.jpg)

1. Weekly News

Brazil

Brazil's Sugar Production Drops 24.3% YoY in Second Half of Oct-24, with Reduced Cane Processing and Lower Extraction Rates

In the second half of Oct-24, sugar production in Central and South Brazil dropped by 24.3% year-on-year (YoY), totaling 1.78 million metric tons (mmt), due to reduced sugarcane processing and lower sugar extraction rates. A total of 27 factories completed their sugarcane processing for the 2024/25 marketing year (MY), bringing the total to 38 plants for the season, compared to 26 last year. The volume of sugarcane processed during this period was 27.17 mmt, a 21.6% YoY decrease from 2023, with 46.12% of the cane used for sugar production, down from 48.85% in the previous year. However, total sugarcane processed from April 1 to November 1 reached 566.03 mmt, slightly up from 561.09 mmt last year, with a marginal increase of 0.27% in sugar production to 37.38 mmt.

Brazil's Sugar Shipments Drop in W47, With Decline in Exports and Revenue in Nov-24

Sugar shipments at Brazilian ports decreased significantly in W47, with 52 vessels scheduled to load 1.901 mmt, down from 62 vessels and 2.279 mmt the previous week. The Port of Santos leads with 1.386 mmt, followed by Paranaguá, with 301,497 metric tons (mt), and other smaller ports. The cargo primarily includes Very High Polarization sugar (VHP), with 1.795 mmt alongside smaller quantities of TBC, Cristal B150, VHP in bags, and Refined A-45.

In Nov-24, Brazil's average daily sugar export volume rose slightly to 183,341 mt, but daily revenue fell 9.3% YoY to USD 88.024 million due to a 9.8% drop in the average price/mt, currently at USD 480.10/mt. Oct-24 exports totaled 1.833 mmt, generating USD 880.241 million in revenue.

China

China's Sugar Imports Decline in Sep-24, But Cumulative Imports Show Strong Growth

In Sep-24, China's sugar imports totaled 403,700 mt, valued at USD 210 million, marking a YoY decline of 25.09% in volume and 35.52% in value. However, from Jan-24 to Sep-24, cumulative sugar imports reached 2.89 mmt, valued at USD 1.61 billion, reflecting increases of 36.94% in volume and 39.58% in value compared to last year.

Brazil was the leading source of China's sugar imports, accounting for USD 1.36 billion in imports, a 58.27% increase from the previous year. Despite this, Sep-24 imports from Brazil fell 42.24% YoY, totaling USD 174 million. The top ten import countries/regions were Brazil, South Korea, El Salvador, Nicaragua, Thailand, South Africa, Malaysia, India, Indonesia, and Mauritius, representing 99.61% of China's total sugar imports.

Kazakhstan

Kazakhstan's Sugar Output Hits Record Low

Kazakhstan's sugar production from Jan-24 to Oct-24 totaled 168,100 mt, the lowest since 2020. Production declined by 17.6% in 2024, following a 31.1% drop in 2023. The Zhambyl region led output with 45.7% of the total, followed by Zhetysu (40%) and Almaty (13.2%). Investments are urgently needed to modernize sugar factories, where equipment wear averages 33%.

Imports covered 72.4% of demand from Jan-24 to Aug-24, up from 57.7% YoY. Domestic sugar sales fell 17.7% YoY to 292,900 mt, the lowest since 2019. Retail prices for granulated and refined sugar declined slightly in Oct-24, averaging USD 0.81 per kilogram (KZT 403/kg), with regional variations from USD 0.72/kg (KZT 360/kg) in Aktobe to USD 0.88/kg (KZT 436/kg) in Taldykorgan.

