W14 2025: Soybean Oil Weekly Update

In W14 in the soybean oil landscape, some of the most relevant trends included:

- Bangladesh is considering a soybean oil price hike due to the expiration of the import duty waiver. Discussions with edible oil refinery owners and the Ministry of Commerce are ongoing, with a decision expected by W15. BTC recommends extending the waiver until June 30.

- China’s soybean oil demand is projected to rise in 2025/26, driven by increased soybean imports and reduced availability of alternative vegetable oils. However, despite growing demand, high production costs and uncompetitive domestic pricing are constraining the expansion of local soybean oil output.

- India's soybean oil market is pressured by domestic soybean prices below the MSP and weak demand, despite higher prices for imported oil.

- Argentina’s soybean oil prices have risen due to tight supply conditions, driven by farmers withholding sales amidst currency and tax uncertainties.

1. Weekly News

Bangladesh

Bangladesh Delays Decision on Soybean Oil Price Hike as Duty Waiver Remains Uncertain

In Bangladesh, there is no decision yet about the proposed USD 0.15 per liter (BDT 18/L) increase in soybean oil prices. A meeting held with edible oil refinery owners and the Ministry of Commerce on April 8 concluded without consensus, with another discussion expected on W15. The proposed price hike, submitted by the Bangladesh Vegetable Oil Refiners and Vanaspati Manufacturers Association (BVORVMA), is linked to the expiration of the existing import duty waiver. Refinery owners argue that without an extension of the waiver, rising international prices will lead to financial losses. The Bangladesh Trade and Tariff Commission (BTC) has recommended extending the waiver until June 30, but the National Board of Revenue (NBR) has yet to respond.

China

China's Soybean Oil Demand to Rise in 2025/26 as Higher Imports and Crushing Offset Tight Edible Oil Supply

China's soybean oil demand is expected to rise in 2025/26 due to higher soybean imports and increased crushing activity amid elevated edible oil prices. According to the United States Department of Agriculture (USDA), domestic soybean consumption is projected to reach 124.4 million metric tons (mmt), with crushing volumes increasing to 101 mmt, up 2% from 2024/25. The shift in consumer preferences from pork to poultry and aquaculture has tempered growth in soybean meal demand. However, the reduced availability of alternative oils like sunflowerseed, rapeseed, and palm oil—driven by weather and biofuel policies—is increasing reliance on soybean oil. Imports are forecast to rise to 106 mmt, while domestic production is expected to slightly decline. Despite policy efforts to boost local output, high production costs and uncompetitive pricing continue to limit expansion in China’s soybean acreage.

India

India's Soybean Oil Sector Struggles Amid Global Surplus and Weak Domestic Demand

Despite government support, India's soybean oil sector is under pressure as domestic soybean prices remain below the Minimum Support Price (MSP). Since Oct-23, procurement prices in major producing states—Madhya Pradesh, Maharashtra, and Rajasthan—have consistently fallen short of MSP levels, even as soybean oil imports from Brazil, Argentina, and the United States (US) continue to rise. Notably, imported soybean oil is USD 0.18 to 0.24 per liter (INR 16 to 21/L) more expensive than domestically produced oil, yet domestic soybeans face weak demand.

The core issue lies in a global surplus of soybean meal, driven by record harvests and increased processing in the US and Brazil. Additionally, the growing use of Distiller's Dried Grains with Solubles (DDGS), a lower-cost feed alternative promoted through bioethanol programs, has further reduced demand. To prevent long-term harm to producers, experts call for a strategic shift focused on expanding markets for soybean meal, improving yields, and aligning support policies with evolving demand dynamics.

