In W17 in the soybean landscape, some of the most relevant trends included:

- Argentina’s soybean harvest is progressing slowly, but yields remain above expectations, keeping production stable at 48 mmt. Harvesting has reached just 2.6% due to delays, but strong yields averaging 3.54 mt/ha have offset concerns, allowing the overall production estimate to remain unchanged.

- Brazil continues to dominate global supply, with 89% of its soybean crop harvested and strong Chinese demand shifting away from Argentina.

- Soybean prices diverged across key exporters in W17, with declines in Brazil and Argentina, a rise in the US, and stable prices in Uruguay. Brazilian and Argentine prices fell due to ample supply and economic pressures, while US prices rose on planting delays and strong Chinese demand.

1. Weekly News

Argentina

Argentina’s Soybean Harvest Lags Behind 2024 Pace

Soybean harvesting in Argentina has begun and is gradually expanding across key regions, with 2.6% of the crop harvested as of April 9, compared to 10.6% in 2024 and a 3% average. In the south, 27% of late-planted soybeans have entered the grain-filling stage. Frost in northern La Pampa and western Buenos Aires affected fields unevenly, with the extent of the damage to be evaluated in the coming days. The average soybean yield is currently 3.54 metric tons (mt) per hectare (ha), which is above expectations, leading the soybean estimate to remain unchanged at 48 million metric tons (mmt) in 2025. As of April 9, the Buenos Aires Grain Exchange (BAGE) reports the following soybean ratings for the 2024/2025 season: 21% of soybeans are rated poor/very poor, 42% fair, and 37% good to excellent, with the latter increasing by 1% from the prior week. Soil moisture is rated 27% short to very short, 72% favorable/optimum, and 1% saturated, with the favorable/optimum percentage dropping by 15% from the previous week.

Brazil

Brazil's 2024/2025 Soybean Harvest Estimate Holds Steady at 169 MMT

The 2024/2025 Brazil soybean harvest estimate remains unchanged at 169 mmt, with a neutral outlook. The soybean harvest in Brazil is nearing completion, except in Rio Grande do Sul, where wet weather has caused delays. As of W17, 89% of Brazil's soybeans were harvested, compared to 85% at the same time last year and 88.9% on average. In Rio Grande do Sul, soybean harvesting reached 50.6%. Moreover, W17 saw a record number of more than 60 vessels of soybeans purchased by China from Brazil.

China

China’s US Soybean Imports Surge 12% YoY in Mar-25

China's soybean imports from the United States (US) rose 12% year-on-year (YoY) in Mar-25, as shipments purchased in late 2024 arrived at Chinese ports. This surge was due to buyers concerned about the potential for a US-China trade conflict. In Mar-25, China imported 2.44 mmt of soybeans from the US, accounting for nearly three-quarters of its total imports, according to the General Administration of Customs (GACC). In Q1-25, US soybean shipments to China rose 62% YoY, totaling 11.6 mmt, while shipments from Brazil fell 55% YoY to 4.5 mmt.

However, Brazil is expected to dominate the Chinese market in the coming months as its harvest season begins.

Paraguay

Paraguay's Soybean Production to Increase to 10.9 MMT in 2025/26 After Weather-Related Setbacks

Paraguay's soybean production will increase to 10.9 mmt in the 2025/26 marketing year (MY), driven by improved weather conditions and a modest increase in the planted area after weather-related losses in the previous year. Crushing will rise to 3.4 mmt, fueled by higher domestic supplies and improved crush margins.

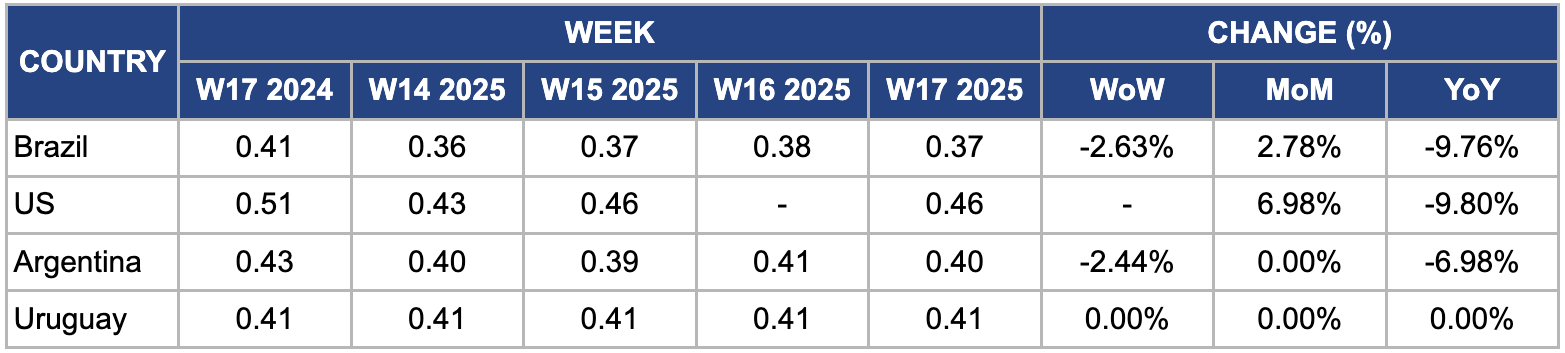

2. Weekly Pricing

Weekly Soybean Pricing Important Exporters (USD/kg)

