In W16 in the soybean oil landscape, some of the most relevant trends included:

- Bangladesh raised retail prices of soybean oil after import duty exemptions expired on March 31, with prices up USD 0.12/L due to increased import costs.

- Nepal's refined soybean oil exports to India surged over 60-fold, prompting Indian industry backlash over allegedly misusing trade agreements and harming domestic producers.

- Argentina's soybean oil prices declined amid weak global demand and strong output, with processing projected at 41.5 mmt for 2024/25. Prices may remain under pressure unless demand rebounds.

- Brazil’s soybean oil prices rose WoW due to strong Chinese demand, driven by a pivot away from US suppliers.

1. Weekly News

Bangladesh

Bangladesh Raises Soybean Oil Prices Following Expired Import Duty Exemptions

The government of Bangladesh has raised the retail price of bottled soybean oil by USD 0.12 per liter (BDT 14/L), setting the new price at USD 1.56/L (BDT 189/L), up from USD 1.44/L (BDT 175/L). The price of loose soybean oil has also increased to USD 1.39/L (BDT 169/L) from USD 1.29/L (BDT 157/L). The adjustments follow the expiry of import duty exemptions on March 31 and were influenced by global market trends. The decision was announced by a senior commerce official following consultations with stakeholders after refiners had earlier requested a price increase due to rising import costs.

India

India Raises Alarm Over Surge in Refined Soybean Oil Imports from Nepal Amid SAFTA Concerns

Refined soybean oil exports from Nepal to India have surged over 60-fold in the first eight months of the current fiscal year, raising alarms among Indian oil producers. Nepal exported over 228,000 metric tons (mt) of refined soybean oil during this period, despite importing large volumes of crude oil from countries such as Argentina and Brazil. Indian industry groups argue that the trade violates South Asian Free Trade Area (SAFTA) rules and harms domestic refiners and oilseed farmers.

India’s increased import duties in late 2023 appear to have triggered trade redirection through Nepal, exploiting the zero-duty access under the India-Nepal Trade Treaty. The Indian Vegetable Oil Producers’ Association (IVPA) and the Solvent Extractors’ Association of India (SEA) have called for regulatory interventions, including shifting ports of entry, imposing a 10 to 15% cess on refined oils, implementing import quotas, and mandating stricter origin documentation.

Nepali exports are reportedly repackaged processed oils with minimal local value addition, raising concerns about regulatory compliance. Indian officials are considering policy responses to curb duty circumvention and protect domestic industries.

2. Weekly Pricing

Weekly Soybean Oil Pricing Important Exporters (USD/kg)

Yearly Change in Soybean Oil Pricing Important Exporters (W16 2024 to W16 2025)

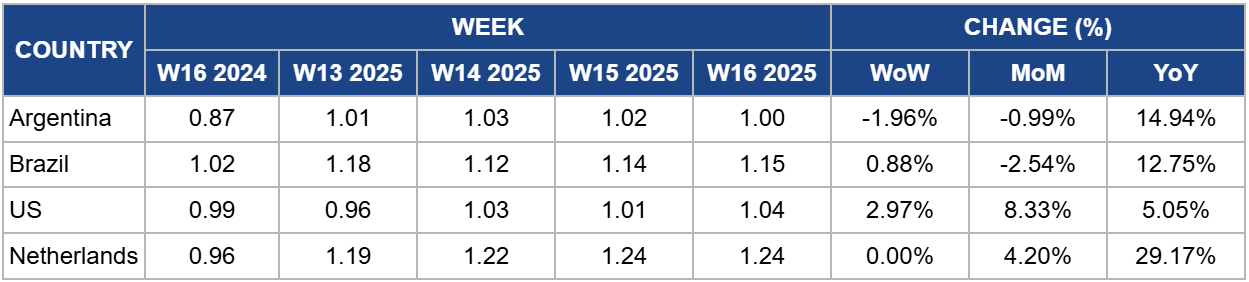

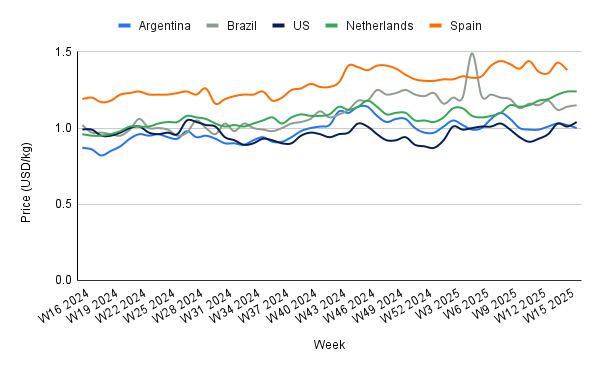

Argentina

Argentina's soybean oil prices fell to USD 1 per kilogram (kg) in W16, down 1.96% week-on-week (WoW), reflecting weaker global demand and robust supply expectations. Despite a projected 3.5% decline in soybean processing to 41.5 million metric tons (mmt) for the 2024/25 season, overall processing remains 14% above the five-year average, supporting relatively high oil output.

