.jpg)

In W2 in the wheat landscape:

- Australia projects a significant boost in wheat production during 2024/25 MY, with an expected output of 31.9 mmt, marking a 23% YoY increase.

- Russia’s wheat exports to China surged significantly in early 2024 but dropped in November 2024 due to supply tightness amid export restrictions.

- Egypt secured contracts for 1.267 mmt of Russian wheat to ensure supplies through mid-2025.

- The Philippines is projected to import 7.2 mmt of wheat in 2024/25, driven by rising demand.

- Russian wheat prices remained steady, but concerns over supply persist, while US wheat prices declined due to record global supplies and a strong dollar.

1. Weekly News

Australia

Australia’s Wheat Production Expected to Surge by 23% YoY in 2024/25 MY

Australia forecasts a notable increase in wheat production during 2024/25 marketing year (MY), with an expected output of 31.9 mmt, representing a 23% year-on-year (YoY) increase. However, concerns have emerged regarding quality downgrades due to heavy rainfall that delayed the harvest and affected test weight. In Western Australia, farmers face lower-than-expected protein levels in the crop, further impacting quality. The country is projected to export between 22 to 23 mmt of wheat, with China's return to the global wheat market driving increased demand. In contrast, India, which has been absent from markets due to an export ban and high tariffs, is expected to see a rise in production during the 2024/25 MY.

China

China's Russian Wheat Imports Surged 2.9 Times in 2024

From Jan-24 to Nov-24, China imported USD 86.5 million worth of Russian wheat, marking a 2.9-fold increase. However, Russian wheat exports to China in Nov-24 dropped by more than half, amounting to USD 2.3 million, compared to USD 5.1 million in Nov-23. Despite this decline, Russia retained its position as the third-largest supplier of wheat to China, following Kazakhstan at 5.8 million and Canada at USD 3.2 million. Overall, China-sourced wheat from five countries from Nov-24.

Egypt

Egypt Secures 1.267 MMT of Wheat, Strengthening Supplies Through Jun-25

Egypt secured contracts for 1.267 million metric tons (mmt) of wheat, primarily sourced from Russia, ensuring sufficient supplies until the end of Jun-25. This procurement strategy reduces the immediate need for additional wheat purchases, especially with Egypt's domestic harvest set to begin in the second half of Apr-25. Earlier, major Russian exporters negotiated with and agreed to participate in its tenders. In the first half of the 2024/25 MY, Egypt emerged as the leading importer of Russian wheat, boosting purchases by 1.8 times to 5.3 mmt, up from 2.9 mmt in the previous season.

Philippines

Rising Demand for Wheat Products Drives 4.1% YoY Growth in Philippine Imports

The Philippines is expected to import more wheat during the 2024/25 MY, driven by increasing demand for products like bread, cakes, and noodles, alongside population growth. According to the United States Department of Agriculture (USDA), the inflow of wheat cargoes to the Philippines from Jul-24 to Jun-25 is projected to reach 7.2 mmt, marking a 4.1% YoY increase compared to the 6.9 mmt imported during 2023/24 MY.

United Kingdom

UK Wheat Harvest in 2024 Hits Lowest Level Since 2020

The Department for Environment, Food and Rural Affairs has reported a decline in the United Kingdom's (UK) wheat production compared to the previous year and the five-year average. The 2024 wheat harvest dropped significantly by 20% YoY, yielding 11.1 mmt, with the sown area and yields falling by 10% from the five-year average. This marks the lowest wheat harvest since 2020, primarily due to adverse weather conditions impacting crop growth and yields.

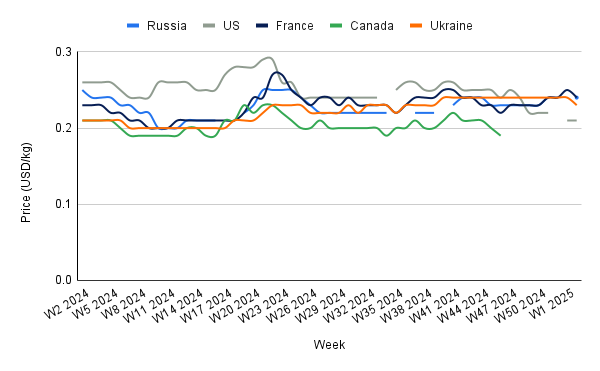

2. Weekly Pricing

Weekly Wheat Pricing Important Exporters (USD/kg)