Yearly Change in Soybean Pricing Important Exporters (W17 2024 to W17 2025)

Brazil

In W17, Brazil's soybean prices declined by 2.63% week-on-week (WoW) to USD 0.37 per kilogram (kg) despite strong export demand. This drop is mainly due to the abundant 2024/25 soybean production, estimated at 169 mmt, which has led to ample domestic supply. The harvest progress reached 89% nationwide, outpacing last year’s 85% and aligning with the 88.9% historical average, adding further downward pressure on prices. Although export premiums remained firm due to strong Chinese demand and limited supply from drought-stricken Argentina, oversupply and rapid harvest pace in Brazil outweighed these bullish factors. Moreover, the weakening Brazilian real improved export competitiveness but did not fully offset the price decline caused by the big harvest.

United States

In W17, US soybean prices rose 6.98% month-on-month (MoM) to USD 0.46/kg, up from USD 0.43/kg in W14. This increase was due to concerns over delayed planting progress in key US soybean-producing states, as wet weather disrupted fieldwork and sowing schedules. Moreover, tightening global soybean supplies has supported price gains. Strong demand from China, the largest importer of US soybeans, also contributed to upward pressure on prices as export volumes remained robust through Apr-25.

Argentina

In W17, Argentina's soybean prices declined 2.44% WoW and 6.98% YoY to USD 0.40/kg, driven by tightening supply and economic pressures. Severe drought conditions weighed heavily on the 2024/25 soybean crop, significantly reducing yields and limiting availability for domestic use and exports. At the same time, Argentina struggled to maintain its competitiveness in global markets, with weak demand from key buyers like China shifting more interest toward Brazil's higher, more reliable supply. Domestically, high inflation and economic instability pushed production costs up and slowed farmer sales as producers held back in hopes of better exchange rates. Furthermore, government policies, including export taxes and restrictions, added further uncertainty, prompting traders to adopt a cautious approach and reduce sales activity.

Uruguay

In W17, Uruguay's soybean prices remained steady WoW at USD 0.41/kg, reflecting a balance between recovering domestic production and subdued global market conditions. Following a severe drought in 2023 that slashed output to 700 thousand mt, Uruguay's 2024/25 soybean harvest rebounded significantly, with production estimated at 3.1 mmt. This recovery was supported by favorable weather conditions and improved yields, bringing production levels closer to the five-year average. Despite the production rebound, international soybean prices have been under pressure due to record harvests across South America, particularly in Brazil, leading to an oversupply internationally.

3. Actionable Recommendations

Improve Post-Frost Crop Assessment and Strategic Sales Timing

Argentina should immediately address the challenges facing its soybean market due to frost damage in northern La Pampa and western Buenos Aires. The country must accelerate post-frost evaluations using advanced tools like satellite imagery and field surveys to assess the full extent of the damage. These assessments will be crucial for determining yield losses and helping farmers decide when to sell. To address the impact of high inflation and economic instability, Argentina should implement strategies to encourage farmers to sell at the right time despite the current holdback in sales. If crop losses are less severe than anticipated, farmers should wait for price recoveries, particularly as global markets continue to favor Brazil’s supply. However, with weakened demand from key buyers like China, Argentina must optimize sales timing to avoid missing out on better exchange rates or potential price hikes.

Capitalize on Weak Real and Strong Chinese Demand with Forward Contracts

Brazil’s soybean market is experiencing a surplus due to abundant production. Despite this, there is an opportunity for farmers and cooperatives to leverage the weaker Brazilian real and strong demand from China by locking in prices through forward contracts or other hedging tools. As the Brazilian harvest nears completion and exports continue to be in demand, particularly from China, this strategy will help ensure favorable export margins. While the large harvest has exerted downward pressure on domestic prices, the ongoing strength in Chinese soybean demand and the weak real make this a crucial moment for Brazilian producers to secure profits before any further logistical bottlenecks or weather-related challenges affect supply. Forward contracts will mitigate the risk of price fluctuations, allowing Brazilian exporters to continue capitalizing on export premiums despite the recent price drops.

Sources: Tridge, Chacra Magazine, Oilworld, UkrAgroConsult