1. Weekly News

China

China's Raw Milk Prices and Dairy Production Significantly Decline

According to the Ministry of Agriculture and Rural Affairs of the People's Republic of China, the country’s raw milk prices in ten provinces, including Heilongjiang and Inner Mongolia, decreased by 1.8% month-on-month (MoM) and 13.8% year-on-year (YoY) to USD 0.45 per kilogram (kg) in Jul-24. Dairy production for Jul-24 reached 2.26 million metric tons (mmt), reflecting a 5.7% YoY decline. From Jan-24 to Jul-24, total dairy output accumulated 18 mmt, marking a 3.4% YoY decrease. This decline in production and prices highlights challenges in China's dairy sector.

Russia

Russia's Daily Milk Sales Increased by 3.4% YoY in 2024

As of August 26, 2024, the Ministry of Agriculture of the Russian Federation (MARF) reported that the country's average daily milk sales reached 56.2 thousand metric tons (mt), showing a 3.4% YoY increase. The Republic of Tatarstan, the Udmurt Republic, the Krasnodar Territory, Voronezh, and Kirov led the consumption. The average milk yield per cow per day was 22.3 kg, 1.1 kg higher than in 2023. The regions showing the highest growth in milk yield were the Krasnodar Territory, St. Petersburg, Leningrad, Kursk, Kaluga, and Kaliningrad, with the yield exceeding 27 kg of milk per cow per day.

Netherlands

Netherlands' Milk Supply Continues Downward Trend

The Netherlands' milk supply saw a 3% YoY decline in Jul-24, with the decrease rate accelerating since Jun-24. Cumulatively, milk production from Jan-24 to Jul-24 was 1.6% lower than in 2023. This downward trend, which began in Sep-23, is primarily attributed to the outbreak of the bluetongue virus and the gradual phasing out of the derogation.

United Kingdom

Great Britain's Milking Herd Declines by 0.3% YoY in 2024

As of July 1, 2024, Great Britain's milking herd totaled 1.61 million heads, representing a 0.3% YoY decrease compared to the previous year, according to the British Cattle Movement Service (BCMS). This decrease is due to reductions across all age categories except for cows aged two to four. The average age of cows in the milking herds in Great Britain is now 4.55 years, slightly younger than the previous year's average. The most significant contributor to this YoY decline is heifers aged 12 to 24 months. In contrast, the two to four years category increased by nearly 16 thousand heads from 2023, driven by the calves born in the youngstock boom of 2021 now aging into the milking herd.

United States

California Reports First Case of Highly Pathogenic Avian Influenza H5N1 in Dairy Cattle

The California Department of Food and Agriculture (CDFA) has confirmed the first case of the highly pathogenic avian influenza (H5N1) in dairy cattle in the Central Valley region. The department has been preparing for this since early 2024, drawing on its experience managing avian viruses to address the situation effectively. While the strain does not significantly threaten the general population, farm workers in direct contact with infected cattle may be at risk. No human infections related to the outbreak have been reported in California. Affected dairy farms have been quarantined, and enhanced biosecurity measures are in place. As of W36, the state's supply of animal protein remains unaffected.

2. Weekly Pricing

Weekly Powdered Milk Pricing Important Exporters (USD/kg)

Yearly Change in Powdered Milk Pricing Important Exporters (W36 2023 to W36 2024)

