.jpg)

1. Weekly News

Global

ISO Forecasts Global Sugar Deficit for 2024/25 as Exports Decline and Ethanol Production Increases

The International Sugar Organization (ISO) has revised its global sugar balance for the 2024/25 season, forecasting a 2.51 million metric tons (mmt) deficit. The 2023/24 cycle ended with a surplus of 1.31 mmt, reversing a previous deficit due to lower consumption estimates. Global sugar production for 2023/24 is a record 181.36 mmt. In 2024/25, production is expected to remain steady, with the largest adjustment being a 0.35 mmt increase in China's output. World sugar consumption is forecast at 181.58 mmt, 1.29 mmt lower than previous estimates.

Exports for 2024/25 are projected to decline by 6.4 mmt to 63.13 mmt, partly due to constrained import demand and a global trend towards increased self-sufficiency. The global ending stocks-to-use ratio for 2023/24 is 54.3%, slightly lower than last season, with a projected 53.17% for 2025. Additionally, global fuel ethanol production and molasses output are forecasted to increase, with Brazil and India driving the growth in ethanol. These developments may impact future sugar prices by influencing global supply and demand dynamics, particularly with shifting export trends and rising competition for sugarcane in ethanol production.

European Union

EU Sugar Beet Sector Declines

The European Commission's (EC) long-term forecast for 2024 to 2035 predicts a gradual decline in sugar production within the European Union (EU), primarily due to shrinking sugar beet acreage and reduced consumer demand for sugar. Sugar beet cultivation is forecasted to fall from 1.6 million hectares (ha) in 2023 to 1.44 million ha by 2035 as farmers shift to alternative crops. Factors driving this trend include climate change, sustainability concerns, and evolving consumer diets that favor lower sugar intake.

Despite a record sugar price increase in 2023, prices have already begun to decline at USD 871.47 per metric ton (EUR 831/mt) in Apr-24, 2.3% higher than 2023 levels but reflecting a downward trend. With sugar consumption projected to decrease by 0.2% annually, EU sugar demand will reach 15.3 mmt by 2035. This outlook indicates continued challenges for European sugar beet production driven by evolving market dynamics, sustainability requirements, and changing consumer preferences, which collectively signal a need for adaptation within the sector.

Brazil

Brazil's Sugar Exports Slow in Dec-24, With Decreased Shipments and Revenue

Brazil's sugar exports have slowed, with the number of vessels waiting to load decreasing to 55 in W50, down from 60 the previous week. The total scheduled sugar shipment volume declined to 1.947 mmt, compared to 2.33 mmt the last week. Key export ports include Santos, Paranaguá, and São Sebastião, with Very High Polarization (VHP) sugar accounting for most shipments.

Exports in Dec-24 totaled 613,176 mt, generating USD 301.25 million, reflecting a 2% decrease in volume and a 40.9% drop in daily revenue compared to Dec-23. The average price per ton also fell by 8.7% to USD 538,00/mt, indicating a slowdown in global demand and lower prices.

India

India's Sugar Production Drops 35.4% in Oct-24, With Recovery Expected in 2025/26 MY

India's sugar production fell 35.4% year-on-year (YoY) to 2.79 mmt in Oct-24, primarily due to delayed starts in Maharashtra and Karnataka. Maharashtra's output dropped 66%, Karnataka's decreased by 36%, while Uttar Pradesh's production remained stable. For the 2024/25 season, India is expected to produce 28 mmt, down from 31.9 mmt in the previous season. This reduction in output could affect global sugar prices.

In addition, India's sugar production is forecasted to recover in the 2025/26 marketing year (MY), driven by favorable rains and expanded sugarcane cultivation. This recovery could allow India to resume exports after two years of restrictions. The increased production, resulting from farmers switching to sugarcane after losses in other crops, is expected to boost sugar exports by 3 to 5 mmt.

