In W22 in the apple landscape, some of the most relevant trends included:

- India’s Kashmir apple growers are hopeful that the proposed import restrictions on apples from Turkey will stabilize local prices, potentially increasing them by 10% to 15%.

- India’s Kashmir region benefited from timely rainfall that improved soil moisture and reduced pest pressure. This has boosted optimism for a strong apple harvest after last year’s drought.

- Mexico’s Coahuila apple production is expected to decline by 20% to 30% due to late frosts and extreme heat damaging blossoms. This situation has prompted the activation of state-funded catastrophic insurance.

- South Africa has become the leading apple exporter in the Southern Hemisphere, surpassing Chile by 16%. This achievement is supported by advanced farming techniques and close market access.

1. Weekly News

India

Kashmir Apple Growers Eye Relief as Import Restrictions Discussed

Apple growers in Kashmir are hopeful that proposed restrictions on apple imports, especially from Turkey, will help stabilize local prices, which have been undercut by the influx of cheaper foreign varieties, including those from Iran. With nearly half of the region’s population dependent on the apple trade, such curbs could raise local prices by 10% to 15%, offering vital financial relief ahead of a promising harvest season supported by favorable weather. Growers and industry advocates urge policymakers to implement supportive measures that enhance local competitiveness and ensure long-term sector sustainability.

Timely Rainfall Revives Apple Prospects in Kashmir

Recent rainfall across Kashmir has brought much-needed relief to apple-growing districts like Shopian, Pulwama, Kulgam, and Anantnag, following a dry May that raised concerns about crop health. The rains have improved soil moisture, reduced pest pressure, and limited heat-related damage, renewing optimism for a strong harvest. After last year’s severe rainfall deficit, especially the 81% shortfall in Shopian, this turnaround is significant for a region that produces over 70% of India’s apples and supports around 350 thousand families. With more showers forecasted, growers are watching conditions to ensure crop development stays on track.

Mexico

Apple Production in Mexico’s Coahuila Falls Due to Unfavorable Weather

Apple growers in Coahuila, Mexico, particularly in Arteaga, face a difficult season due to adverse weather conditions. A combination of late frosts followed by extreme heat has damaged blossoms and is expected to reduce yields by 20% to 30%. Affected areas include Huachichil and the San Antonio de las Alazanas canyon, prompting the state government to activate catastrophic insurance funded entirely by state resources. While other crops like sorghum remain unaffected, the situation highlights the increasing vulnerability of apple farming in the region to erratic weather conditions.

South Africa

South Africa Becomes Leading Southern Hemisphere Apple Exporter

South Africa has surpassed Chile as the Southern Hemisphere’s leading apple exporter, outpacing it by 2.6 million cartons, a 16% lead by W22. South Africa’s advantage stems from its close access to major markets, strict phytosanitary standards, and continued investment in advanced farming techniques, including high-density planting and the use of protective netting. These factors have supported a 30% increase in apple production over the past eight years, even as Chile faces a projected 44% drop in harvest volume by 2025. Despite climate variability and logistical constraints at Cape Town port, South Africa continues to strengthen its position as a key global apple supplier.

Ukraine

Ukraine Faces Apple Shortage as Prices Climb and Export Markets Expand

Ukraine is experiencing a sharp apple shortage, with prices rising by 14% to USD 0.80 to 1 per kilogram (UAH 32 to 40/kg). This is double the levels of the previous year, due to dwindling stocks and delayed early harvests following a prolonged spring. Only 10 to 15% of seasonal supply remains, and just 20% meets maritime export quality, leading to a shift in focus toward European markets. Gala apples were particularly affected by yield losses, driving a threefold decline in export volume this year. However, Ukraine has secured access to the Canadian market, pushing producers to meet higher phytosanitary and logistics standards, a step toward more diversified and resilient exports.

2. Weekly Pricing

Weekly Apple Pricing Important Exporters (USD/kg)

Yearly Change in Apple Pricing Important Exporters (W22 2024 to W22 2025)

