W8 2025: Avocado Weekly Update

In W8 in the avocado landscape, some of the most relevant trends included:

- Weather-related disruptions, including Storm Dorothea in Spain and reduced rainfall in Kenya, have affected production volumes, though some regions expect recovery in 2025.

- Mexico leverages major events like the Super Bowl to boost demand, while California plans promotional campaigns to emphasize sustainability and local production.

- Colombia faces logistical and labor challenges that could impact long-distance exports, particularly to China, while Kenya’s government is investing in infrastructure and farmer training to support growth.

1. Weekly News

Australia

Domestic Demand for Australian Avocados Remains Strong and Export Markets Continue to Grow

Australia ensures a year-round avocado supply through its diverse growing regions, with production currently shifting from Western Australia to North Queensland. The season starts with the Shepard variety, followed by Hass in April. While the recent wet weather briefly disrupted transport in North Queensland, conditions have stabilized. After a period of oversupply, production is lighter this year, though volumes are expected to rise from Jul-25 to Dec-25, particularly in Western Australia. Local demand remains strong, and exports continue to perform well in key markets like Hong Kong, Singapore, and Malaysia, with growing shipments to Thailand, Japan, and India. Meanwhile, efforts are currently in progress to secure market access to China.

Colombia

Colombia Strengthens Its Position in the Global Avocado Market

Colombia’s Hass avocado industry is expanding rapidly, with 2024 exports exceeding USD 300 million, a 54.3% year-on-year (YoY) increase from 2023, making avocados the country’s second most exported fruit after bananas. This growth has significantly boosted key producing regions, with Valle del Cauca nearly tripling its exports to over USD 50 million, while Antioquia and Risaralda recorded increases of 42.1% and 37.9%, respectively. However, rising production brings challenges, including labor shortages, inadequate road infrastructure, and quality control issues for long-distance exports, particularly to China. Despite these challenges, Colombia continues to strengthen its position in high-demand international markets.

Kenya

Kenya's Avocado Production Expected to Rebound in 2025

Kenya’s avocado production fell by 11.2% YoY in 2024 to 562 thousand metric tons (mt) due to reduced rainfall but is expected to recover by 4% YoY in 2025, reaching 585 thousand mt. This rebound is driven by expanded cultivation, improved yields through quality control, and government support, including high-quality seedlings, farmer training, and subsidized inputs. Despite lower production, export value rose by 11% in 2024 to USD 159 million, fueled by strong global demand. In 2025, exports are projected to grow by 5% to 135 thousand mt, benefiting from expanded market access to Iraq, South Korea, and India. Kenya remains Africa’s top avocado producer and the second-largest exporter by value after South Africa. Smallholder farmers play a vital role in the industry.

Mexico

Mexican Avocados Take Center Stage at the Super Bowl

Mexico’s avocado industry capitalizes on the Super Bowl to boost its presence in the United States (US) market. Since early Jan-25, it has exported 100 thousand tons of Hass avocados, with 35 thousand tons for consumption as guacamole on game day. For the fourth consecutive year, Avocados From Mexico is supporting a Super Bowl commercial to enhance brand visibility. Michoacán remains the leading producer, with Jalisco and the State of Mexico also contributing significantly.

Mexico Leads US Avocado Market Despite Supply Decline

Mexico retained its 85% share of the US avocado market despite a sharp 40% drop in shipments in W6, while lower supplies from Colombia and California contributed to record-high prices. In China, Peru remained the leading avocado supplier, accounting for 93% of shipments, though prices slightly declined. Meanwhile, shifting market dynamics in Europe saw Israel increasing its avocado exports by 37%, while Morocco's share plummeted by 62%.

Spain

Storm Dorothea Cuts Avocado Production in the Canary Islands

The Canary Islands avocado season faced challenges on December 15, 2024, when Storm Dorothea’s 140 kilometers per hour winds caused a 48% production loss, particularly in the Western Islands, the region’s main growing area. This sharp decline is expected to shorten the season but could drive higher prices. Despite strong demand from mainland Spain and Europe, exports will be more limited this year. Meanwhile, the region is nearing approval for a Protected Geographical Indication (PGI) for "Aguacate de Canarias," which would certify its quality.

United States

California Expects Strong 2025 Avocado Harvest

The 2025 California avocado harvest is expected to reach 375 million pounds (lbs), the highest volume since 2020, driven by increased tree planting and improved per-acre yields. While the recent strong winds posed challenges, growers remain optimistic about the season’s potential. Peak availability is anticipated from spring through summer, supported by a promotional campaign emphasizing the locally grown and sustainably farmed qualities of California avocados.

