W36 2024: Potato Weekly Update

.jpg)

1. Weekly News

Global

Potato Market Poised for Strong Growth, Reaching USD 137.46 Billion by 2029

The global potato market is forecasted to grow from USD 115.74 billion in 2023 to USD 137.46 billion by 2029, driven by the crop's adaptability to various climates, ease of storage, and significant nutritional benefits. These characteristics position potatoes as an essential staple in regions facing food security challenges. The market includes over 4,000 edible potato varieties, most cultivated in the Andes of South America. A critical market growth factor is the shift toward processed potato products. Less than half of potatoes globally are consumed fresh, with the rest processed into items such as frozen French fries, potato chips, flour, dehydrated cereals, and starch. The Asia-Pacific region, particularly China, is the fastest-growing potato market. China’s production increased from 75.7 million metric tons (mmt) in 2019 to over 78.2 mmt in 2020, with 60% of the harvest consumed fresh in households and restaurants.

France

2024/25 French Potato Campaign Faces Challenges but Production Remains Stable

The 2024/25 French ware potato campaign has faced significant challenges due to adverse weather conditions and plant supply issues. Despite these obstacles, production and market prospects remain stable. According to the National Union of French Potato Producers (UNPT), potato sowing was delayed by up to six weeks, and wet conditions led to increased pressure from diseases like mildew. However, the UNPT estimates an average national yield of 45.5 metric tons (mt) per hectare (ha), consistent with the past decade's average. However, variability will be based on variety, sowing dates, and regional conditions. The potato supply is expected to be sufficient to meet the growing domestic, European, and global demand for French potatoes. This supply and demand balance is anticipated to support the sector's development and prepare it for a solid 2025/26 campaign.

Germany

Germany's 2024 Potato Harvest Expected to Rise Despite Lower Yields

The German Ministry of Agriculture forecasts an average potato yield of 41.1 mt/ha for 2024, a 6% year-on-year (YoY) decline compared to last year. However, this lower yield per unit area is offset by a 9% YoY increase in the total cultivated area, now at 289,300 ha. As a result, Germany's potato harvest is expected to reach 11.9 mmt, a 2.5% increase from last year's production of 11.6 mmt.

Peru

Potato Prices Surged in Huancayo in W36

In Huancayo, Peru, potato prices have surged, causing financial strain for local households. At El Tambo market, Yungay potatoes are priced between USD 0.74 and 0.79 per kilogram (kg), sparking consumer concern. Traders attribute the spike to a seasonal shortage, with larger potatoes selling for USD 0.66/kg and yellow potatoes, a premium variety, reaching USD 0.79/kg. The Ministry of Agricultural Development and Irrigation (MIDAGRI) also suggests that market speculation may contribute to the price hike.

Ukraine

Ukraine's Potato Sector Faces 36% Cultivation Decline in 2024

Ukraine's potato cultivation in 2024 experienced a 36% decrease compared to pre-war levels. This significant decline continues to impact the sector. Current yields vary, with private farms producing an average of 16.5 mt/ha while industrial enterprises achieve 25.8 mt/ha. The number of certified seed enterprises dropped sharply, from 30 in 2021 to 19 in 2024. As for seed potatoes, production is expected to reach 38,147 mt, yet the annual market need remains around 20 mmt. This shortfall in certified seed production and the reduced number of seed enterprises are insufficient to meet the country's demand for potatoes, exacerbating the sector's challenges.

2. Weekly Pricing

Weekly Potato Pricing Important Exporters (USD/kg)

* Varieties: France (Pomme de Terre), Netherlands (Bintje), Germany (Anabelle), Pakistan and Egypt (overall average)

Yearly Change in Potato Pricing Important Exporters (W36 2023 to W36 2024)

* Varieties: France (Pomme de Terre), Netherlands (Bintje), Germany (Anabelle), Pakistan and Egypt (overall average)

* Blank spaces on the graph signify data unavailability stemming from factors like missing data, supply unavailability, or seasonality

