In W25 in the avocado landscape, some of the most relevant trends included:

- Malaysia is expected to boost local avocado production as the implementation of a 5% sales and service tax on imported avocados is likely to shift demand toward locally grown varieties, particularly in Sabah.

- Guatemala is close to securing market access to the US for its Hass avocados, with a USDA audit of 28 farms and eight packing facilities still pending. This effort is part of its broader strategy to expand exports beyond Europe and Central America.

- Mexico is facing downward pressure on avocado prices due to global oversupply. This comes despite strong yields and high fruit quality in Michoacán and Jalisco, along with continued tariff-free access to the US.

- Peru has increased avocado exports despite ongoing logistical disruptions at European ports. Export volumes have already surpassed last year’s levels, and production is expected to rise by 15% in 2025, further strengthening its position as a key global supplier.

1. Weekly News

Malaysia

Malaysia Eyes Growth in Local Avocado Production as Import Tax Takes Effect

Malaysia is poised for growth in local avocado production following the implementation of a 5% sales and service tax (SST) on imported avocados starting July 1. The SST aims to support local agriculture and improve food security. With imports currently accounting for 85% of the avocado market, the new tax is expected to shift consumer demand toward locally grown varieties, particularly in Sabah, where avocado farms span around 2 thousand hectares (ha). Local avocados are priced between USD 1.70 and 2.10 per kilogram (kg) at the farm level, reaching up to USD 4.20/kg at retail. The SST exemption for local produce, along with stable pricing and expected regulatory support, will encourage more Malaysian farmers to invest in avocado cultivation and increase production to meet rising demand.

Guatemala

Guatemala Nears US Market Access for Hass Avocados

Guatemala is nearing approval for access to the United States (US) market for Hass avocados, pending an upcoming audit by the United States Department of Agriculture’s (USDA) Animal and Plant Health Inspection Service (APHIS) to inspect 28 farms and 8 packing facilities. The process requires an operational plan and a public-private cooperation agreement to ensure all production meets strict phytosanitary standards, including pest-free certification against threats such as Macrocopturus aguacate. Led by the National Avocado Association in collaboration with APHIS, the initiative represents a strategic step for Guatemala, which already exports avocados to the Netherlands, the United Kingdom (UK), Germany, France, Canada, and Central America.

Mexico

Mexico Faces Avocado Market Pressure as Oversupply Lowers Price

Mexico continues to report strong avocado yields due to favorable weather in Michoacán, Jalisco, and the State of Mexico, improving fruit size, quality, and shelf life, which benefits retailers. While the crop avoided damage from Hurricane Erick, Mexico now faces pricing pressure due to a global oversupply, with large volumes arriving from Peru and Colombia. Despite enjoying tariff-free access to the US, its primary export market, the influx of size 48 avocados has lowered prices. Mexico retains a competitive advantage through consistent quality and coordinated exports, though overlapping harvests with other producing countries may prolong challenging market conditions.

Nicaragua

Avocado Production Supports Growth in Nicaragua’s Agriculture

Nicaragua is emerging as a growing player in avocado production, supported by favorable climate and soil conditions that enhance flowering and fruit development. Avocados are becoming increasingly significant to the country’s agriculture, benefiting more than 2.1 thousand small and medium-sized farming families who harvested around 3.2 million avocados between Jan-25 and May-25. The peak season runs from April to June, with supply serving local and export markets, underscoring Nicaragua’s expanding role as a dependable avocado supplier in the region.

Peru

Peru’s Avocado Exports Grow Despite Logistical Disruptions

Peru’s avocado season has reached its midpoint, with export volumes surpassing last year's due to expanded cultivation and strong demand, especially from the US and Europe. However, congestion at European ports such as Rotterdam and Algeciras has delayed shipments, causing temporary supply gluts and price drops. Despite these disruptions, demand remains strong in Germany, Spain, and Eastern Europe, where avocado consumption continues to rise. With production expected to increase by 15% in 2025, Peru is reinforcing its position as a major global exporter of avocados.

2. Weekly Pricing

Weekly Avocado Pricing Important Exporters (USD/kg)

Yearly Change in Avocado Pricing Important Exporters (W25 2024 to W25 2025)

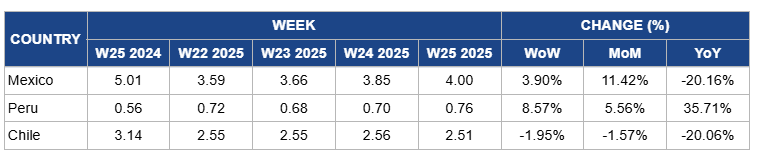

Mexico

In W25, avocado prices in Mexico increased by 3.90% week-on-week (WoW) to USD 4/kg, reflecting an 11.42% month-on-month (MoM) increase due to tighter supplies linked to the seasonal decline in harvesting volumes and increased local demand. However, year-on-year (YoY) prices dropped by 20.16% due to significantly higher production levels earlier in the year, which had pushed prices down in 2024 compared to the same period in 2023, when supply was more limited and export demand was stronger.

Peru

In W25, Peruvian avocado prices rose by 8.57% WoW to USD 0.76/kg. This marks a 5.56% MoM gain and a sharp 35.71% YoY increase. The price surge was driven by tightening supplies, following earlier season production declines in key coastal regions, where adverse weather reduced yields by up to 30%. Strong export demand also played a role, especially from Europe, the US, and Asia, which absorbed most of the available fruit as Peru ramped up shipments to fill gaps left by Mexico’s off-season. Additionally, logistics delays and higher freight costs constrained availability further, allowing traders to maintain elevated price levels.

Chile

Chile's avocado price dropped slightly by 1.95% WoW to USD 2.51/kg in W25, reflecting a 1.57% MoM decrease and a 20.06% YoY decline. This price softening stems from a surge in domestic supply. Chile is gearing up for its largest crop in over a decade, expected to exceed 235 thousand metric tons (mt). This increase is driven by favorable weather and improved farming practices, leading to an extended season into Jun-25. With over 45% earmarked for export and significant volumes also entering the local market (supported by local consumption of around 8 kg per person annually), the resulting oversupply has driven prices lower compared to last year, when output was more constrained.

3. Actionable Recommendations

Segment Exports by Fruit Size and Market

Avocado producers should sort and segment their exports by fruit size to better match demand across multiple markets and reduce price pressure from size 48 oversupply. For instance, size 48 avocados can be prioritized for US retailers running promotions, while smaller sizes like 60s and 70s can be directed to markets such as Eastern Europe or Southeast Asia, where smaller calibers are preferred. By working closely with packers and distributors, producers can tailor shipments by size and destination, improving margins and reducing the surplus of any single size in key markets.

Strengthen Logistics and Distribution Diversification

Avocado producers should proactively diversify their export routes and strengthen partnerships with logistics providers to minimize the impact of port congestion in Europe. Instead of relying heavily on ports like Rotterdam and Algeciras, producers can redirect partial volumes to less congested entry points such as Antwerp, Marseille, or Hamburg. They should also explore staggered shipment schedules and collaborate with cold chain service providers to maintain fruit quality during delays. These steps will help stabilize prices, avoid oversupply in single markets, and ensure timely access to high-demand regions like Germany and Eastern Europe.

Sources: Tridge, APEAMEX, el19digital, FMT, Freshplaza, Lahora