.jpg)

In W19 in the olive oil landscape, some of the major trends include:

- The EC is consulting on potential retaliatory tariffs on 95 billion US dollars worth of US goods, including olive oil, which is part of 10.5 billion US dollars in targeted US food exports. This could increase trade uncertainty and create cost pressures for olive oil exporters.

- Spain's olive oil sector shows a strong recovery in the 2024/25 season, with production more than doubling to 1.41 mmt, strong domestic and export sales (+27% YoY), and growing international recognition despite rising costs and labor shortages.

- Italy's 2024/25 olive oil harvest fell 32% YoY due to drought, pests, and disease, pushing prices higher amid firm global demand and new US 20% tariffs on EU imports, creating export cost uncertainties and potential shifts toward intra-EU trade.

- India's olive oil market is expanding rapidly, reaching USD 183 million in 2024 and projected to grow to USD 221 million by 2028, driven by health trends. However, high tariffs of 45% and limited rural reach remain key challenges, with Spanish producers maintaining market dominance.

1. Weekly News

European Union

EU Weighs Tariffs on US Olive Oil and Other Goods Amid Ongoing Trade Dispute

The European Commission (EC) is holding a public consultation from May 8 to June 10 on potential countermeasures targeting USD 95 billion worth of United States (US) goods, including olive oil, if current European Union (EU)-US trade negotiations fail. The proposed tariffs could impact a wide range of US agricultural products, such as olive oil, nuts, and alcoholic beverages, as well as industrial goods. Olive oil is among the USD 10.5 billion in targeted US food exports.

The EU may also initiate a World Trade Organization (WTO) dispute procedure over broad US tariffs, particularly those affecting cars and auto parts. This comes as 70% of EU exports to the US are now subject to new American tariffs. While negotiations continue, the EC explores new export markets and supply diversification to mitigate potential disruptions.

Australia

Australia's Expanding Olive Oil Market Opens New Opportunities for Greek Exports

Australia's olive oil market is expanding steadily, with rising consumer demand and limited domestic production creating favorable conditions for Greek exports, according to a report by the Consulate General of Greece in Sydney. Domestic output remains modest at 20,000 to 25,000 metric tons (mt) annually, while the market, valued at USD 304.38 million (AUD 475 million) in 2023, is projected to grow by 5.2% annually through 2028.

Olive oil is now a staple of two-thirds of Australian homes, driven by health and culinary trends. Over 95% of imports come from the EU, led by Spain, Italy, and Greece. Although Greece holds a smaller share, its olive oil is well-regarded, especially among the Greek diaspora and Mediterranean cuisine consumers. Imports face no tariffs, and distribution is supported by specialty importers and ethnic retailers in major cities.

India

India's Olive Oil Market Grows Despite Tariff Challenges, Led by Spanish Exports

India's olive oil market is steadily expanding, with sales rising from USD 110.74 million (EUR 99 million) in 2018 to USD 183.45 million (EUR 164 million) in 2024, and projected to reach USD 221.48 million (EUR 198 million) by 2028, according to the Spanish Institute for Foreign Trade (ICEX). Spanish producers dominate the market, supplying 82% of imports, led by major bottlers such as Deoleo. Growth is driven by rising health awareness, urbanization, and interest in international cuisine, though high tariffs (45% basic duty) and limited rural penetration remain key challenges. Efforts to increase local awareness and adapt products to Indian cooking methods support continued demand growth, particularly in major and secondary cities.

Spain

Spanish Olive Oil Market Strengthens in 2024/25 with Strong Sales and Production Recovery

Spanish olive oil sales remain strong, with 139,400 mt sold in Mar-25, bringing total sales for the first half of the 2024/25 season to 727,700 mt, an increase of 27.1% year-on-year (YoY) and 3.4% above the four-season average. Both export sales, totaling 456,300 mt, and domestic sales, reaching 271,500 mt, have contributed to this growth, with YoY increases of 26.2% and 28.7%, respectively.

Production reached 1.41 million metric tons (mmt) by the end of Mar-25, marking a substantial recovery after two weak harvests. Imports declined slightly to 126,100 mt, a decrease of 2.6%, while end-Mar-25 stocks stood at 996,100 mt, higher than the past two seasons but below 2020/21 and 2021/22 levels.

Spain's Olive Oil Sector Rebounds with Strong Harvest and Global Recognition at 2025 NYIOOC

Spain's olive oil sector marked a significant recovery in the 2024/25 season, producing 1.41 mmt, more than double the volume of the previous two years, thanks to favorable weather conditions. This rebound in both quantity and quality enabled Spanish producers to win 93 awards at the 2025 New York International Olive Oil Competition (NYIOOC), led by Andalusia with 60 accolades.

