1. Weekly News

Argentina

Argentina's 2024/25 Corn Planting Delayed Due to Dry Conditions

The Buenos Aires Grains Exchange (BAGE) reported that Argentina's corn planting for the 2024/25 crop year is currently on hold in parts of the country's agricultural west due to insufficient soil moisture following several weeks of dry conditions. Argentina is the world's third-largest corn exporter, with plans to plant 6.3 million hectares (ha), targeting a production of 47 million metric tons (mmt). BAGE highlighted significant variability in water conditions across western Buenos Aires, causing delays in sowing as farmers await new rainfall. So far, only 18.5% of the planned corn area has been planted.

Brazil

Brazil's Corn Exports in Oct-24 Fall Short of Expectations

As of Oct-24, 59% of Brazil's 2024 second corn crop in the Center-South has been sold, slightly trailing last year's pace of 59.9%. The estimated production for 2024 is 85.891 mmt, lower than 2023's 99.098 mmt, and the five-year average sales pace for this period is 67.4%. State-wise, Mato Grosso leads sales at 65.1%, followed by Mato Grosso do Sul with 56.3%, Goiás/Federal District with 54.7%, São Paulo with 55.4%, and Paraná with 50.5%. Meanwhile, 62% of the 7.049 mmt of second-crop corn were sold in Matopiba, down from 70.7% in 2023.

Türkiye

Türkiye to Allow 1 Million MT of Corn Imports at Reduced Duty

On October 10, Türkiye's Trade Ministry announced a permit to import 1 mmt of corn by the end of 2024 with a reduced duty of 5%. This import quota aims to balance the corn supply and demand due to insufficient domestic production to meet consumption needs. If corn imports exceed 1 mmt, the duty will revert to 130%.

Ukraine

Ukraine's Corn Exports Surged in Early 2024/25 Season

As of October 9, Ukraine exported 11.41 mmt of the 2024/25 season's grains and pulses, an increase of 58.1% year-on-year (YoY). According to the Ministry of Agrarian Policy and Food of Ukraine, corn exports reached 3.08 mmt, 7.8% higher than last year's figure. This significant growth reflects a strong export demand in the early stages of the marketing year.

Poltava Region Forecasts Significant Decline in 2024 Corn Harvests Due to Unfavorable Weather

The Poltava region is anticipating a decrease in its gross harvest of crops in 2024 due to unfavorable weather conditions. The corn harvest is expected to decline by nearly 1 mmt, with projections estimating a total of 2.8 mmt, down from 3.7 mmt last year. Factors contributing to this decline include insufficient air and soil moisture, a lack of rainfall, and excessively high temperatures, leading to drought conditions that adversely affect plant development.

United States

US Corn Harvest Progressed Ahead of Schedule

According to the United States Department of Agriculture (USDA) report, the United States (US) corn harvest is 30% completed as of October 7, ahead of the five-year average. Corn conditions were 64% rated good to excellent, reflecting the best crop ratings since 2018. Despite dry conditions in the Midwest, which sped up fieldwork, the USDA expects record US corn yields. The US remains the largest corn exporter globally and the second-largest soybean supplier, trailing Brazil.

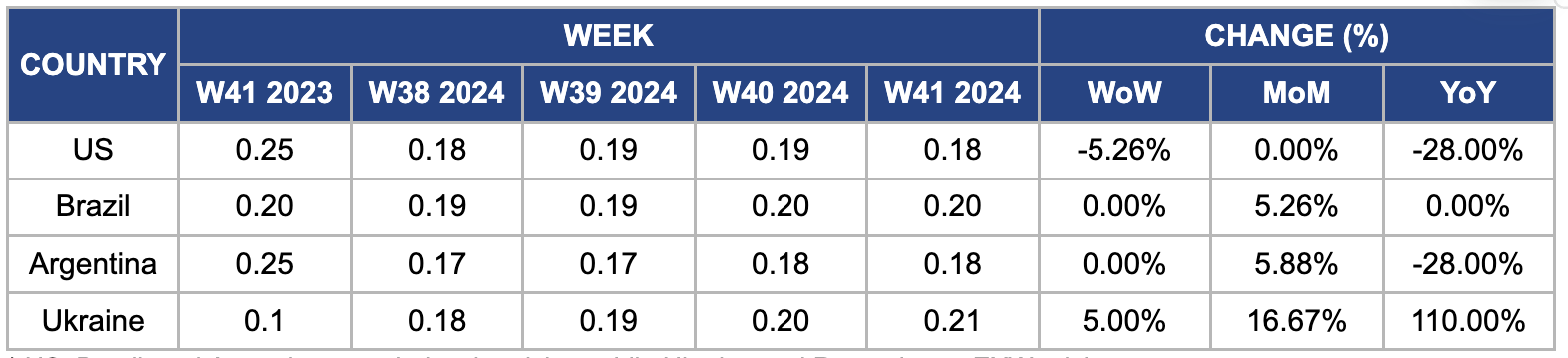

2. Weekly Pricing

Weekly Maize Pricing Important Exporters (USD/kg)