Peru

Peru-Thailand FTA to Boost Agricultural Trade

Peru and Thailand are set to finalize a Free Trade Agreement (FTA) next year, marking 60 years of diplomatic relations. The FTA aims to enhance trade, particularly in agriculture, with sugar emerging as one of the products Peru could significantly export to Thailand. As of Dec-24, Peru's agricultural exports to Thailand include grapes, avocados, and blueberries, while studies highlight untapped opportunities for products such as sugar, mandarins, and garlic. Thailand's USD 16 billion agricultural import market in 2022 underscores the growth potential. The agreement is forecasted to create jobs, support small enterprises, and expand Peru's agricultural exports in the competitive Asian market.

Ukraine

Ukraine's Sugar Exports Projected to Reach Record High in 2024

Ukraine's sugar beet harvest is nearing completion, with 12.1 mmt gathered from 98% of the sown area, yielding an average of 47.7 tons/ha. Sugar production reached 1.165 mmt, matching 2023's figures. In 2024, Ukraine is expected to export over 700,000 mt of sugar, the highest volume since 2000, despite restrictions. Between Jan-24 and Nov-24, 622,000 mt worth USD 356 million were exported.

For 2024/25, analysts forecast sugar production at 1.75 mmt and exports at 600,000 mt, slightly lower than 2023/24 levels of 1.8 mmt and 690,000 mt, respectively. Sown sugar beet areas rose to 258,000 ha. However, declining global sugar prices and weak export demand have kept domestic prices low at USD 0.55 per kilogram (UAH 23 to 24/kg).

2. Weekly Pricing

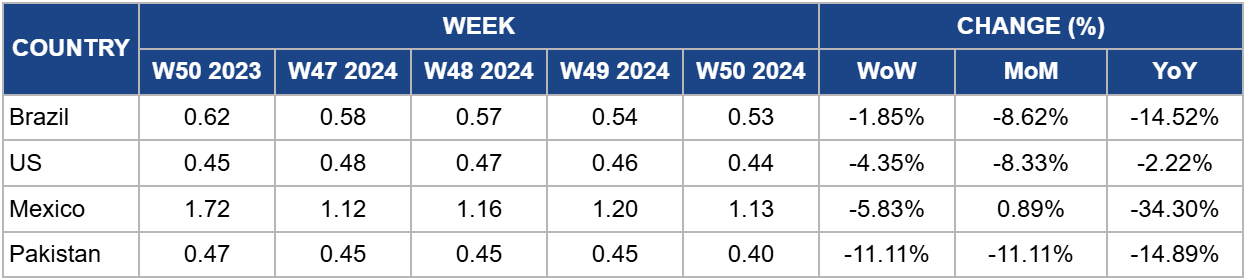

Weekly Sugar Pricing Important Producers (USD/kg)

Yearly Change in Sugar Pricing Important Producers (W50 2023 to W50 2024)

.png)

Brazil

Brazil's sugar prices dropped to USD 0.53/kg in W50, marking a 1.85% week-on-week (WoW) decrease and a 14.52% YoY decline. In the second half of Nov-24, sugar production in Brazil's Central-South region reached 1.08 mmt, a 23% decrease from last year but above market expectations. Sugarcane crushing fell by 15.2%, totaling 20.35 mmt, with delays caused by earlier rainfall shifting more activity to late Nov-24. Despite the production drop, stronger-than-expected results could signal price stabilization, though future sugar prices may remain volatile depending on weather conditions and production trends.

United States

In W50, United States (US) sugar prices declined to USD 0.44/kg, marking a 4.35% decrease WoW and an 8.33% month-on-month (MoM) drop. This price drop reflects factors affecting domestic production and import expectations. The United States Department of Agriculture (USDA) revised its sugar production forecast for the 2024/25 season downward by 45,359.25 mt to 9.22 mmt, marking the second consecutive reduction, primarily driven by lower sugar extraction from beet molasses. With US sugar production now expected to be lower than in 2023, this could put additional pressure on the market.