Yearly Change in Wheat Pricing Important Exporters (W2 2024 to W2 2025)

Russia

In W2, Russian wheat prices remained unchanged week-on-week (WoW) at USD 0.24 per kilogram (kg). However, prices declined by 4% YoY from USD 0.25/kg in W2 2024. Despite this stability, concerns have arisen regarding a potential decrease in wheat supply from Russia due to several factors. One significant concern is the adverse weather conditions affecting early wheat growth. Drought and other climatic challenges have led to reduced production forecasts, with the USDA estimating a decrease in Russian wheat production to 83 mmt for the 2024/25 MY, down from previous projections. Furthermore, the Russian government has implemented export restrictions to manage domestic food prices and ensure local supply. These measures have limited the volume of wheat available for export, further tightening the global wheat market.

United States

In W2, United States (US) wheat prices stood at USD 0.21/kg, a decline of 4.55% month-on-month (MoM) and 19.23% YoY. This decrease is mainly due to expectations of record global wheat supplies and the strong US dollar , which have exerted downward pressure on prices. The USDA forecasts the US wheat crop to increase by 11% YoY in 2025, totaling approximately 2 billion bushels. This abundant supply has significantly contributed to the price decline. Moreover, the strengthening of the USD made US wheat exports more expensive, potentially reducing demand from major importers such as the Philippines, Mexico, and Japan.

France

In W2, French wheat prices declined by 4% WoW, reaching USD 0.24/kg, with a 4.35% increase YoY. This decline comes despite reduced wheat production forecasts for the 2024/25 MY. The French Ministry of Agriculture has lowered its estimate of soft wheat production to 25.78 mmt, a decrease of 540 thousand mt from previous projections. This adjustment reflects a 17% reduction in planted acreage and a 15% decrease in yields compared to 2023/24.

Ukraine

In W2, Ukrainian wheat prices declined 4.17% WoW and MoM to USD 0.23/kg. The wheat harvest forecast in Ukraine remained unchanged at 22.9 mmt, but the export forecast was reduced to 16 mmt. Despite the drop, prices rose by 9.52% YoY, primarily due to reduced wheat production in major exporting countries such as Russia and the European Union (EU), which has led to a more competitive market for Ukrainian wheat. For example, Russia's 2024 wheat harvest decreased by 10 mmt compared to the previous year, and the EU also experienced a smaller harvest, resulting in less wheat available for export. Furthermore, Ukraine's wheat exports have been robust, with significant sales to countries like Egypt, which purchased 120 thousand mt of Ukrainian wheat in 2024.

3. Actionable Recommendations

Strengthen Quality Assurance and Sustainability Initiatives to Meet Global Standards

Given the quality downgrade risks in Western Australia, Australian wheat producers should invest in quality assurance programs that ensure grain meets global specifications, targeting Asian feed markets. Initiatives such as continuous quality testing during harvest and partnerships with third-party certifiers can help ensure protein and test weight meet market requirements. Moreover, sustainable farming practices such as soil health management, water-saving irrigation techniques, and low-emission farming practices can improve wheat quality and align with global sustainability standards, making Australian wheat more attractive to international buyers.

Capitalize on Growing Demand in the Philippines with Long-Term Supply Agreements

The Philippines plans to increase its wheat imports, driven by rising consumption of baked goods, bread, and noodles. Australian exporters can focus on building long-term supply agreements with local food manufacturers and flour mills to stabilize their position in this market. By negotiating bulk contracts directly with millers and food processors, Australian exporters can lock in consistent supply at predictable prices, ensuring a steady foothold in the country’s expanding wheat market. Additionally, leveraging trade agreements like the Australia-Philippines Free Trade Agreement (APFTA) could further reduce tariffs and enhance market access, giving Australian wheat a competitive edge in pricing and delivery reliability.

Diversify Export Markets to Offset Quality Concerns in Australian Wheat

Australia’s wheat production is projected to rise significantly, but concerns around quality due to weather impacts present challenges in maintaining stable demand in traditional markets like Southeast Asia. To mitigate this, Australian wheat exporters should diversify their export destinations by targeting East African countries like Kenya and Tanzania, increasingly sourcing higher-quality wheat for growing bakery industries. These regions rely on imports to meet domestic demand, making them potential buyers for Australian wheat. Establishing partnerships with local milling companies and bakeries can create consistent demand and allow Australia to maintain competitive pricing in these emerging markets.

Sources: Tridge, Grain Trade, Foodmate, Hellenic Shipping News, UkrAgroConsult