W8 2025: Palm Oil Weekly Update

In W8 in the palm oil landscape, some of the most relevant trends included:

- The palm oil industry is threatened by climate change, with droughts and rising temperatures reducing yields in regions like Indonesia and Colombia, Indonesia’s production has declined by up to 10% annually in some areas.

- Indonesia's 2024 palm oil production is projected to drop to 48 mmt, while Malaysia's output is also impacted by monsoon rains. Despite lower production, strong biodiesel demand and stock replenishment in China and India are sustaining demand.

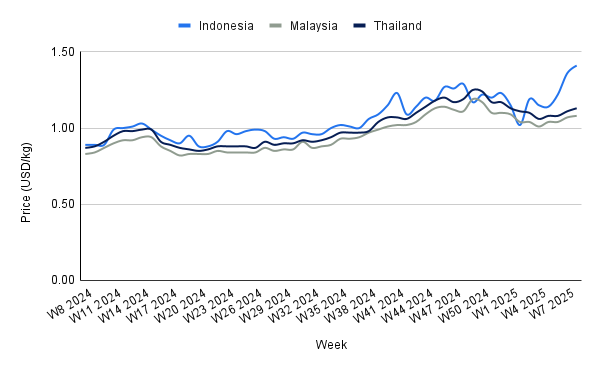

- Palm oil prices have risen significantly, with Indonesia reaching USD 1.41/kg and Malaysia USD 1.08/kg, reflecting a 30% YoY increase. This is driven by reduced production, higher export taxes, and growing biodiesel demand.

- Indonesia and Malaysia saw declines in palm oil exports in Jan-25, particularly to India, Pakistan, and China, impacting export value, though the market remains resilient.

- Papua New Guinea will join the CPOPC, with its palm oil sector generating USD 1.1 billion

1. Weekly News

Global

Climate Change Threatens Palm Oil Yields as Indonesia and Colombia Develop Resilience Strategies

The palm oil industry is increasingly threatened by climate change, with prolonged droughts and rising temperatures reducing yields in key producing regions. In Indonesia, areas like Lampung and South Kalimantan have seen production declines of up to 10% annually, potentially leading to USD 4.6 billion in losses. To address this, the Sinar Mas Agribusiness and Food Research Institute (SMART) Research Institute has developed drought-tolerant palm oil varieties, SD14 and SD63, which maintain 14 to 27% higher yields under extreme drought conditions. SD14 is currently awaiting official release approval. Meanwhile, Colombia's palm oil sector faces similar challenges, with 168,000 hectares (ha) lost in 15 years due to climate-related disease outbreaks. Research by Colombia's Oil Palm Research Center (Cenipalma) indicates that improved irrigation and soil conservation techniques can significantly mitigate productivity losses, while genomic selection and optimized fertilizers are being explored to enhance resilience.

India

Indian Refiners Cut Palm Oil Imports Amid Rising Prices and Weak Margins

Indian refiners have canceled 100,000 metric tons (mt) of crude palm oil (CPO) shipments for Mar-25 to Jun-25 due to rising Malaysian prices and negative refining margins. Palm oil futures surged over 11% in four weeks, making soybean oil a more attractive alternative. India's palm oil imports dropped 45% in Jan-25 to a 14-year low of 275,241 mt as refiners shifted to soybean oil from Argentina and Brazil. Market speculation on higher Indian import duties further pressured palm oil demand. These cancellations may cap Malaysian palm oil prices but could support soybean oil.

Indonesia

Indonesia's Palm Oil Exports Drop 24.1% MoM in Jan-25

Indonesia's palm oil exports experienced a significant decline in Jan-25, with a 24.1% month-on-month (MoM) drop in volume to 1.27 million metric tons (mmt) compared to Dec-24. The export value also fell by 16.68% year-on-year (YoY), from USD 1.72 billion in Jan-24 to USD 1.44 billion in Jan-25. Major markets, including India, Pakistan, and China, saw steep import declines. Exports to India decreased by 43.65%, while exports to Pakistan and China dropped by 52.92% and 76.93%, respectively. Despite the downturn, palm oil remains a key export, contributing 7.04% to Indonesia's non-oil and gas exports. Indonesia plans to increase the mandatory biodiesel blend to 50% in 2026 to reduce diesel imports.

Indonesia Targets 120,000 HA of Smallholders' Palm Oil Replanting in 2025

Indonesia aims to replant 120,000 ha of smallholders’ palm oil plantations in 2025, funded through the state plantation agency, which manages the palm oil export levy. The program, which also includes up to 10,000 ha for cocoa, is part of broader efforts to support smallholders and maintain long-term productivity. In 2024, only 38,247 ha of palm oil plantations were replanted, falling short of the 70,000 ha target due to land legality issues and high palm oil prices. Smallholders receive USD 3,700/ha (IDR 60 million/ha) for replanting, though funding details for cocoa remain undisclosed.