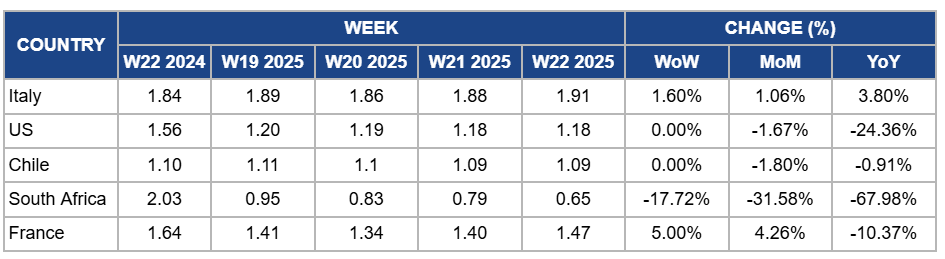

Italy

Italy's apple prices increased by 1.60% week-on-week (WoW) to USD 1.91/kg in W22, reflecting a 1.06% month-on-month (MoM) growth and a 3.80% year-on-year (YoY) rise. This price increase is driven by reduced production following spring frosts in Apr-25, which impacted yields across major apple-producing regions in Europe, including Italy. At the same time, strong export demand, particularly from non-European markets, has supported price growth, as Italian apples are favored for their quality. Despite weaker local consumption, prices have remained firm locally due to consistent consumer interest and the premium quality of specific varieties. These combined factors have tightened supply and maintained upward pressure on prices.

United States

United States (US) apple prices remained stable WoW at USD 1.18/kg in W22. This was supported by strong local supply from the 2024 harvest and consistent demand for popular varieties like Gala and Fuji. However, prices declined by 1.67% MoM and 24.36% YoY due to a decrease in total US apple production for the 2024/25 crop year, reaching approximately 259.5 million bushels. A 13% drop in foreign demand for fresh apple exports compared to their peak a decade ago also contributed to the MoM and YoY drops.

Chile

In W22, Chile's apple prices remained steady WoW at USD 1.09/kg, but registered a 1.80% MoM drop and a 0.91% YoY decrease. The MoM decline is due to increased local supply from the 2025 harvest, as production volumes have risen by 4.4% YoY, totaling 573.6 thousand tons, particularly in red varieties like Pink Lady and Fuji. This growth is driven by favorable climatic conditions and improved orchard management practices. However, the YoY price decrease reflects a normalization from the elevated prices in the previous year, which were influenced by global supply shortages. Additionally, intensified competition from other Southern Hemisphere exporters and logistical challenges have contributed to the slight annual price decline.

South Africa

South Africa's apple prices dropped by 17.72% WoW to USD 0.65/kg in W22, with a 31.58% MoM decrease and a 67.98% YoY drop. This is due to sluggish export demand, particularly from key markets such as the Middle East and Asia, combined with oversupply in the domestic market as harvest volumes peak. The high availability of lower-grade fruit, partly due to adverse weather earlier in the season, affecting quality, further pressured prices. Additionally, logistical challenges and shipping delays continued to disrupt export flows, causing more products to be redirected to the local market, intensifying downward price pressure.

France

In France, apple prices rose by 5% WoW to USD 1.47/kg in W22, with a 4.26% MoM increase. This rise is due to tightening supplies toward the end of the storage season, leading to reduced availability of high-quality apples and stronger domestic demand. The ongoing transition between stored and freshly harvested imports has also contributed to price firmness. However, the YoY drop of 10.37% is mainly due to lower export activity earlier in the season and subdued consumer demand compared to last year, when prices were elevated due to supply chain disruptions and reduced yields across Europe.

3. Actionable Recommendations

Prioritize Quality Grading and Cold Chain Investment

Apple producers should prioritize strict grading and invest in improved cold chain systems to expand access to premium export markets. Producers in Poland, Ukraine, and Turkey can implement tighter post-harvest sorting to separate maritime-quality apples early while upgrading cold storage to preserve export-grade varieties like Gala and Fuji. This helps maximize value from limited high-quality supply and enables entry into demanding markets such as Canada and Asia, where consistent quality and cold chain compliance are critical.

Adopt Climate-Resilient Orchard Practices

Apple producers should adapt orchard management to withstand increasing climate volatility. Growers in Northern Mexico, Turkey, and parts of Eastern Europe can invest in anti-frost systems such as wind machines or overhead sprinklers, and use shade nets to protect blossoms from heat stress. Shifting to more resilient apple varieties with stronger flowering windows and higher heat tolerance, like Aztec Fuji or Gala Schniga, can also help stabilize yields in unpredictable weather.

Plan Storage-to-Harvest Transitions Early

Apple producers should better align storage depletion with fresh harvest timelines to maintain consistent quality and supply. Cooperatives and packhouses can schedule gradual cold storage releases, prioritizing high-grade fruit for key markets, while planning import timing to fill short gaps. For example, Polish and Italian growers can coordinate controlled atmosphere storage exits with early harvests of Gala or Delbarestivale to avoid sudden market shortages or dips in quality.

Sources: Tridge, AgroNews, Freight News, Freshplaza, Pune Times Mirror, Vanguardia