Russia

Russia's 2024/25 Sugar Production Forecast to Drop 11% YoY, Despite Increased Sugar Beet Planting

Russia’s sugar production for the 2024/25 agricultural year is forecasted to reach 6.1 mmt, an 11% YoY decrease, according to the Institute for Agricultural Market Studies (IKAR). Despite a 10% YoY increase in sugar beet planting to 1.7 million hectares (ha), harvest volumes by Nov-24 were down by 8.7%, totaling 42.7 mmt. The most significant declines were observed in the South of Russia and the Central Black Earth Region. IKAR predicts a 15% YoY reduction in the total sugar beet harvest to 45 mmt. The Ministry of Agriculture (Minselkhoz) offers slightly more optimistic figures, forecasting a 44 mmt beet harvest and sugar production of 6.3 to 6.4 mmt. As of Sep-24, Russia had produced 2.9 mmt of sugar, a 13.4% YoY increase from 2023. However, Minselkhoz cites using Russian-bred seeds and yield decreases as risks that could further impact sugar production.

Mozambique

Mozambique's Sugar Industry Set for 10% Production Increase in 2024/25 Season

Mozambique's sugar industry is set to increase production by 10% in the 2024/25 agricultural season, recovering from recent setbacks, including flooding and the temporary closure of the Maragra sugar mill. Production is projected to rise from 1.6 mmt to 1.9 mmt, meeting domestic demand and boosting exports. Supporting 18,000 jobs, the sector faced challenges after the 2022 cyclone reduced sugar cane output from 2.7 mmt to 1.6 mmt.

Türkiye

Türkiye's Kayseri District Completes Sugar Beet Harvest

In Türkiye, the sugar beet harvest in the Kayseri district, spanning 900 acres, has been completed. The harvest yielded 6,500 mt of produce, which was transported for processing. Farmers expressed satisfaction with this season's productivity, highlighting favorable regional outcomes.

Ukraine

Ukraine's Sugar Prices Rise Following Export Recovery, EU Market Set to Boost 2025 Outlook

Over the past week, sugar prices in Ukraine have risen by USD 0.024 to 0.036/kg (UAH 1 to 1.5/kg), reaching USD 0.56 to 0.59 (UAH 23 to 24.5/kg), driven by recovering exports and stable domestic demand. Key export markets include Türkiye and African countries, while indirect supply routes to Europe have also contributed. Analysts expect prices to rise further in early 2025 with direct sugar exports to the European Union (EU) resumption, potentially approaching the previous season's high of USD 700.05 to 772.46/mt (UAH 29,000 to 32,000/mt).

2. Weekly Pricing

Weekly Sugar Pricing Important Producers (USD/kg)

Yearly Change in Sugar Pricing Important Producers (W47 2023 to W47 2024)

.png)

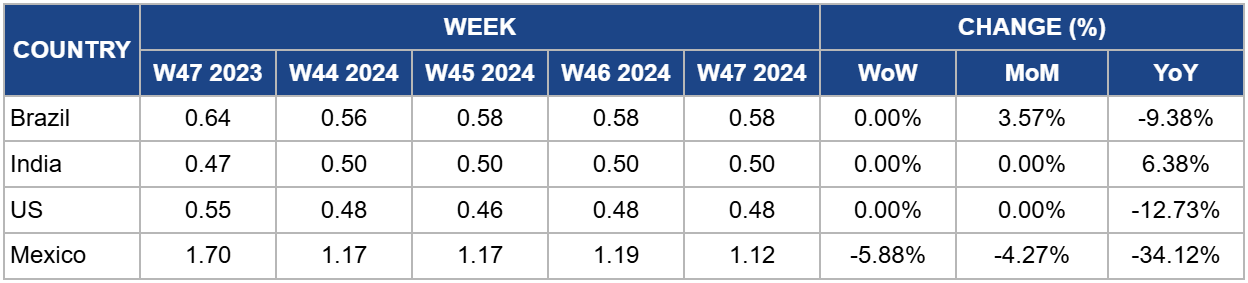

Brazil

In W47, Brazil's domestic sugar prices remained stable at USD 0.58/kg, reflecting a 9.38% YoY decrease from USD 0.64/kg. The stability comes amid challenges in Brazil's sugar production, including the impact of heavy rainfall that has affected the harvest. The early closure of sugar mills due to adverse weather conditions has led to expectations of reduced sugar supply, which boosted futures prices on international exchanges. As Brazil faces ongoing weather-related disruptions, the sugar market remains under pressure, and prices could experience further volatility in the coming weeks.