Yearly Change in Maize Pricing Important Exporters (W41 2023 to W41 2024)

US

In W41, wholesale maize prices in the US decreased 5.26% week-on-week (WoW) and 28% YoY, reaching USD 0.18 per kilogram (kg). This is mainly due to the USDA's upward revision of corn production and yield forecasts, now estimating output at 15.186 billion bushels with an average yield of 183.6 bushels per acre. This improved production outlook has contributed to a more favorable supply situation, significantly affecting the YoY price decline.

Brazil

In W41, wholesale maize prices in Brazil remained unchanged WoW and YoY but rose 5.26% month-on-month (MoM) to USD 0.20/kg. This increase is due to a decrease in total acreage for the first crop, estimated at 9.26 million acres, a 6% YoY reduction, leading to a production estimate of 23 mmt, down 2%. The safrinha corn acreage is estimated at 39.19 million acres, a 2% decrease, with production projected at 100 mmt, an increase of 10%. Overall, total corn production for the 2024/25 season is expected to reach 125 mmt, a rise of 2.5 mmt. Moreover, solid international demand, rising corn prices abroad, and the appreciation of the US dollar's elevated port values make it challenging for Brazilian buyers to purchase corn. Although some farmers had previously been willing to lower their asking prices in early Sep-24 due to storage constraints and cash flow needs, market dynamics have shifted.

Argentina

The wholesale price of Argentine corn remained unchanged WoW but increased by 5.88% MoM to USD 0.18/kg in W41. This rise is attributed to delays in the 2024/25 corn planting due to dry conditions, as BAGE reported. There are growing concerns regarding a potential leafhopper plague reminiscent of the one that devastated the previous corn harvest. This pest issue could result in approximately 2 million ha of corn being left unplanted, with a significant portion expected to shift to soybeans. Consequently, these challenges have delayed input sales and lowered planting expectations, leading to an anticipated production shortfall of around 21%YoY. The total planted area for corn is projected to decrease to about 8 million ha.

Ukraine

Ukrainian wholesale maize prices increased by 5% WoW, 16.67% MoM, and an impressive 110% YoY, reaching USD 0.21/kg. According to the Ukrainian Agrarian Council (UAC), this price surge is due to solid demand from exporters. Contrary to market expectations, the anticipated influx of new corn from Argentina did not alleviate demand or lead to lower prices for Ukrainian grain. The UAC noted that China has been actively contracting Ukrainian corn, with significant purchases from other importers, including Türkiye, Egypt, Italy, and Spain. European traders reported that Chinese importers secured at least 65 thousand metric tons (mt) of animal feed corn from Ukraine, further bolstering demand.

3. Actionable Recommendations

Enhance Export Strategies

Brazilian corn producers should diversify export markets to mitigate reliance on traditional buyers like the European Union (EU) and North America. This could involve forging partnerships with emerging Asian markets, including China, India, and Africa, where demand for corn is increasing. Furthermore, enhancing logistics and infrastructure to facilitate faster export processes can help capitalize on current price dynamics. By broadening the customer base and improving export efficiency, Brazil can better position itself to maximize profits and reduce exposure to fluctuations in domestic market conditions, ultimately maintaining its status as a leading corn exporter.

Mitigate Planting Risks in Argentina

Argentine farmers should implement water conservation strategies and explore drought-resistant corn varieties to adapt to dry conditions. Collaborating with agricultural research institutions to develop and disseminate best practices for water management can enhance resilience against future dry spells. This initiative would involve partnerships with institutions like the National Institute of Agricultural Technology (INTA) and the University of Buenos Aires (UBA), emphasizing effective water management practices such as soil moisture monitoring and rainwater harvesting.

Enhance Data-Driven Decision-Making

Brazil and Ukraine should invest in data-driven agricultural technologies to optimize corn production and improve market strategies. Precision agriculture tools, such as satellite imagery and soil moisture sensors, can help farmers make informed decisions about planting schedules, fertilizer application, and pest management. Collaborating with tech companies to develop user-friendly platforms that aggregate weather forecasts, market trends, and yield predictions will empower farmers to respond quickly to changing conditions and market demands and focus on integrating Internet-of-Things (IoT) devices to monitor crop health and soil conditions in real time. Farmers can enhance productivity, reduce input costs, and ultimately boost profitability in a competitive global market by implementing these technologies.

Sources: Portal Do Agronegócio, UkrAgroConsult, Agrotimes, El Periódico Mexico, PortalDBO