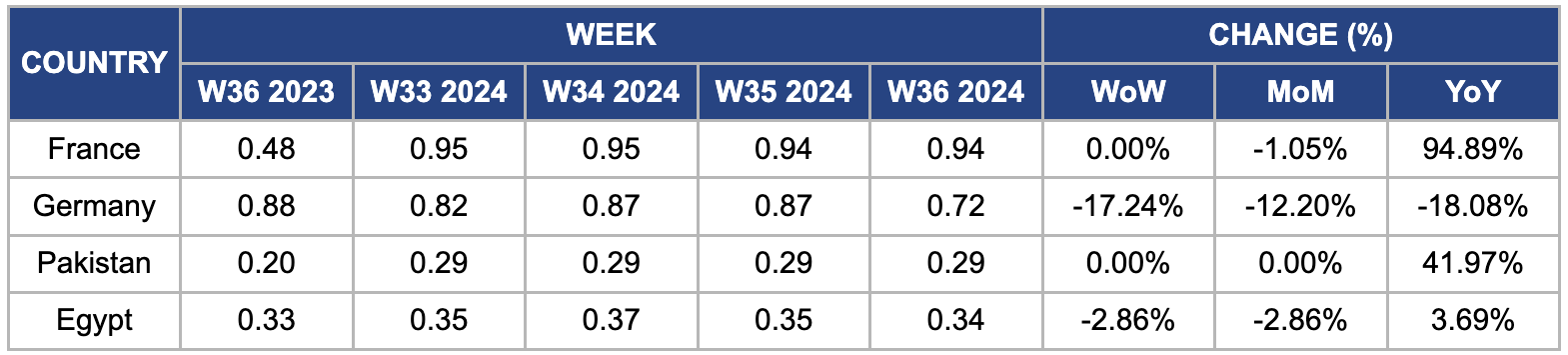

France

In W36, the wholesale price of French potatoes held steady at USD 0.94/kg week-on-week (WoW) but saw a dramatic increase of 94.89% YoY. The 2024/25 French ware potato campaign has faced significant challenges, including adverse climatic conditions and increased pressure from plant diseases, notably mildew, due to exceptionally wet weather. Despite these hurdles, the UNPT anticipates a balanced production and valorization outlook. Although sowing was delayed by up to six weeks and the sector faced complications with plant supplies, the prospects for the upcoming 2025/26 campaign look promising, suggesting a consolidation and potential for sector development soon.

Germany

The wholesale price of German potatoes fell by 17.24% WoW and 12.20% month-on-month (MoM) to USD 0.72/kg in W36. The price drop is due to Germany's potato harvest, which is expected to grow this year due to a 9% YoY increase in the cultivation area, reaching 289,300 ha. The German Ministry of Agriculture predicts production of 11.9 mmt, a 2.5% YoY rise from the previous year's 11.6 mmt.

Pakistan

Pakistan's wholesale potato prices remained stable WoW at USD 0.29/kg. However, prices significantly surged 41.97% YoY from USD 0.20/kg in W36, 2023. This price surge is due to high inflation, which reached 17.96% in Aug-24. Increased taxes and rising costs for essential utilities, including electricity, gas, and oil, have driven inflation. These factors have significantly raised potato production costs and increased wholesale prices.

Egypt

In W36, Egypt's wholesale potato prices decreased by 2.86% in WoW and MoM, falling to USD 0.34/kg. This decline is attributed to increased supply as the season progresses. Egypt expects further price relief with the new season starting in Nov-24. However, the current season has been marked by challenges, including difficulties in importing seeds due to a dollar crisis, which led to a 25% reduction in seed quantities compared to the previous year. Despite the recent decrease, YoY prices have risen by 3.69% due to a significant drop in yield. Production has fallen from 14 to 16 mt per acre in 2023 to 9 to 12 mt in 2024. Yields from local leftover seeds have also decreased to around 7 to 10 mt per acre, contributing to a 35 to 40% YoY reduction in market supply.

3. Actionable Recommendations

Optimize Production and Market Strategies for Germany

The decrease in wholesale potato prices in Germany indicates a shift in the market due to increased production. To address these changes, German producers should optimize their production and market strategies. Investing in precision farming techniques and yield-enhancing varieties like 'Laura' and 'Agria' can help maintain productivity despite challenges. Strengthening partnerships with processors and retailers will ensure better alignment of supply and demand. Additionally, enhancing supply chain efficiency through improved storage solutions and transportation networks will help stabilize prices and effectively meet market demands.

Expand Seed Potato Production and Improve Distribution in Ukraine

Ukraine's significant reduction in potato cultivation and the shortfall in certified seed potatoes highlight the need for strategic seed production and distribution improvements. This includes focusing on varieties like 'Sante,' 'Innovator,' and 'Agria,' which are known for their high yield potential and resistance to diseases such as late blight. Enhancing the capacity of seed enterprises to produce these improved varieties can help meet market demand. Additionally, improving seed distribution networks and offering subsidies or incentives for seed production can address shortages and support the recovery of the potato sector.

Invest in High-Yielding, Disease-Resistant Seed Varieties

France and Egypt should adopt high-yielding, disease-resistant potato varieties, which are crucial to combat yield losses due to disease pressures like mildew in France and declining yields in Egypt. French farmers, for instance, could benefit from planting varieties such as ‘Charlotte,’ ‘Bintje,’ or ‘Lady Claire.’ These varieties are known for their resistance to mildew and other joint diseases, making them ideal for regions experiencing wet weather conditions. Additionally, in Egypt, where the current potato season has been marked by reduced yields due to seed shortages and a dollar crisis, the introduction of ‘Spunta,’ a variety well-suited to Egypt's growing conditions, can help improve productivity.

Sources: AgroPortal.ua, Apnoticias, Nieuwe Oogst, Agro Digital, Agrotimes, Agrodigital