Malaysia

Malaysia Maintains 10% Palm Oil Export Duty for Mar-25

Malaysia will maintain its CPO export duty at 10% for Mar-25, according to the Malaysian Palm Oil Board (MPOB). The base price for March declined by USD 96.53/mt (MYR 427.33/mt) to USD 991.79 (MYR 4,390.37/mt). Malaysia’s palm oil export duty follows a tiered structure, reaching 10% when prices exceed USD 914.89/mt (MYR 4,050/mt). In Jan-25, the country’s palm oil exports fell by 12.94% YoY to 1.17 mmt.

Papua New Guinea

Papua New Guinea Set to Join CPOPC, Boosting Sector's Economic Impact

Papua New Guinea is set to join the Council of Palm Oil Producing Countries (CPOPC) as its fourth member. Council members from Indonesia, Malaysia, and Thailand are in Port Moresby to finalize Papua New Guinea's membership. Papua New Guinea’s Oil Palm Industry generates USD 1.1 billion (PGK 2.9 billion) in revenue, benefiting farmers and supporting sustainable projects. Approximately 500,000 families are employed in the palm oil sector, highlighting its significant role in the country's economy.

2. Weekly Pricing

Weekly Palm Oil Pricing Important Exporters (USD/kg)

Yearly Change in Palm Oil Pricing Important Exporters (W8 2024 to W8 2025)

Indonesia

Indonesia’s palm oil prices rose to USD 1.41 per kilogram (kg) in W8, reflecting a 3.68% week-on-week (WoW) increase and a 58.43% YoY surge, driven by lower production, higher domestic biodiesel demand, and rising export taxes. CPOPC estimates Indonesia’s 2024 production at 48 mmt, down from 50.07 mmt in 2023. Despite the supply contraction, demand remains strong, supported by the B40 biodiesel mandate and stock replenishment in key importing nations like China and India.

However, soybean oil's price advantage may pressure palm oil’s competitiveness. In addition, Indonesia’s export tax hikes contributed to the price surge, impacting global market dynamics. Going forward, palm oil prices may remain elevated due to tight supplies and rising biodiesel demand, but competition from cheaper soybean oil and potential shifts in global vegetable oil trade could limit upside potential.

Malaysia

Malaysia’s palm oil prices increased to USD 1.08/kg in W8, reflecting a 0.93% WoW rise and a 30.12% YoY increase. This price surge is supported by reduced production forecasts due to monsoon rains in East Malaysia, expected to impact output from February 21 to 25, 2025. In addition, the export tax on crude palm oil for Mar-25 remains at 10%, with a lowered reference price of USD 988.38/mt (MYR 4,390.37/mt).

The continuation of the export tax and lowered reference price could put upward pressure on prices by maintaining a balance between domestic supply constraints and export competitiveness, especially in key markets like China and India. However, the premium over soybean oil remains a challenge in attracting demand, particularly in price-sensitive regions. Should production issues persist, price volatility may rise, reinforcing higher price levels in the short term while balancing out with a more cautious outlook for demand growth in the medium term.

Thailand

Thailand’s palm oil prices increased to USD 1.13/kg in W8, reflecting a 1.80% WoW rise and a 29.89% YoY increase. The surge in prices has raised concerns, particularly regarding bottled palm oil shortages, with prices rising from USD 1.35 per liter (THB 45.5/L) in Aug-24 to 1.70/L (THB 57.5/L) in Feb-25.

Despite sufficient domestic production, the price hike has led to accusations of market manipulation and stockpiling by private players, reminiscent of the 2008 palm oil crisis. If such practices persist, it could lead to consumer unrest and political fallout, potentially destabilizing both local markets and public confidence. This situation may prompt further government intervention, with potential implications for future price volatility, particularly if the government fails to stabilize the market and restore consumer trust.

3. Actionable Recommendations

Adopt Climate-Resilient Palm Oil Varieties

Given the increasing threat of climate change, palm oil producers should invest in drought-tolerant varieties like SD14 and SD63, which have demonstrated up to 27% higher yields under extreme conditions. Governments and industry bodies can facilitate the adoption of these varieties by offering subsidies, technical support, and incentives for research institutes to accelerate approvals and distribution. This strategy would mitigate the risk of yield losses from droughts and ensure more stable production levels, particularly in vulnerable regions like Indonesia and Colombia.

Implement Enhanced Irrigation and Soil Conservation Techniques

With climate-related disease outbreaks and productivity losses in key regions such as Colombia, palm oil producers should prioritize improving irrigation and soil conservation practices. Farmers can adopt modern irrigation systems, such as drip irrigation, and implement soil health management techniques to ensure consistent production. Governments should support these initiatives by providing grants or low-interest loans for infrastructure improvements and offering training programs for smallholders on best practices in water management and soil preservation.

Expand Biodiesel Mandates to Strengthen Domestic Demand

To offset declining export volumes and global price fluctuations, Indonesia's palm oil sector should continue expanding its biodiesel mandates, such as the B40 and planned B50 mandates. This would not only reduce dependence on foreign diesel but also create a stable domestic market for palm oil, driving demand despite global market pressures. Collaboration with industry stakeholders to scale up biodiesel production facilities and streamline distribution channels would further bolster this strategy, helping to sustain the palm oil market in the face of global price volatility.

Sources: Tridge, Rosng, Noticias Agricolas, Grain Trade, UkrAgroConsult, News Foodmate, Reccessary, Producer, Nation Thailand, ABC