1.Weekly News

United States

USDA Anticipates Increases in the 2024/25 Global Sugar Production and Decreased Exports

The United States Department of Agriculture (USDA) Foreign Agricultural Service (FAS) forecasts global sugar production in 2024/25 to reach 186 million metric tons (mmt), an increase of 1.38% year-on-year (YoY) compared to the estimate of 183.5 mmt for 2023/24. According to the USDA, an increase in India and Thailand’s production is expected to offset the production drop in Brazil. Global exports are projected to decrease by 3.53% YoY to 65.83 mmt in 2024/25, and world consumption is expected to reach 178.8 mmt, up from 177.33 mmt in 2023/24. Additionally, world stocks at the end of 2024/25 are anticipated to decrease by 4.67% YoY to 38.34 mmt.

Sugar Futures Decline on New York and London Stock Exchanges

On May 24, 2024, sugar futures slightly decreased on the New York and London Stock Exchanges. In New York, there was a 0.05% to 0.11% decline in contracts, with the Jul-24 raw sugar contract trading at 18.15 cents per pound. In London, futures contracts for raw and white sugar also showed a negative trend, with the Oct-24 white sugar dropping by 2.80% to USD 515.6 per metric ton (mt) and the Dec-24 contract declining by 2.60% to USD 506.1/mt. This decrease in sugar prices can be attributed to currency fluctuation, anticipated strong sugarcane yields in Brazil, expanded European Union (EU) production capabilities, and higher imports from Ukraine. These factors have raised concerns about a possible decline in global sugar prices.

Brazil

Brazil's Sugar Production and Exports Expected to Decline in the 2024/25 Season

The USDA anticipates that Brazil's sugar production will reach 44 mmt in the 2024/25 season, 1.54 mmt less than the previous season but it is still the second highest on record. This decline is attributed to the reduced volume of sugarcane available for crushing due to dry weather conditions. According to the USDA, Brazil's sugar exports are forecasted to decline by 4.1% YoY to 34.5 mmt.

Significant Increase in Sugarcane Harvest and Sugar Production in Minas Gerais, Brazil

As of May 24, 2024, the sugarcane harvest in Minas Gerais, Brazil, surged 41% YoY to 6.7 mmt. This led to the production of 356 thousand mt of sugar, marking a 48.6% YoY increase compared to the previous year. Additionally, ethanol production reached 219 thousand cubic meters, representing a 32% YoY increase.

Thailand

USDA Forecasts Increased Sugar Production and Decreased Exports and Stock in Thailand

According to the USDA, Thailand's sugar production is forecasted to increase by 16.4% YoY in 2024/25 to 10.2 mmt, driven by a recovery in sugarcane production and a higher level of total recoverable sugar (TRS). However, exports are anticipated to decline by 10% YoY to 9 mmt, and the stock is projected to drop by 45.3% YoY to 2.92 mmt.

India

USDA Forecasts Increased Sugar Production and Stocks, Decreased Exports and Stock in India

In the 2024/25 season, the USDA has forecasted a 500,000 mt increase in India's sugar production, reaching 34.5 mmt due to improved yields. Despite this growth, sugar exports are anticipated to decline by 20% YoY, totaling 3.7 mmt, as the government is likely to continue restricting shipments to satisfy domestic demand. Consequently, sugar stocks in India are expected to rise by 17.7% YoY, amounting to 12.35 mmt.

2.Weekly Pricing

Weekly Sugar Pricing Important Producers (USD/kg)

Yearly Change in Sugar Pricing Important Producers (W21 2023 to W20 2024)

.png)

* Blank spaces on the graph signify data unavailability stemming from factors like missing data, supply unavailability, or seasonality

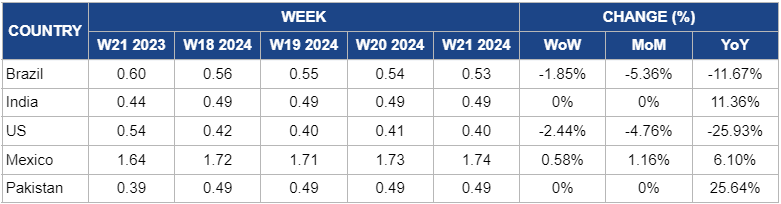

Brazil

Due to ample supply, Brazil's sugar prices fell by 0.85% week-on-week (WoW) to USD 0.53 per kilogram (kg) in W21. According to the USDA, Brazil's sugar output for the 2023/24 marketing year (MY) is projected to reach 45.5 mmt. Despite a slight YoY reduction in the 2024/25 production forecasts, optimal weather conditions, investments in sugarcane field renovation, and yield improvements are expected to continue putting downward pressure on prices

India

Sugar prices in India remained unchanged at USD 0.49/kg in W21, marking no WoW changes for the fourth consecutive week and an 11.39% YoY increase. This is attributed to India's decision to halt sugar exports this season to stabilize local prices amidst electoral activities and erratic rainfall in key sugarcane-growing regions such as Maharashtra and Karnataka. According to the USDA, India’s sugar is expected to decrease by 20% YoY in MY 2024/25.

United States

Sugar prices in the US dropped by 2.44% WoW to USD 0.40/kg in W21 compared to USD 0.41/kg in W20. This decrease can be attributed to declined sugar futures prices due to improved global sugar supply prospects. According to the USDA, the sugarcane harvest in the 2023/24 season exceeded market expectations at 705.2 mmt, 8% higher than the initial estimate of 652 mmt.

Mexico

Mexico's sugar prices increased to USD 1.74/kg in W21. Despite an amplified global supply, sugar prices in Mexico have experienced significant increases due to underlying inflation, supply shortages, and unstable fuel prices.

Pakistan

The price of sugar remained stable in Pakistan during W21, at USD 0.49/kg. According to the Pakistan Sugar Mills Association, Pakistan forecasts a surplus of at least 1.5 mmt in MY 2023/24 due to a record annual production. The association highlighted that the increased sugar availability has reduced sugar mills' margins, making it difficult to compensate sugarcane producers adequately.

3.Actionable Recommendations

Investment in Yield Enhancement Technologies

To address challenges such as dry weather conditions affecting sugarcane yields, stakeholders in Brazil and other affected regions should prioritize investment in yield enhancement technologies. Research and development initiatives focused on drought-resistant sugarcane varieties and precision agriculture techniques can help optimize yields and mitigate production losses.

Enhanced Market Intelligence and Risk Management

To navigate the dynamic sugar market landscape, stakeholders should prioritize enhancing market intelligence and implementing robust risk management strategies. Regular monitoring of global sugar market trends, currency fluctuations, and policy developments can help anticipate market shifts and mitigate risks associated with price volatility and trade disruptions.

Investment in Infrastructure and Logistics

Improving infrastructure and logistics capabilities in sugar-producing regions can help reduce production costs, enhance supply chain efficiency, and facilitate market access. Investments in transportation networks, storage facilities, and port infrastructure can streamline the movement of sugar products to domestic and international markets, ensuring timely delivery and competitive pricing.

Sources: Tridge, Canal Rural,