.jpg)

1. Weekly News

Europe

EU’s 2024 Wheat Production Forecast Lowered to 122.47 MMT

The European Organization of Traders in Cereals, Oilseeds, Vegetable Oils, and Meals (COCERAL) has forecasted the total production of soft and durum wheat in the European Union (EU) for 2024 to be only 122.47 million metric tons (mmt), representing a decrease from 129.91 mmt estimated in Jun-24 and a significant drop from the 133.79 mmt produced the previous season. The decline in wheat production is primarily due to common wheat, with COCERAL estimating its yield in the EU for 2024 at just 114.93 mmt. This is a reduction from the 122.64 mmt projected in Jun-24 and down from 126.38 mmt harvested in 2023. Moreover, COCERAL has made a notable adjustment to its estimate for soft wheat production in France, reducing it by 4.18 mmt from the 30.35 mmt forecasted in Jun-24. This revised figure is nearly 9 mmt less than harvested in the previous season, indicating significant challenges in the French wheat sector.

Russia

Adverse Weather Delays Wheat Harvest in Russia

Adverse weather conditions and abundant rainfall in Sep-24 severely delayed the grain harvest in key Russian regions such as the Urals, Siberia, and the Volga. Only 50 to 60% of the grain area has been harvested in these regions, leaving around 8 million hectares (ha) of grain crops, predominantly spring wheat, still unharvested. Nationwide, 10.6 million ha of grain crops remain uncollected. As of W39, Russia harvested 78% of the grain area, producing 105.9 mmt of grain, including 77.7 mmt of wheat. Russia set the 2024 wheat harvest forecast at 82 to 83 mmt, and while improving weather conditions are anticipated to speed up the harvest, some crop losses are forecasted.

Ukraine

Ukraine's Wheat Exports Up 87.1% as of Sep-24

According to the Ministry of Agrarian Policy and Food of Ukraine, Ukraine exported 9.764 mmt of grain and leguminous crops for the 2024/25 season as of September 25, 2024, marking a 58.7% year-on-year (YoY) increase. Wheat exports reached 5.59 mmt, marking an 87.1% YoY rise from the 2023/24 season.

Yemen

Hodeidah Port Faced Sharp Decline in Wheat Imports Amid Ongoing Red Sea Attacks

The Yemeni government reported a sharp 54% month-on-month (MoM) decline in wheat imports through the Houthi-controlled Hodeidah port in Aug-24, attributed to Israeli airstrikes and attacks by Iran-backed Houthi militias on international shipping. Despite this, wheat imports at main ports increased during the first eight months of 2024 by 12% YoY, ensuring that food and fuel supplies remained ample, with significant shortages not expected in the short term. Moreover, the Yemeni rial in government-controlled areas depreciated by 2% MoM in Aug-24, reaching a historic low of 1,904 per USD, marking a 26% YoY drop due to depleted foreign reserves and banking disruptions. Meanwhile, stricter exchange rate controls in Houthi-controlled regions have helped stabilize their local currency, though ongoing banking crises present risks of further depreciation.

2. Weekly Pricing

Weekly Wheat Pricing Important Exporters (USD/kg)

Yearly Change in Wheat Pricing Important Exporters (W39 2023 to W39 2024)