India

India's sugar prices remained stable at USD 0.50/kg in W47, reflecting a 6.38% YoY increase. Despite this, favorable monsoon rains, exceeding the long-term average by 7.6%, will likely boost India's sugar crop. While this may support domestic supply, the increased production potential could negatively impact prices. India’s recent policy changes support the prices. The Food Ministry lifted restrictions on sugar mills producing ethanol for the 2024/25 season, which may extend the country's sugar export restrictions. India had imposed export curbs in Oct-23 to ensure domestic sugar supplies, limiting exports to 6.1 mmt in the 2022/23 season, down from a record 11.1 mmt in the prior season. The Indian Sugar and Bio-energy Manufacturers Association (ISM) projects a modest 2 mmt of sugar exports for the 2024/25 season and has called for lifting export restrictions. While India faces an optimistic production outlook, export restrictions and domestic strong reserves will likely support stable sugar prices in the near term.

United States

In W47, the United States (US) sugar prices remained stable at USD 0.48/kg, although they marked a 12.73% YoY decrease from USD 0.55/kg. The price stability comes amid ongoing legal challenges in Florida concerning the Comprehensive Everglades Restoration Plan (CERP), set to restore portions of the Everglades, Lake Okeechobee, the Caloosahatchee River, and Florida Bay. The Florida sugar industry, represented by US Sugar, is contesting a state construction project for a stormwater treatment area. It argues that it violates a 2000 federal law that mandates maintaining water reserves for agricultural use during Everglades restoration efforts. This legal battle could potentially impact water management policies in the region, affecting the sugar industry's operations.

Mexico

In W47, Mexico's sugar prices dropped to USD 1.12/kg, reflecting a 5.88% week-on-week (WoW) decrease and a 34.12% YoY decline from USD 1.70/kg. This price trend coincides with strengthened international collaboration in the sugar sector. Cuban and Mexican sugarcane research institutions formally agreed to exchange genetic and biological material to enhance sugarcane cultivation. The initiative aims to improve breeding practices, combat pests and diseases, and advance scientific research. These efforts align with broader discussions during the VIII Meeting of Sugar Technicians' Associations from both countries, where experts highlighted the need for innovative and efficient production methods to address global challenges like climate change and supply chain disruptions. These efforts may improve yields and lower costs in the long term, stabilizing prices. However, short-term volatility from weather and market factors remains likely.

3. Actionable Recommendations

Strengthen Supplier Diversification

To address Brazil's declining sugar production and mitigate supply chain risks, businesses should diversify sourcing strategies by increasing procurement from emerging sugar-producing regions like Mozambique, which anticipates a 10% production increase in 2024/25, and stable suppliers like Thailand and India. Building relationships with alternative suppliers can enhance resilience against weather-related disruptions and export limitations in key markets such as Brazil and India. Long-term agreements and exploring options like refined and value-added sugars can ensure consistent quality and supply stability.

Enhance Supply Chain Efficiency

Invest in port infrastructure and logistics improvements to efficiently manage reduced sugar shipment volumes, particularly in Brazil, where port congestion remains a bottleneck. Prioritize partnerships with freight services and develop contingency plans for high-demand periods to expedite shipments. Stakeholders should also consider advanced tracking technologies to optimize loading schedules at major ports like Santos and Paranaguá, ensuring smoother supply chain operations amidst fluctuating sugar output.

Promote Value-Added Product Development

Amid falling sugar prices in major markets like the US and Mexico, stakeholders should invest in developing and marketing value-added sugar products such as organic, fair-trade, or specialty sugars to capture premium pricing. This strategy can target niche markets where demand is less sensitive to price fluctuations, offsetting revenue losses from raw sugar price declines. Additionally, producers in regions like Kazakhstan should modernize facilities to improve efficiency and quality, aligning with global standards to remain competitive.

Sources: Sondaikika, Grain Trade, Agrarian Sector, Moz-Agri, Portal Do Agronegocio, Foodmate, Ukragroconsult, NASDAQ, E&E News, Radio Bayamo