2. Weekly Pricing

Weekly Avocado Pricing Important Exporters (USD/kg)

* All countries are looking at the pricing of Hass avocado

Yearly Change in Avocado Pricing Important Exporters (W8 2024 to W8 2025)

* All countries are looking at the pricing of Hass avocado

* Blank spaces on the graph signify data unavailability stemming from factors like missing data, supply unavailability, or seasonality

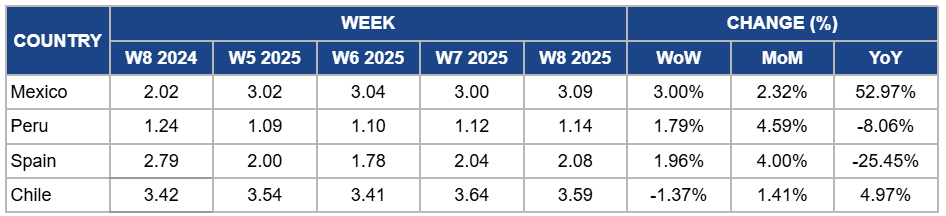

Mexico

In W8, avocado prices in Mexico increased by 3% week-on-week (WoW) to USD 3.09 per kilogram (kg), with a 2.32% month-on-month (MoM) increase and a 52.97% YoY surge due to heightened Super Bowl demand driving a spike in US imports. The export of 100 thousand tons of Hass avocados since early Jan-25, with 35 thousand tons consumed on game day, significantly reduced local availability, pushing prices higher. Additionally, Mexico’s dominant 85% market share in the US, despite a 40% drop in shipments, created supply constraints that further fueled price increases. In contrast, shifting global market dynamics, including rising exports from Israel to Europe and a decline in Morocco’s share, had a limited impact on Mexico’s pricing trends.

Peru

Peru's avocado prices rose by 1.79% WoW to USD 1.14/kg in W8, marking a 4.59% MoM increase due to strong demand from European markets, where lower supplies from Morocco and Spain created opportunities for Peruvian exports. Additionally, higher export values were supported by strategic market positioning and a gradual tightening of supply as growers prepared for improved yields in 2025. However, YoY avocado prices dropped by 8.06% due to increased competition from Mexico and Chile, which maintained strong shipments to key markets, preventing a sharper price recovery. Sufficient carryover supplies from the previous season also helped stabilize supply levels, limiting the impact of Peru's lower 2024 production on overall price trends.

Spain

In Spain, avocado prices rose by 1.96% WoW to USD 2.08/kg in W8, marking a 4% increase due to reduced supply following significant production losses in the Canary Islands caused by Storm Dorothea. The reduced harvest, particularly in the Western Islands, has led to limited availability, supporting price increases despite steady demand from mainland Spain and European markets. Additionally, anticipation of the PGI approval for "Aguacate de Canarias" has further reinforced the fruit’s premium positioning. However, avocado prices dropped significantly by 25.45% YoY due to the overall higher availability of imported avocados from Latin America, which have increased competition and exerted downward pressure on prices.

Chile

Avocado prices in Chile declined slightly by 1.37% WoW to USD 3.59/kg in W8 due to a marginal increase in available supply as the final harvest volumes entered the market, easing immediate price pressure. However, there is a 1.41% MoM increase and a 4.97% YoY rise in avocado prices due to reduced supply as the harvest season winds down, coupled with strong domestic and export demand. Additionally, reduced competition from alternative suppliers, particularly Peru, has contributed to firmer prices compared to the previous year, when higher production volumes had driven prices lower.

3. Actionable Recommendations

Strengthen Market Position with Quality and Supply Management

Kenyan avocado exporters should enhance post-harvest handling and cold chain logistics to maintain fruit quality and meet premium market standards. Smallholder farmers can adopt pruning and irrigation techniques to improve yields and mitigate climate-related risks. Exporters should diversify distribution channels by targeting high-demand markets like India and South Korea while leveraging value-added products such as avocado oil to maximize returns. Strengthening partnerships with international buyers through consistent supply and quality assurance will help sustain export growth.

Optimize Supply Strategies to Maintain Market Share

Mexican avocado exporters should coordinate shipments more efficiently to prevent sharp supply fluctuations that drive price volatility. Exporters can explore staggered harvesting and improved cold storage to extend availability. Peruvian suppliers should focus on maintaining competitive pricing in China while enhancing branding to reinforce market dominance. In Europe, Israeli exporters can capitalize on their growing presence by securing long-term contracts, while Moroccan growers should reassess logistics and pricing strategies to regain lost market share.

Sources: Tridge, Avocados Australia, Digitallpost, Freshfruitportal, Freshplaza, Msn, USDA