Award-winning producers highlighted improved weather, enhanced production practices, and growing international recognition, particularly in the US market. Despite challenges such as rising input costs and labor shortages, optimism remains high for the 2025/26 season, supported by ample rainfall and healthy flowering across key olive-growing regions.

2. Weekly Pricing

Weekly Olive Oil Pricing Important Exporters (USD/kg)

Yearly Change in Olive Oil Pricing Important Exporters (W19 2024 to W19 2025)

Italy

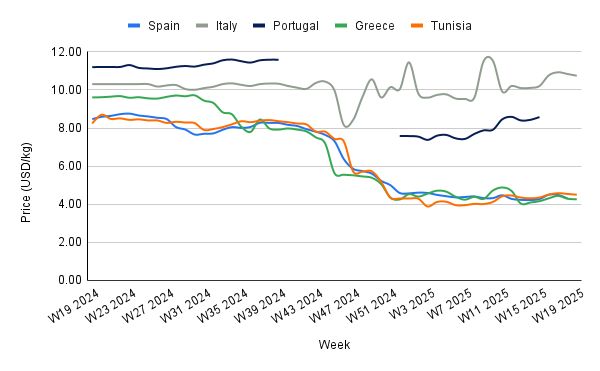

In W19, Italy's olive oil price stood at USD 10.75 per kilogram (kg), marking a decrease of 0.83% week-on-week (WoW) but an increase of 4.27% YoY. The slight weekly decline reflects temporary market adjustments, yet prices remain high due to ongoing supply-side constraints. The 2024/25 harvest fell by 32% YoY to 224,000 mt, weighed down by prolonged drought, extreme temperatures, and persistent pest and disease pressure, particularly from the olive fruit fly and Xylella fastidiosa in Southern regions. Meanwhile, international demand remains firm, keeping prices elevated despite weak output. The US announcement in Apr-25 of a 20% tariff on all EU imports, including Italian olive oil, has added further uncertainty. Although a 90-day pause in most reciprocal tariffs is in effect, the risk of escalating trade tensions may distort future price trends. If the tariffs persist, export costs could rise significantly, potentially driving Italian olive oil prices higher in non-EU markets and encouraging greater reliance on intra-EU trade to stabilize demand.

Greece

In W19, Greece's wholesale olive oil prices declined to USD 4.26/kg, falling 0.70% WoW and sharply down 55.67% YoY from USD 9.61/kg. The substantial annual decrease reflects a strong recovery in production following prior supply shortages that had pushed prices to record highs. Production for the 2024/25 season remains stable at approximately 250,000 mt, yet limited stock levels continue to constrain supply flexibility. As mid-2025 approaches, tightening availability alongside persistent demand is beginning to halt the price decline, signaling a potential rebound. Nonetheless, the Greek olive oil market remains susceptible to climatic fluctuations, which could quickly influence future price dynamics and market stability.

Tunisia

Tunisia's olive oil prices declined to USD 4.50/kg in W19, a decrease of 0.88% WoW and a 45.39% YoY drop from USD 8.24/kg. This weekly decline reflects sustained pressure from an oversupplied global market, driven by strong harvest recoveries in key producing countries. Despite the falling prices, Tunisia’s olive oil exports surged 85.3% YoY in Q1-2025, reaching 115,200 mt, largely due to bulk shipments. Extra virgin olive oil prices also plunged 43.5% YoY to USD 5,603/mt in Mar-25 after peaking at record highs earlier. With global production rising to an estimated 3.1 mmt for 2024/25, up from 2.5 mmt last season, price pressures are expected to persist throughout 2025.

3. Actionable Recommendations

Diversify Export Markets to Mitigate Transatlantic Trade Risk

In anticipation of potential EU retaliatory tariffs on US olive oil and related goods, exporters, particularly from Spain, Italy, and Greece, should proactively expand access to alternative high-growth markets such as Australia and India. These markets offer tariff-free or low-barrier entry and are experiencing rising demand driven by health trends and culinary globalization. Targeted promotional campaigns, tailored packaging for local preferences, and partnerships with ethnic retailers and specialty distributors can facilitate market entry and long-term presence.

Strengthen Position in Australia Through Origin Branding and Diaspora Engagement

Given Australia's reliance on EU olive oil imports and its growing demand, Greek and other Mediterranean exporters should invest in branding strategies that emphasize regional origin, quality, and cultural resonance. Outreach through Greek-Australian networks and Mediterranean cuisine associations. Expanding distribution via urban specialty stores and premium supermarkets will further entrench EU olive oil in a market projected to grow over 5 percent annually.

Sources: Tridge, Agro Popular, Agri.bg, Olive Oil Times, Kathimerini, Ukr AgroConsult, African Manager