To compensate for the reduced domestic production, the USDA has increased its import projection for 2024/25 by nearly 272,155.5 mt. This increase is due to higher imports from Mexico, with the forecast raised from 358,338.5 mt to 506,218.5 mt. Imports also surged in early Dec-24, with over 145,149.6 mt paying high-tier tariffs. Despite the reduced production, the US sugar supply remains adequate, with a projected stocks-to-use ratio of 13.5%. However, the combination of decreased domestic production and higher reliance on imports could put upward pressure on US sugar prices in the future, especially if global market conditions or trade policies influence import volumes. The increased dependency on imports, particularly from Mexico, could lead to price fluctuations depending on international trade dynamics and tariffs.

Mexico

Mexico's sugar prices fell to USD 1.13/kg in W50, marking a 5.83% WoW decrease and a 34.30% drop YoY from USD 1.72/kg. The decline reflects ongoing challenges within the domestic sugar industry, as production has decreased due to high costs and low global market prices. The Mexican sugar sector has ceased exports, as the international market is not profitable, with prices below domestic production costs.

The government's support for sugarcane producers is under scrutiny, with calls for better monitoring to ensure it is effectively applied, particularly in light of the potential for tariffs on sugar imports as part of a renegotiation of the FTA with the US. If tariffs are imposed on Mexican sugar, retaliation could involve restrictions on high-fructose corn syrup imports from the US. Furthermore, the sugar industry is also facing challenges related to aging sugarcane plantations, which could lead to rising agricultural costs and a potential collapse of the domestic market due to increased imports. This has led industry representatives to advocate for a more sustainable, rational approach to production, focusing on maintaining planted areas rather than increasing output for growth's sake.

The 2024/25 sugar cycle is expected to yield over 5 mmt, but with the surplus, there is pressure to increase exports, particularly in light of rising imports of high-fructose syrup and yellow corn. Despite these challenges, there are positive expectations for the harvest, although issues such as labor shortages and logistical difficulties remain. Mexico's sugar industry faces domestic and international pressures that will likely influence future sugar prices and trade dynamics.

Pakistan

Pakistan's sugar prices decreased to USD 0.40/kg in W50, marking an 11.11% decline in both WoW and MoM. Projections suggest the wholesale price could increase to USD 1.51/kg (INR 128/kg) in Dec-24, potentially reaching USD 1.57/kg (INR 133/kg) in Jan-25. Furthermore, speculation about future trade conditions suggests that prices could rise by an additional USD 0.094/kg (INR 8/kg) in the coming months. While current prices remain relatively stable, ongoing concerns over supply chain dynamics and market speculation may lead to further fluctuations in sugar prices.

3. Actionable Recommendations

Diversify Export Strategies and Markets

To address declining global sugar prices and reduced export demand, stakeholders should prioritize diversifying export markets by targeting regions with untapped potential, such as Southeast Asia, through agreements like the Peru-Thailand FTA. Leveraging trade opportunities and expanding into markets with growing import demand can stabilize revenues despite challenging global conditions. For example, Peru's focus on exporting sugar to Thailand as part of its agricultural export strategy highlights the benefits of such diversification.

Invest in Sugarcane Alternatives and Ethanol Production

With rising competition for sugarcane due to increased global ethanol production, especially in Brazil and India, stakeholders should explore investments in integrated production models that optimize the use of sugarcane for both sugar and bioethanol. By enhancing processing capacities and adopting technologies for flexible output, businesses can capitalize on the growing demand for sustainable energy sources while mitigating the risks of market dependency on sugar alone.

Strengthen Self-Sufficiency and Sustainable Practices

In regions like the EU, where sugar production is projected to decline due to sustainability concerns and shifting consumer preferences, stakeholders should focus on supporting sugar beet cultivation through sustainable agricultural practices. Encouraging crop diversification and investing in modern farming techniques can help maintain production levels while aligning with environmental goals. Developing partnerships with local producers can also enhance supply chain resilience and reduce reliance on imports.

Sources: Tridge, El Peruano, Revista Campo, Grain Trade, Ukragroconsult, Vinanet, Portal Do Agronegócio, El Sol de Cordoba