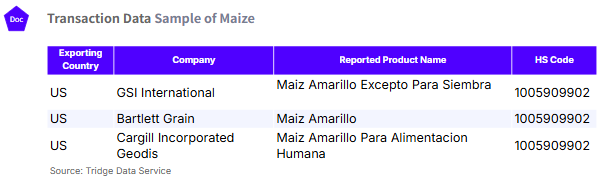

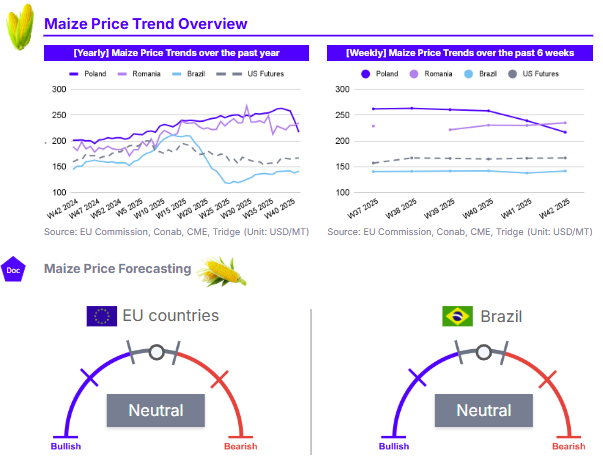

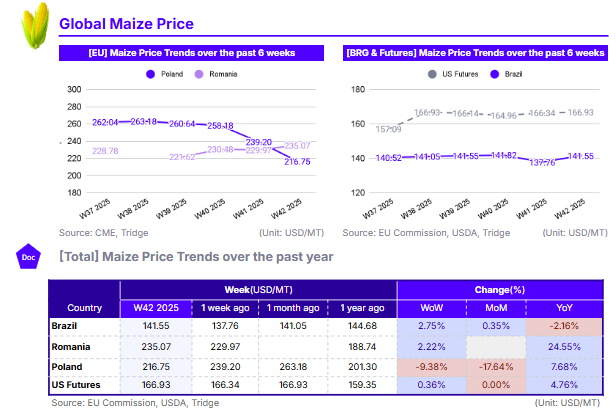

In W42 2025, maize prices showed significant regional divergence. The US market remained stable, with futures prices flat month-on-month (MoM) at USD 166.93 per metric ton (mt). This stability is anchored by the massive 16.8 billion bushel crop forecast in the September WASDE report, which has offset demand optimism. European markets were volatile, driven by conflicting harvest results. Poland’s prices crashed 17.64% MoM due to harvest pressure from better-than-expected yields in northern Europe. In contrast, Romania’s prices showed a 24.55% year-on-year (YoY) gain, reflecting tighter supplies in the southeastern region. In South America, Brazil’s prices saw a modest 2.75% week-on-week (WoW) rise to USD 141.55/mt, supported by strong near-term export demand as it begins planting its next crop. For near term purchases, the US remains a preferred origin, with identified suppliers including GSI International, Bartlett Grain, and Cargill.

1. Weekly Price Overview

Harvest Pressure in Poland Result in Short term Price Collapse

In Brazil, the price of maize was USD 141.55 per metric ton (mt) in W42, a 2.75% increase WoW. In Romania, the price was USD 235.07/mt, rising 2.22% WoW. Conversely, Poland experienced a sharp 9.38% WoW decline, with its price falling to USD 216.75/mt. US Futures remained stable at USD 166.93/mt, showing a minimal 0.36% WoW gain. Romania’s price increase was supported by strong demand from EU importers and and weather-related harvesting delays in Ukraine. In contrast, Poland’s sharp price drop reflects significant harvest pressure. Recent reports note that maize yields in northern Europe have exceeded expectations, adding to a bearish sentiment fueled by the International Grains Council (IGC) raising its global grain production forecast. Brazilian prices saw a modest gain, supported by strong export demand at the start of Oct-25 and some planting-season weather concerns, despite generally favorable conditions. The US market was largely unchanged, as persistent drought concerns and good demand optimism were completely offset by the September WASDE report’s massive production forecast, which continues to anchor the market. Also, due to the government shutdown in the US no official information is released by the United States Department of Agriculture (USDA), which limits market movement.

2. Price Analysis

High Export Demand Support Higher YoY Prices in Major Exporting Countries

In Poland, the price of maize fell significantly by 17.64% MoM, though its W42 2025 price of USD 216.75 per metric ton (mt) remains 7.68% higher YoY. In Romania, the price reached USD 235.07/mt, and while MoM data was unavailable, the price posted a substantial 24.55% YoY gain. The US Futures market was stable, remaining flat MoM at USD 166.93/mt, which is 4.76% higher YoY. Similarly, Brazil’s price was steady, rising just 0.35% MoM to USD 141.55/mt, reflecting a 2.16% YoY decline.

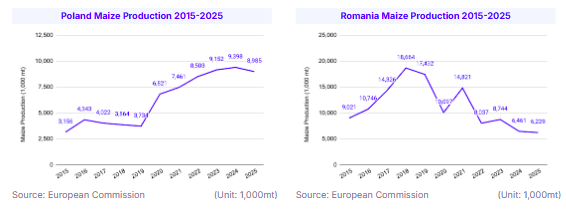

The sharp MoM drop in Poland is a direct result of harvest pressure, as recent reports indicate that maize yields across northern Europe have surpassed expectations. European Commission (EC) data indicates that Poland’s maize harvest expectation for 2025 is 8.99 million metric tons (mmt), 7.32% above the five year average. This influx of supply is weighing heavily on near-term prices. Lack of demand from the UK is also weighing heavily on Polish maize prices. However, the YoY gain in Poland reflects robust demand from EU trading partners in 2025. Conversely, Romania's significant YoY strength points to tighter supply conditions in the southeastern EU region compared to the previous year. This is backed up by EC data which indicates Romania’s 2025 maize harvest at 6.23 mmt, 30.47% below the five year average.

The stability in the US market is directly linked to the September WASDE report. This report's bearish forecast for a near-record 16.8 billion bushel crop has been fully absorbed, capping any price rallies. However, the same report projected record exports of 3.0 billion bushels, establishing a strong price floor and explaining the 4.76% YoY strength. With the ongoing US government shutdown, no new official USDA data is being released, contributing to the flat MoM price. Brazil’s stable price reflects a market balancing strong current export demand against the favorable planting outlook for its 2025/26 crop.

3. Strategic Recommendations

Capitalize on Record US Production for Maize Procurement

Global maize buyers should prioritize the US as the primary procurement destination for maize contracts in the coming months (Q4 2025 – Q1 2026). The fundamental driver for this strategy is the large crop currently being harvested in the US. The USDA's September WASDE report projected a near-record US corn production of 16.8 billion bushels. This immense volume is the result of a significant expansion in harvested area, which is forecast at 90.0 million acres, the largest area harvested since 1933.

This large supply ensures availability and market liquidity for buyers needing to secure substantial volumes. This supply-driven environment makes the US a reliable and secure source for fulfilling large tenders and building strategic reserves. The scale of the 2025/26 crop, which is forecast to be large enough to meet all domestic demand and achieve record exports of 3.0 billion bushels, provides a deep well of supply for the global market. Buyers can confidently execute major purchases, assured that the physical supply is readily available. This supply glut has anchored US prices, making it a competitive and stable source for short term, large-volume procurement. According to Tridge Eye data, US suppliers to consider for purchasing maize include GSI International, Bartlett Grain, and Cargill.