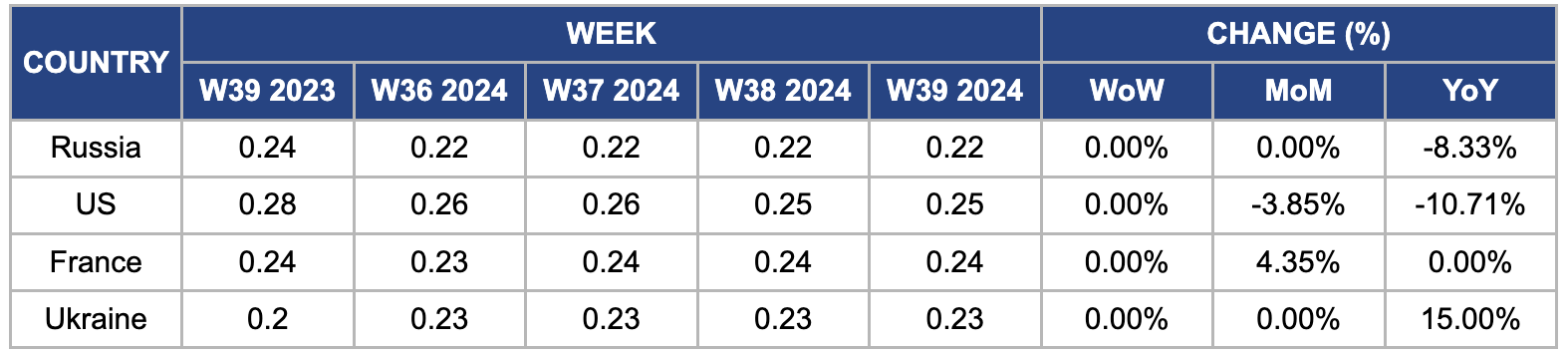

Russia

In W39, Russian wheat prices remained stable at USD 0.22 per kilogram (kg), although this reflects an 8.33% decline YoY from USD 0.24/kg in the same week of 2023. The price decline is due to an increased wheat harvest forecast estimated at around 82 to 83 mmt, with improving weather conditions expected to expedite harvesting efforts. Moreover, as of July 1, 2024, Russia's wheat reserves reached a record 20.3 mmt, a 21% increase from the previous year. This reserve surge has been fueled by an early harvest and favorable weather conditions, positioning Russia well in the global wheat market.

United States

In W39, United States (US) wheat prices remained unchanged week-on-week (WoW) at USD 0.25/kg. However, they have declined 3.85% MoM and 10.71% YoY. This decrease is due to lower demand for US wheat, increased competition from Black Sea suppliers, weaker exports, and improved conditions for US winter wheat planting. Wheat sales for the 2024/25 season totaled 168.90 thousand metric tons (mt) in W39, significantly below the anticipated range of 225 thousand mt to 600 thousand mt. This price trend reflects the ongoing weak demand despite favorable weather conditions and an interest-rate cut from the Federal Reserve, which has not significantly boosted demand.

France

French wheat prices remained steady WoW but rose 4.35% MoM to USD 0.24/kg in W39. This increase is consistent with the International Grains Council's (IGC) revised global wheat production forecast for the 2024/25 season, which reflects poor harvest conditions in France. Moreover, French soft wheat exports outside the EU are projected to decline by 60% YoY to 4.1 mmt, marking the lowest export levels in 23 seasons. This significant drop is due to heavy rainfall that damaged crops and adversely affected exports to key markets, including Morocco, Algeria, and Tunisia.

Ukraine

In W39, Ukrainian FOB wheat prices remained steady at USD 0.23/kg but surged 15% YoY. This price increase is primarily due to concerns over drought conditions in Ukraine, which are expected to hinder the planting of winter wheat for the 2025 harvest. Ukrainian farmers face challenges from adverse weather and the ongoing war. The unfavorable weather has significantly reduced the area sown with winter wheat, now estimated at approximately 4.2 million ha, compared to 4.4 million ha the previous year. A smaller harvest and lower carryover stocks have further reduced the exportable surplus, contributing to the price rise.

3. Actionable Recommendations

Adapt to Climate Challenges and Strengthen Agricultural Practices

The EU, particularly France, should enhance climate resilience in wheat production by adopting drought-resistant wheat varieties and improving water management systems. Efforts to mitigate the impact of erratic weather and rainfall are crucial. Integrating precision agriculture technologies, such as weather monitoring and automated irrigation, can optimize input use and maintain stable yields. These advancements will support the EU in ensuring more consistent wheat production and securing its role as a leading supplier to wheat-reliant regions such as North Africa and the Middle East.

Increase Production Resilience and Innovate Farming Techniques

Facing delayed harvests due to adverse weather in regions like the Urals and Siberia, Russia should prioritize improving harvest efficiency by adopting weather-resilient technologies and optimizing harvest logistics. Investments in machinery upgrades and satellite-based tracking systems for crop progress can mitigate losses and secure long-term production stability. Meanwhile, Ukraine should capitalize on rising global demand by continuously innovating crop production and disease management.

Strengthen Export Strategies and Market Diversification

France, the US, and Ukraine should focus on diversifying their wheat export markets to navigate global challenges and expand their trade footprint. As France's wheat exports outside the EU are projected to decline by 60% YoY due to adverse weather, strengthening trade ties with alternative markets in Asia and Africa is vital. Meanwhile, facing competition from Black Sea suppliers, the US should explore new partnerships in regions with rising demand, such as Southeast Asia. With its growing wheat exports, Ukraine should reinforce infrastructure and logistics to maximize export potential amid domestic and regional challenges, including war and drought.

Sources: UkrAgroConsult, Graintrade, Agrotimes