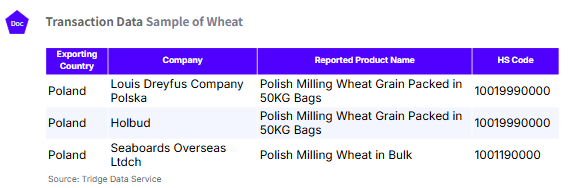

.jpg)

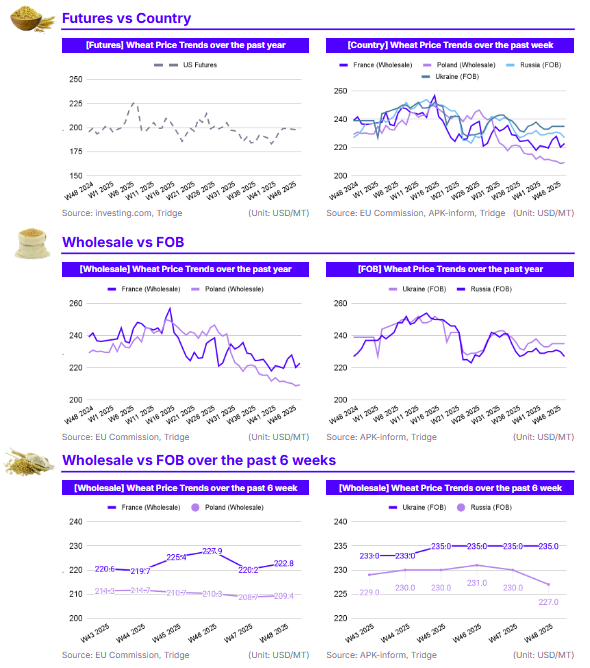

In W48 2025, prices remained relatively stable in major wheat producing countries, with no swings beyond 1.5% in either direction. The US and EU markets exhibited minor WoW gains, while Russian FOB prices declined 1.30% WoW to USD 227.0/mt due to pressure from Southern Hemisphere supply. French wholesale prices, at USD 222.8/mt, gained 1.43% MoM, but like Poland (USD 209.4/mt), remain locked in deep YoY declines (France -6.81% YoY, Poland -8.67% YoY). This structural compression is due to high global and European production and as confirmed by the November WASDE report, the first YoY stock build up since 2019/20. The US (+1.67% YoY) and Russian (0.00% YoY) markets demonstrate unique resilience against this global glut. For EU buyers, Poland offers the most cost-competitive sourcing opportunity, providing a USD 13.4/mt discount compared to France. Conversely, France is the preferred option for large-scale fulfillment due to its high volume and liquidity.

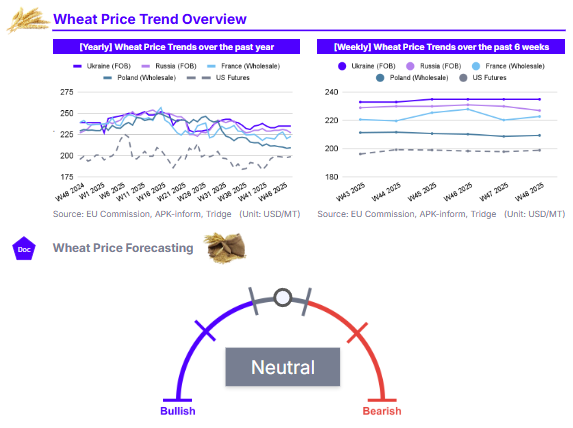

1. Weekly Price Overview

European Prices Rebound Marginally as Southern Hemisphere Supply Pressures Russian Values

In W48 2025, the market saw a clear contrast between an upward correction in the European Union (EU) and a downward adjustment in Russian prices. France's wholesale price rose 1.18% week-on-week (WoW) to USD 222.8 per metric ton (mt). This strong gain is primarily a market correction following a price dip in W47, supported by the continued brisk pace of planting for the 2026 crop. US Futures also posted a modest 0.49% WoW gain, reaching USD 198.8/mt, finding slight support from strong export demand and Black Sea tensions. Poland's wholesale price edged up slightly by 0.31% WoW to USD 209.4/mt.

In contrast, Russia's Free on Board (FOB) price declined 1.30% WoW to USD 227.0/mt. This drop is attributed to stiff competition and pressure from the promising crop prospects in the Southern Hemisphere, particularly the large harvests coming out of Australia and Argentina. Meanwhile, Ukraine's FOB price remained unchanged at USD 235.0/mt, displaying short-term market. This is largely attributed to the subdued demand experienced in the Ukrainian wheat industry currently.

