upcoming summer harvest. Favorable weather conditions in most regions have positively impacted the 2024/25 summer harvest sowing, which is now nearing its final stages in Southern Brazil.

Argentina

In W49, the wholesale price of Argentine corn remained steady WoW but declined by 5.26% MoM and 48.57% YoY, reaching USD 0.18/kg. The price drop is due to recent rainfall, which has improved crop conditions. Rainfall in Eastern Buenos Aires and Central Argentina has enhanced soil moisture levels for corn planting, with light rain expected to continue. Corn planting is currently 41.3%, with 75 to 80% planting in core areas and less than 5% in the north.Moreover, Argentina's corn sowing plans for the 2024/25 campaign are optimistic, as the Dalbulus Maidis National Monitoring Network reported reduced leafhopper and disease pressure. The Association of Argentine Cooperatives (ACA) predicts increased planting of late corn varieties. Although these varieties yield less than early corn, they can still be profitable with proper management. The Rosario Stock Exchange projects that nearly 8 million ha will be planted, with potential production estimated at 51 to 52 mmt.

Ukraine

In W49, Ukrainian wholesale maize prices remained stable at USD 0.20/kg WoW but saw a 42.86% year-on-year increase. Due to dry weather conditions, the price rise is due to the USDA's downward revision of Ukraine's corn harvest forecast by 1 million metric tons to 26.2 million metric tons (mmt). Despite this, Ukraine faces challenges with a 13% YoY decline in exports through the Constanta Port, mainly due to its reliance on deep-sea ports. The Ministry of Agrarian Policy and Food confirmed the completion of the harvest season, with a total grain collection of 53.9 million metric tons. Although reduced exports could typically lower prices, logistical issues contribute to higher costs.

3. Actionable Recommendations

Diversify Export Markets to Reduce Dependence on Single Trade Partners

Mexico should prioritize diversifying its export markets to shield its corn producers from market fluctuations and geopolitical risks. Recent trends show that reliance on key destinations like the US can expose risks due to supply chain disruptions or policy changes. Corn exporters should actively explore partnerships with emerging markets in Asia and North Africa through trade agreements and strategic alliances. This approach ensures sustained demand for corn exports while mitigating risks associated with over-reliance on a few key trading partners.

Strengthen Logistics Infrastructure to Enhance Market Access

Brazil should focus on modernizing its logistics infrastructure to ensure efficient market access for its corn exports. Recent disruptions, such as transportation delays caused by climatic impacts and expanded production areas, highlight the need for better connectivity. Investments in improved port facilities, modern rail networks, and efficient transport systems are critical. Strengthened infrastructure will ensure that corn reaches global markets timely, reducing bottlenecks and market price instability while increasing competitiveness.

Adopt Weather-Resilient Farming Technologies to Combat Climate Variability

Ukraine should invest in advanced farming technologies to ensure productivity during extreme weather events. With recent trends showing dry weather impacting harvest projections, adopting technologies such as drought-resistant hybrid corn seeds like Bt (Bacillus thuringiensis) and drought-tolerant transgenic varieties, advanced irrigation methods like drip and subsurface irrigation, and precision farming tools like GPS-guided machinery and soil moisture sensors can stabilize yields. These hybrid seeds can withstand low rainfall conditions and resist pests, ensuring better performance in challenging climates. Furthermore, precision farming tools can optimize resource usage by applying water, fertilizers, and pesticides, enhancing crop efficiency and reducing waste. These strategies will ensure consistent production and provide stability against unpredictable weather shifts, addressing the risks of climate change and regional drought patterns.

Sources: Tridge, Zol, Agrotimes, Portal Do Agronegócio, NoticiasAgricolas, UkrAgroConsult