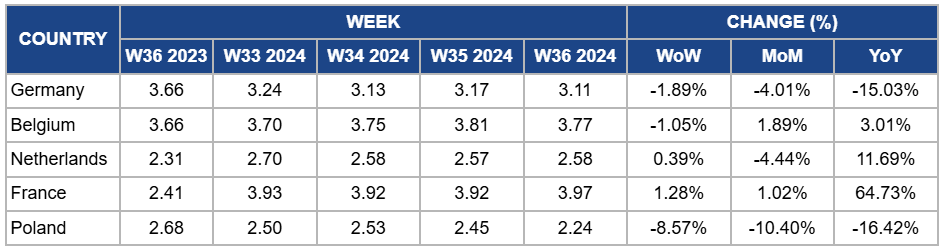

Germany

In W36, Germany's powdered whole milk prices decreased by 1.89% week-on-week (WoW), falling to USD 3.11/kg from USD 3.17/kg in W35. MoM prices dropped by 4.01%, while the YoY decline was 15.03%. This downward trend reflects the country's reduced powdered whole milk demand and a shift to higher-profit products such as cheese and butter. In addition, the country’s farmgate price of raw milk can only cover 77% of the production cost, which will continue to challenge the industry.

Belgium

In W36 2024, Belgium’s powdered whole milk prices decreased by 1.05% WoW, reaching USD 3.77/kg compared to USD 3.81/kg in W35. Despite this weekly drop, prices rose by 1.89% MoM and 3.01% YoY. The bluetongue virus outbreaks, combined with improved milk quality due to better farming practices, have kept prices high despite the short-term fluctuations.

Netherlands

The Netherlands’ skimmed milk powder prices slightly increased by 0.39% WoW in W36, reaching USD 2.58/kg, up from USD 2.57/kg in W35. However, prices fell by 4.44% MoM but rose by 11.69% YoY. The dairy market in the Netherlands has experienced fluctuations this week due to the ongoing impact of the bluetongue virus outbreak, contributing to overall supply constraints. In addition, as Christmas approaches, the production demand for butter and cheese will increase in the following months, influencing the country’s raw milk prices.

France

France’s semi-skimmed milk powder prices increased by 1.28% WoW in W36, reaching USD 3.97/kg, up from USD 3.92/kg in W35. This was accompanied by a 1.02% MoM rise and a substantial 64.73% YoY increase. The WoW price decline can be attributed to the overall production decline in the European Union (EU) due to the bluetongue virus outbreak. In addition, the climate challenges and increasing production costs further driving up market prices.

Poland

Poland's skimmed milk powder prices significantly declined, dropping by 8.57% WoW to USD 2.24/kg in W36, compared to USD 2.45/kg in W35. The MoM decline was 10.40%, with a YoY decrease of 16.42%. The price decrease is due to Poland's increased milk production in 2024 and China's investigation into EU dairy subsidies. As one of China's major milk powder suppliers, this trade dispute will significantly impact Poland's production patterns and market prices.

3.Actionable Recommendations

Strengthen Biosecurity Measures Amid H5N1 Outbreak

Following the first case of H5N1 in dairy cattle in California, dairy farmers should continue to reinforce biosecurity measures, especially for workers in direct contact with livestock. Continued collaboration with state agricultural agencies to implement quarantine measures and vaccination campaigns can prevent the virus from spreading further. Additionally, ensuring transparent communication with buyers and maintaining public trust in dairy products will help mitigate any market disruptions.

Adapt to Market Shifts Toward Butter and Cheese

To counteract the decline in powdered whole milk prices, dairy producers in Germany should focus on diversifying production into higher-margin products such as cheese and butter, which continue to experience demand growth. Dairy farms should also evaluate operational efficiencies since farmgate prices for raw milk cover only 77% of production costs. Investing in energy-efficient technologies and optimizing feed to lower input costs can provide some relief from financial pressures.

Plan for Seasonal Demand and Supply Constraints

Given the upcoming increase in demand for butter and cheese for the holiday season, Dutch dairy processors should prioritize strategic planning for raw milk allocation. With skimmed milk powder prices rising slightly but experiencing monthly fluctuations, producers can benefit from hedging contracts to lock in prices and mitigate risks associated with supply constraints due to the bluetongue virus. Exploring export opportunities for higher-value dairy products may also provide financial stability.

Sources: Tridge, Foodmate, Ganaderia, Melkveebedrijf, Ahdb, Milknews