2. Price Analysis

Supply Glut Locks European Prices in Deep YoY Decline While US and Black Sea Markets Demonstrate Resilience

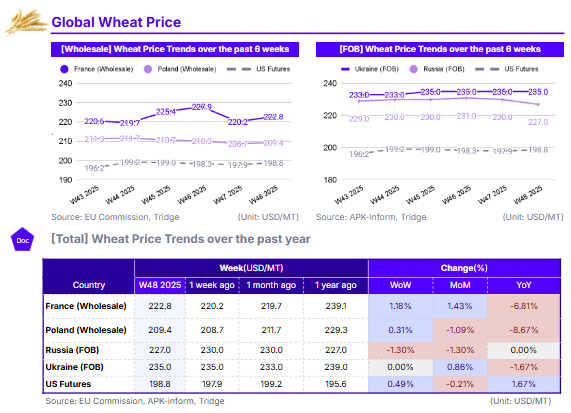

The long-term price structure remains fundamentally bearish across most markets, reflecting a persistent global supply glut. The European wholesale markets, specifically France and Poland, continue to suffer the deepest impact from the global oversupply, translating directly into substantial YoY price compression. In Poland, wholesale prices fell 1.09% month-on-month (MoM) to USD 209.4/mt, culminating in the most severe price drop at 8.67% YoY. This decline is attributed to the larger 2025 Polish harvest, coming in at 13.41 million metric tons (mmt), 4.94% above the five-year average. Similarly, in France, the wholesale price of USD 222.8/mt is down 6.81% YoY. This large decrease is driven by the strong domestic production recovery in 2025, coupled with stiff export competition from Australia and Argentina, which has challenged France's traditional market share.

A wider EU wheat harvest growth is compounding the downward pressure on European prices, with the European Commission pegging 2025 EU wheat production at 143.55 mmt, 9.17% above the five-year average. Furthermore, the structural pressure from the global glut is worsening the price situation in Europe, confirmed by the November WASDE report, which projected global supplies to increase by 11.7 mmt to 1,090.3 mmt and raised global ending stocks by 7.4 mmt, signaling the first YoY stock build since 2019/20.

In contrast to Europe, the US and Black Sea markets exhibit structural price resilience that defies the overall bearish global trend. US Futures, despite a slight MoM decline of 0.21%, gained 1.67% YoY to USD 198.8/mt. The US market is supported by strong cumulative export demand and ongoing Black Sea tensions, which counteract the pressure from record global production. The Russian FOB price achieved YoY parity at USD 227.0/mt, despite falling 1.30% MoM. This price parity showcases stability and managed supply, successfully offsetting the current severe downward pressure caused by record crop prospects in the Southern Hemisphere. Ukraine's FOB price also shows resilience, with a minimal -1.67% YoY drop, supported by a slight MoM gain of 0.86% and the seasonal expectation of rising importer demand. However, demand in the Ukrainian wheat market has been uncharacteristically slow, which could mean stable prices in the foreseeable future.

3. Strategic Recommendations

Prioritize Poland For Cost-Competitive Sourcing in Europe

For price-sensitive buyers in the European market, Poland remains the preferred origin to optimize procurement costs, capitalizing on a significant market discount compared to other European suppliers. The underlying global supply scenario is fundamentally bearish, translating to price compression across the region compared to last year. As of W48, Polish wholesale wheat is priced at USD 209.4/mt. This offers a clear price advantage, providing a USD 13.4/mt discount compared to French wholesale prices of USD 222.8/mt. The price gap between France and Poland have widened in recent weeks. Thus, the fundamental reasons for Poland’s discount persist. The price is protected by strong supply fundamentals, including Poland’s high 2025 production, expected at 13.41 mmt. Securing volumes from Poland allows buyers to capitalize on the country’s steep 8.67% YoY price decline and maximize the price spread available among major Western European producers.

Secure Large-Scale European Volume and Liquidity via France

Large-scale processors and multinational buyers whose priority is stable, high-volume fulfillment should prioritize sourcing from France, with its larger availability justifying the necessary price premium. As of W48, France’s market price reflects its domestic stability, showing a strong 1.43% MoM gain to USD 222.8/mt, and remains more stable than Poland on a long-term basis. While the USD 13.4/mt premium exists, this cost reflects a market with significantly greater liquidity and reliable infrastructure for large trades. France’s strong 2025 production recovery is the primary driver of its YoY price decline, resulting in ample free volumes. The combination of its expected 34.61 mmt production and fast-paced planting for the 2026 season guarantees the volume required for large scale operations. Buyers prioritizing supply reliability and the ability to execute large contracts will find the French market better equipped to manage logistics and volume volatility.