In W12 in the maize landscape, some of the most relevant trends included:

- As of March 16, Brazil's second corn crop planting reached 89.6%, progressing steadily but slightly lagging behind the five-year average of 90.4%.

- Mato Grosso’s harvest is concluding, while rainfall in Paraná improved conditions despite soil moisture concerns in the west.

- China’s corn imports for 2024/25 are projected at 9 mmt, significantly down from 2023/24’s imports of 13 mmt due to weak demand, economic slowdown, and tariffs on US corn. Meanwhile, US corn exports to the EU surged 87-fold to 2.7 mmt, benefiting from reduced Ukrainian supply and competitive pricing.

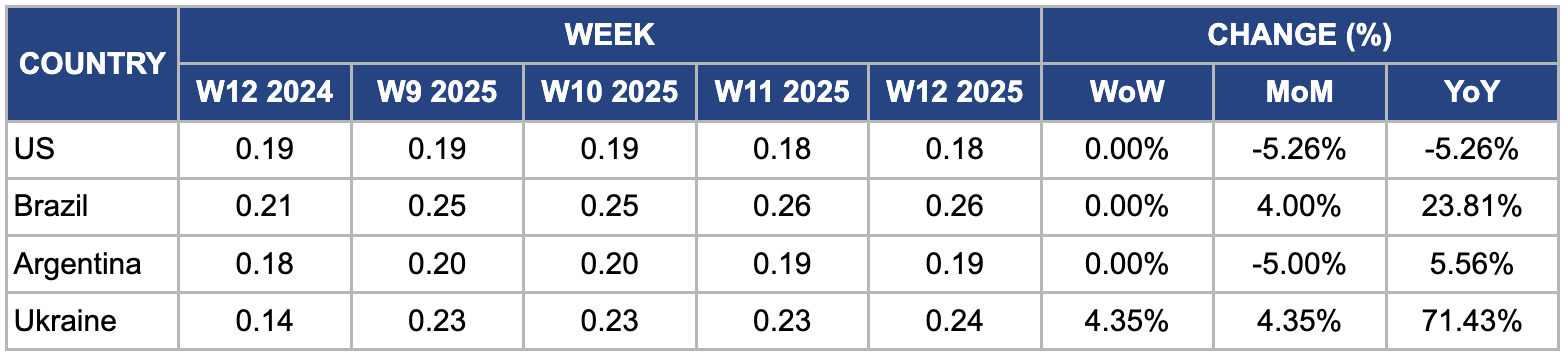

- In W12, US maize prices remained stable WoW but fell MoM due to increased supply. Brazil’s prices rose MoM and YoY, supported by strong export demand and logistical delays. Due to supply shortages, Ukrainian maize prices climbed MoM, while Argentine prices declined MoM with improved harvest conditions.

1. Weekly News

Brazil

Brazil’s Second Corn Crop Planting Reached 89.6% in W11

As of March 16, 2025, Brazil's second corn crop planting reached 89.6%, up from 83.1% in W9, according to the National Supply Company (CONAB). Despite this progress, planting lags behind the five-year average of 90.4%. Among the most advanced states are Mato Grosso with 98.8%, Goiás with 94.8%, Maranhão with 88%, and Tocantins with 85.6%. Meanwhile, Minas Gerais and São Paulo are behind, with 70.4% and 46%, respectively. With favorable conditions, Mato Grosso is nearing completion. In Paraná, recent rainfall has improved planting though low soil moisture remains a concern in the western region.

China

China’s Corn Imports Slow to Lowest in Seven Seasons, Forecast Cut to 9 MMT

China experienced its slowest pace of corn imports in seven seasons, importing only 180 thousand metric tons (mt) in Jan-25 and Feb-25, bringing the total for the 2024/25 marketing year (MY) to 1.07 million metric tons (mmt). This slowdown is the most significant since the 2017/18 season when imports totaled just 1.03 mmt during the same period. The Chinese government now forecasts 9 mmt of corn imports for the entire year, a sharp reduction from the previous estimate of 13 mmt. A sluggish economy reduced agricultural consumption, and tariffs on United States (US) corn contributed to the weaker demand. Furthermore, a downturn in the livestock sector has driven corn futures lower, prompting the state stockpiler to step in and intervene in the market.

Türkiye

Türkiye Implements 1 MMT Corn Import Quota with 5% Duty, Tightens Shipment Rules

Türkiye has introduced an additional 1 mmt corn import quota with a reduced 5% duty, valid until June 30, 2025. However, new regulations restrict shipments to 8 thousand mt per transaction, requiring a seven-day waiting period before the next application. This measure aims to regulate import flows. Ahead of the quota, importers stockpiled corn to capitalize on lower tariffs, leading to nearly full storage facilities and unusually high demand. As the quota takes effect, traders are expected to compete for better prices to offload their accumulated stocks.

Ukraine

Ukraine's 2024/25 Corn Harvest Projected at 30 MMT with Increased Planted Area

Ukraine is projected to harvest 30 mmt of corn in the 2024/25 season, driven by an increase in planted area. Analysts from the Ukrainian Agricultural Commission highlight that corn remains the most profitable spring crop, outperforming sunflower and soybeans in terms of returns.