Soybean oil production is estimated at 8.2 mmt, 400,000 mt lower than in 2023/24 but still 800,000 mt above the five-season average. This elevated supply and softening export prices suggest continued pressure on Argentina's domestic and export prices in the near term. Key export destinations, such as India, Bangladesh, China, Peru, and Mozambique, will play a crucial role in market stabilization. Sustained or rising demand from these countries could help offset price declines. Argentina's soybean oil prices may face limited short-term recovery unless global demand improves or competing suppliers face disruptions. However, strong export volumes and Argentina's leading role in the global soybean oil trade may offer medium-term price support.

Brazil

In W16, Brazil's soybean oil prices rose to USD 1.15/kg, marking a 0.88% WoW and 12.75% year-on-year (YoY) increase. This price uptick is driven by surging Chinese demand, as Beijing pivots away from United States (US) suppliers following the imposition of new tariffs. Chinese buyers began accelerating Brazilian purchases even before the new US tariffs were enacted, signaling strategic shifts in sourcing. The Brazilian Association of Vegetable Oil Industries (Abiove) has acknowledged this rising demand but emphasized the need to maintain domestic processing levels to support national supplies of vegetable oil and biodiesel.

While this short-term boost supports Brazilian soybean oil prices, long-term price direction will depend on whether domestic crushing capacity keeps pace with increased export interest. If processing remains prioritized domestically, prices could remain elevated due to limited external availability. However, broader trade disruptions and logistical uncertainties linked to the global trade environment may introduce volatility going forward.

United States

US soybean oil prices increased to USD 1.04/kg in W16, rising 2.97% WoW and 5.05% YoY, supported by firm domestic demand despite tightening export prospects. Recent trade tensions with China, including retaliatory tariffs of up to 245% and import suspensions—have curbed US soybean oil exports, especially to China, which typically accounts for over 40% of US exports. This redirection of supply toward the domestic market has added downward pressure on inventories, though rising demand for renewable diesel continues to offer partial support. However, the domestic market has limited capacity to absorb large surpluses, raising concerns about potential oversupply if crushing volumes remain elevated and export growth stagnates.

Despite record early export commitments for the 2025/26 marketing year (MY) and a strong 2024/25 export pace, fueled by high global vegetable oil prices, the export outlook remains uncertain. South America, particularly Brazil, is strengthening its competitive edge in China, potentially displacing US market share. US soybean oil prices may stay supported by robust internal demand and high global oilseed prices. However, sustained trade friction, limited export alternatives, and growing South American competition could cap future price gains and contribute to increased market volatility.

Netherlands

In W16, soybean oil prices in the Netherlands held steady at USD 1.24/kg for the second consecutive week, reflecting a 4.20% month-on-month (MoM) and 29.17% YoY increase. This sustained strength highlights firm domestic and regional demand amid tightening global supplies and rising geopolitical tensions. As a major European Union (EU) hub for soybean imports, particularly from the US, the Netherlands faces increased risk of supply disruption following the EU's approval of retaliatory tariffs on US agricultural goods, including soybeans. Should these duties be implemented, US soybean flows to the Dutch market may decline, potentially tightening availability for crushing operations and supporting further price firmness.

3. Actionable Recommendations

Adapt to Evolving Trade Dynamics in South Asia

With Nepal’s refined soybean oil exports to India surging and raising compliance concerns, Indian importers and regulators should prioritize stricter enforcement of origin rules under SAFTA and the India-Nepal Trade Treaty. Introducing traceability systems and mandating value-addition thresholds will help prevent duty circumvention, protect domestic processors, and ensure fair market access. Importers may also diversify sourcing to include certified suppliers from Argentina or Brazil to reduce over-reliance on repackaged Nepali exports.

Secure Supply Amid Southeast Asian Price Volatility

As Bangladesh's soybean oil prices rise due to the expiration of import duty exemptions and global market pressures, local refiners and distributors should explore forward contracts with key exporters like Argentina and Brazil to lock in competitive prices. Additionally, developing regional storage infrastructure could buffer short-term price shocks and support more stable consumer pricing during periods of global supply disruption.

Strengthen Market Resilience Against Export Redirection

Given ongoing trade friction between the US and China and the resulting shift in Chinese demand toward Brazilian soybean oil, global importers, particularly in India, Bangladesh, and the EU, should reassess their procurement strategies. Establishing flexible sourcing frameworks and diversifying suppliers can mitigate exposure to geopolitical disruptions and supply concentration risks. Market actors should also monitor shifts in crushing capacity in key origin countries to anticipate changes in export availability.

Sources: Tridge, Asia News, United News of Bangladesh, Clarín, Reuters