2. Weekly Pricing

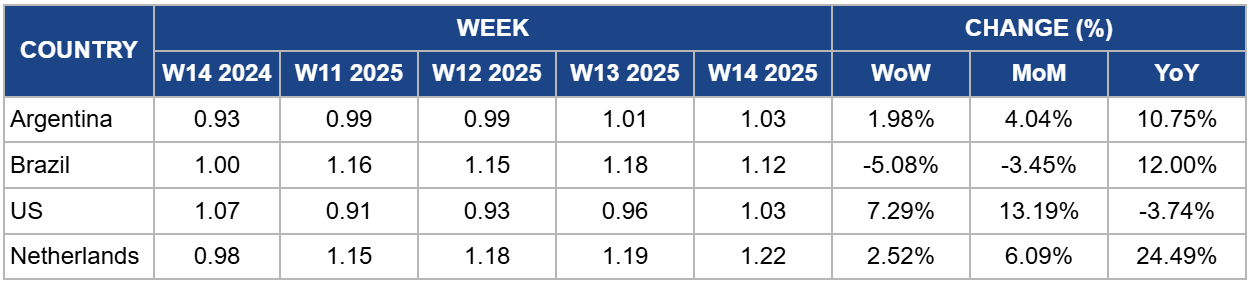

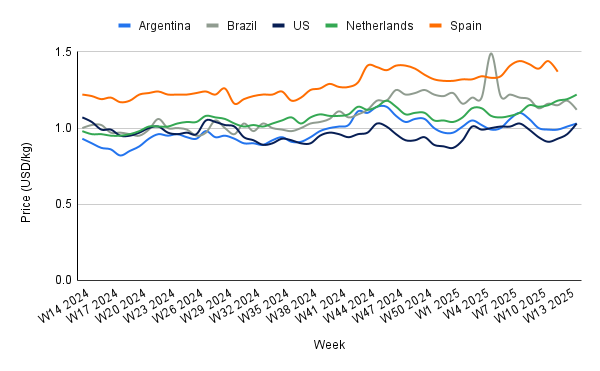

Weekly Soybean Oil Pricing Important Exporters (USD/kg)

Yearly Change in Soybean Oil Pricing Important Exporters (W14 2024 to W14 2025)

Argentina

Argentina’s soybean oil prices rose to USD 1.03 per kilogram (kg) in W14, up 1.98% week-on-week (WoW) and 10.75% year-on-year (YoY), driven by tight supply conditions. Farmers are withholding soybean sales due to exchange rate uncertainty and expectations of potential tax relief, pushing sales to a 10-year low. This limited availability is supporting higher prices in the short term. If current tax and exchange rate uncertainties persist, supply constraints may keep prices elevated. However, any policy shifts—such as reduced export taxes or currency stabilization—could unlock sales, increasing supply and easing price pressure.

Brazil

Brazil’s soybean oil prices decreased to USD 1.12/kg in W14, marking a 5.08% WoW decline and a 12% YoY increase. The weekly decline was driven by lower demand in the domestic market. Despite a slight 0.5% reduction in the 2025 soybean harvest forecast, production is still expected to reach a record 170.9 mmt, supported by yield improvements. The Brazilian Vegetable Oil Industry Association (Abiove) raised its soybean oil export forecast by 27.3%, citing the government’s decision to maintain the biodiesel blend at 14%. This policy supports domestic demand, offsetting potential downward pressure from lower soybean prices.

United States

In W14, US soybean oil prices rose to USD 1.03/kg, marking a 7.29% WoW and 13.19% month-on-month (MoM) increase from USD 0.91/kg. This price rise is linked to growing optimism over ongoing negotiations among oil and biofuel industry stakeholders—reportedly encouraged by the US administration—to address uncertainty over future biofuel mandates. Increased speculation around potential increases in biofuel blending mandates, particularly proposals to raise biodiesel production quotas for 2026, has also fueled the price rise.

Soybean oil, a key input in biodiesel production, plays a central role in supporting broader soybean prices. Continued speculation about federal biofuel policies has contributed to market volatility but also boosted short-term price momentum. If a consensus is reached and supportive mandates are announced, prices may remain elevated. However, without policy clarity, volatility could persist. Additionally, trade tensions with China continue to put pressure on US soybean free-on-board (FOB) values relative to Mercosur origins, further emphasizing soybean oil's importance in maintaining US market competitiveness.

Netherlands

In W14, soybean oil prices in the Netherlands increased to USD 1.22/kg, marking a 2.52% weekly rise and a 24.49% yearly increase. As a crucial trade hub in Europe, the Netherlands imports nearly all of its soybean supply, with the Port of Rotterdam playing a key role in distributing oil across the European Union (EU). The uptick in prices is driven by rising regional demand and a strengthening euro, both of which are expected to continue exerting upward pressure on prices in the near term. However, potential disruptions in supply chains or changes in European renewable energy policies could introduce volatility, impacting price trends.

3. Actionable Recommendations

Monitor Policy Changes in Key Soybean Oil Export Markets

Importers and refiners should closely track policy decisions in key markets like Argentina, Brazil, and the US, particularly regarding export taxes, biodiesel mandates, and biofuel policies. Early identification of favorable shifts, such as tax reductions or adjustments to biofuel blending mandates, can help secure more competitive pricing and stable supply.

Diversify Sourcing to Manage Price and Supply Volatility

To mitigate the impact of rising soybean oil prices and supply disruptions, importers should diversify their sourcing strategies. Exploring alternatives in regions such as Argentina and Brazil, where export forecasts are rising, and securing long-term contracts with multiple suppliers, can help balance risks tied to price fluctuations or geopolitical factors.

Adapt to Demand Shifts and Local Market Conditions

Given the varying demand and production conditions in markets like India and China, businesses should consider adapting their sourcing strategies to local supply dynamics. For example, expanding soybean oil imports in India, where local prices are under pressure, or taking advantage of China’s rising demand could present opportunities for both supply security and profitability.

Sources: Tridge, Grain Trade, UkrAgroConsult, Dhaka Tribune, Oils & Fats International