United States

US Corn Exports to EU Surge 87-Fold, Reaching 2.7 MMT in MY 2024/25

US corn exports to the European Union (EU) surged to 2.7 mmt as of March 6 in MY 2024/25, marking an 87-fold increase from the same period in 2023/24, when only 30,981 mt were shipped. This spike is driven by poor Ukrainian production, making US corn a competitive alternative, while quality advantages and favorable exchange rates have strengthened its position against Brazilian corn. The EU now accounts for 9% of US corn exports, a significant jump from its decade-long share of under 1%, but tariff uncertainties could pose challenges. In pricing, Free-On-Board (FOB) Gulf corn stood at USD 210.73/mt on March 13, down 0.6% since January 2, while FOB Santos corn rose 6.6% to USD 212/mt, slightly above US prices. Despite strong demand, future exports will hinge on tariff developments and competition from Ukraine and Brazil.

2. Weekly Pricing

Weekly Maize Pricing Important Exporters (USD/kg)

Yearly Change in Maize Pricing Important Exporters (W12 2024 to W12 2025)

United States

In W12, US wholesale maize prices remained unchanged week-on-week at USD 0.18 per kilogram (kg) but decreased 5.26% month-on-month (MoM) and 5.26% year-on-year (YoY). This decline is due to improved weather conditions that accelerated the maize harvest, leading to increased supply. Moreover, the United States Department of Agriculture's (USDA) Mar-25 World Agricultural Supply and Demand Estimates (WASDE) report indicated higher carryover stocks, further pressuring prices downward. The USDA also projects that US corn yields will reach 181 bushels per acre in 2025, up from the previous year’s record of 179.3 bushels per acre.

Brazil

In W12, Brazil's wholesale maize prices remained unchanged WoW. However, price increased 4% MoM and 23.81% YoY to USD 0.26/kg, driven by strong export demand, particularly from China, which accounted for over 40% of Brazil’s total maize shipments in Feb-25, when exports reached 1.92 mmt, a 26% increase YoY. Logistical constraints, including port congestion at Santos and Paranaguá, due to heavy rainfall affected transportation in the Midwest and South, delaying shipments. Furthermore, concerns over dry conditions in key producing states like Mato Grosso and Paraná, where below-average rainfall threatens second-crop (Safrinha) yields responsible for about 75% of total maize production.

Argentina

In W12, Argentine maize prices remained unchanged WoW but fell 5% MoM to USD 0.19/kg, as improved supply conditions from ongoing harvests increased market availability. Favorable weather in Buenos Aires, Córdoba, and Santa Fe likely boosted yields, adding downward pressure on prices. Meanwhile, currency fluctuations and macroeconomic instability influenced price movements, with the Argentine peso’s depreciation enhancing export competitiveness, increasing shipments, and bolstering domestic supply. However, inflation and financial instability raised production costs and impacted farmer selling decisions, contributing to overall price volatility.

Ukraine

In W12, Ukraine's wholesale maize prices rose 4.35% WoW and MoM to USD 0.24/kg, driven by severe supply constraints from reduced domestic production. In 2025, prolonged drought conditions in key maize-growing regions and unseasonably cold temperatures during spring hampered yields, leading to an estimated production decline of 24 mmt. Moreover, ongoing conflict-related disruptions, including damage to infrastructure and logistical bottlenecks at export corridors such as the Black Sea, restricted the movement of maize to international markets. Despite strong global demand, particularly from the EU and China, these supply-side limitations tightened availability, pushing prices higher.

3. Actionable Recommendations

Capitalize on Favorable US Corn Prices With Forward Contracts

Importers and buyers should take advantage of the relatively lower FOB Gulf corn prices, which currently stand at USD 210.73/mt, compared to Brazilian corn at USD 212/mt. Securing forward contracts at these rates can provide cost stability and hedge against potential price fluctuations. With the EU increasing its US corn imports due to lower Ukrainian production, demand is expected to remain strong. Locking in contracts now ensures a steady supply at competitive prices, mitigating future risks from tariff uncertainties and increased competition from Ukraine and Brazil.

Optimize Brazil’s Logistics to Prevent Export Delays

Brazilian maize exporters should address logistical challenges, particularly port congestion at Santos and Paranaguá, which has led to shipment delays. Diversifying export routes by utilizing alternative ports or enhancing rail and inland transportation efficiency can help reduce bottlenecks. Heavy rainfall in the Midwest and South has already impacted transportation, limiting domestic supply availability. By improving logistics, Brazil can maintain strong export momentum, especially toward China, which accounted for over 40% of its total maize shipments in Feb-25. This would help ensure timely deliveries and sustain Brazil’s competitive edge in the global maize market.

Secure Alternative Supply Sources Amid Ukraine’s Supply Constraints

Given Ukraine’s projected maize production decline in 2025, importers should proactively diversify their supply sources to minimize risks from reduced availability. Increased procurement from Argentina and the US can help stabilize supply chains, mainly as Argentina benefits from improved harvest conditions and competitive pricing. Meanwhile, Ukraine faces ongoing supply constraints due to adverse weather and conflict-related disruptions. Securing alternative suppliers ensures consistent supply, mitigates price volatility, and prevents potential shortages in key import-dependent markets.

Sources: Tridge, NoticiasAgricolas, Sinor, UkrAgroConsult