In W17 in the onion landscape, some of the most relevant trends included:

- Argentina's onion growers face critical economic strain due to low farmgate prices well below production costs, rising input expenses, and declining export competitiveness amid cheaper regional imports.

- In Bangladesh prices surged due to limited supply and stockpiling by farmers and traders. Bangladesh's government policies, such as import suspensions, have further tightened market conditions.

- Uzbekistan's onion exports are seeing strong demand and significantly higher prices, driven by reduced winter plantings and renewed interest from regional buyers like Russia and Belarus.

- India's stable yet lower YoY onion prices result from a production rebound and government-led buffer stock strategies aimed at curbing inflation and post-harvest losses, though continued oversupply may suppress prices

1. Weekly News

Argentina

Mendoza Onion Producers Struggle with Losses as Costs Soar and Imports Undercut Market

Onion producers in Mendoza, Argentina, are facing severe economic challenges in 2025, marked by low profitability, rising input costs, and weak domestic and export demand. Small and medium-scale farmers report selling prices far below production costs, at USD 0.43 to 0.85 per 20-kilogram bag (ARS 500 to 1,000/20-kg bags), while retail prices remain significantly higher. The situation is compounded by increased costs for seeds, fertilizers, fuel, and labor, discouraging further investment and leading to reduced cultivation. Export opportunities have diminished due to competition from cheaper imports, especially from Brazil and Peru. Many producers face total losses, prompting concerns over the long-term viability of onion farming in the region.

Bangladesh

Bangladesh Onion Prices Spike Over 23% MoM Amid Import Suspension and Strategic Stockpiling

Onion prices in Bangladesh have surged sharply in recent weeks despite the peak harvesting season, driven by reduced market supply and a suspension of imports as of W17. Farmers and traders are withholding high-quality stocks in hopes of better returns, following earlier low prices that failed to cover production costs. Retail prices in Dhaka have climbed to around USD 0.57/kg (BDT 70/kg), up by over 23% month-on-month (MoM), while wholesale rates in key producing regions like Pabna and Faridpur have more than doubled. The government's Mar-25 decision to halt imports, intended to support domestic growers, has tightened market supplies, with both farmers and traders now storing onions to sell strategically, anticipating further price increases.

Ukraine

Ukrainian Yellow Onion Prices Rose 55% WoW Due to Supply Shortages and Strong Demand

Yellow onion prices in Ukraine have surged by 55% week-on-week (WoW) due to dwindling farm stocks and strong wholesale demand. Farmers are now selling at USD 0.34 to 0.49/kg (UAH 14 to 20/kg), with many holding back remaining stocks amid limited high-quality supply. As of W17, prices are 59% higher year-on-year (YoY), and the upward trend is expected to continue until the arrival of the new harvest.

Uzbekistan

Uzbekistan Launches New Onion Export Season

Uzbekistan has commenced exporting its new-season bulb onions as of mid-Apr-25, with initial shipments priced at USD 0.40 to 0.45/kg, free carrier (FCA), approximately double the rates seen during the same period last year. The price surge is primarily attributed to a significant reduction in winter onion planting in late 2024. Despite higher prices, demand remains strong, with major Russian and Belarusian retailers initiating procurement tenders. Onions remain Uzbekistan’s largest vegetable export by volume, with over 64,000 metric tons (mt) shipped in Q1-2025.

2. Weekly Pricing

Weekly Onion Pricing Important Exporters (USD/kg)

Yearly Change in Onion Pricing Important Exporters (W17 2024 to W17 2025)

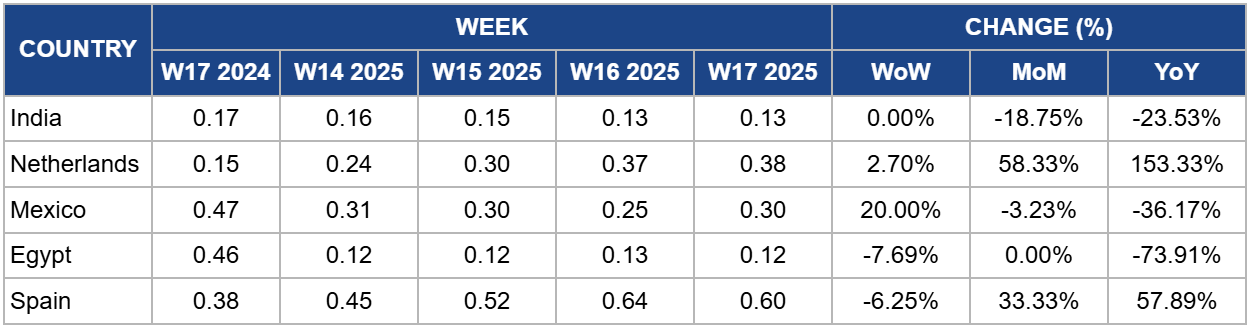

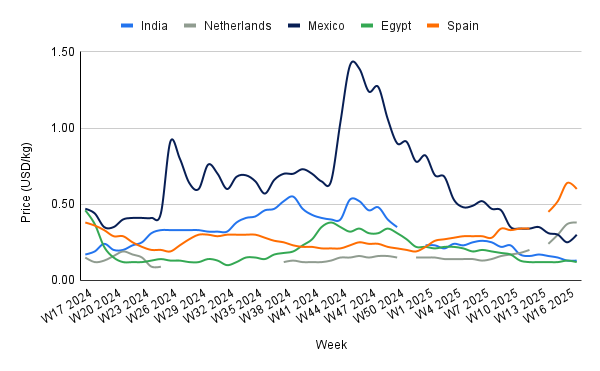

India

In W17, India's onion prices remained stable at USD 0.13/kg, unchanged WoW but down 23.53% YoY. This decline is linked to a strong rebound in domestic production, which is expected to rise 19% to 28.88 million metric tons (mmt) in the 2024/25 crop year, following a poor harvest last year. The increased supply has eased retail inflation, with food inflation falling to 2.69% in Mar-25, its lowest in over a year. To manage volatility and prevent price spikes during the August–November festive season, the government will store onions at 90 decentralized locations and involve private firms in procurement and logistics under the Price Stabilization Fund (PSF). This proactive strategy, combined with buffer stock releases, is designed to temper seasonal inflation while preventing waste, as post-harvest losses typically claim about 25% of the crop. The policy ensures consumer affordability but may pressure farmgate prices if oversupply continues and export demand remains weak. Experts stress fair pricing and timely payments to protect farmers. While the buffer stock system could stabilize prices short-term, oversupply risks may keep prices low through mid-2025 unless exports increase.

Netherlands

In W17, onion prices in the Netherlands rose to USD 0.38/kg, an increase of 2.70% WoW and 153.33% YoY, driven by tight domestic supply and strong export demand. Heavy autumn rains in 2023/24 damaged harvests in key regions like Zeeland and Flevoland, reducing marketable stocks by nearly 25% compared to the five-year average. Rising exports to West Africa and Southeast Asia, along with an 18% YoY increase in energy and storage costs, added further upward pressure. If export momentum continues and domestic supplies remain limited, elevated prices may persist through mid-2025.

Mexico

In W17, Mexico’s onion prices rose by 20% WoW to USD 0.30/kg, though still down 36.17% YoY from USD 0.47/kg. The recent uptick reflects short-term supply adjustments, but broader market conditions remain weak due to regional oversupply. In Sinaloa, an important production hub, the excess output of onions has depressed prices. If this trend continues, onion prices may remain under pressure despite temporary increases, especially in the absence of stronger domestic demand or export relief. Elevated plantings following last year’s favorable conditions and water concerns further heighten the risk of prolonged price volatility.

Egypt

In W17, Egypt's onion prices fell to USD 0.12/kg, down 7.69% WoW and 73.91% YoY from USD 0.46/kg, reflecting continued market saturation. The sharp YoY decline stems from significant overproduction in 2024 when output exceeded 3 mmt as farmers expanded acreage in response to earlier price spikes. However, sluggish domestic and export demand in 2025 has led to persistent surpluses and weak pricing. Although a modest price recovery was seen recently with the start of the export season, ongoing supply-demand imbalances and rising input costs suggest prices may remain low in the near term unless international demand strengthens.

Spain

Spain's onion prices fell to USD 0.60/kg in W17, a decrease of 6.25% WoW, yet 57.89% higher YoY from USD 0.38/kg. This decline reflects a normalization following years of above-average yields, as national supply in 2024 exceeded demand despite a 14.9% drop in production. Average onion prices have stabilized compared to 2023 peaks, supported by still-elevated production costs and increasing storage expenses. Although current prices remain profitable, rising input costs, irrigation restrictions, and consumer demand pressures may limit further gains. The outlook for 2025 points to gradual price recovery if production stabilizes and domestic consumption rebounds.

3. Actionable Recommendations

Enhance Export Competitiveness Through Regional Trade Diversification

To counter declining export opportunities, especially in Argentina and Egypt, producers and exporters should diversify market access beyond traditional destinations like Brazil and Peru. By engaging in trade missions and bilateral agreements with underserved markets in Africa, the Middle East, and Southeast Asia could help unlock new demand. Additionally, investment in export-grade packaging, certification, and logistics infrastructure can improve the competitiveness of onions in higher-value markets.

Promote Strategic Stock Management and Transparent Pricing Mechanisms

In countries like Bangladesh and Ukraine, where hoarding and speculative trading are distorting markets, governments and cooperatives should implement monitored storage systems and promote transparent, real-time pricing platforms. These measures can stabilize market conditions, reduce price manipulation, and improve market access for smallholders and buyers.

Sources: Tridge, Asian News Network, Fresh Plaza, East Fruit, Los Andes, Mint, Municipios, Valencia Fruits